")

Dear readers/followers,

In this article, I’ll take a look at French company Vinci SA (OTCPK:VCISY). This is a French concessions and construction business, that was initially part of one of the French multinational banks over 120 years ago. For some time now, it’s been one of the largest construction businesses in France, with annual revenues of over €60B, of which it manages an over 10% operating margin or EBIT.

In this article, we’ll look at what Vinci is, what it offers, why it has almost doubled its annual sales volume in around 10 years, and why investing in this business could be a good idea if you’re interested in owning construction, energy and automotive tolls, which is another part of the company’s operations.

This will be my first direct article on Vinci S.A. I do a lot of coverage of European stocks here on SA – in fact, I would say I mainly try to focus on European stocks and offer the undervalued ones for your consideration with a personal “BUY” rating.

I also don’t take a “BUY” rating if I don’t have skin in the game – and in this company, I’ll show you if I consider it the right time to get some skin in the game on Vinci, or if we should wait.

A lot to like about Vinci, construction, and tolls – but what is the price?

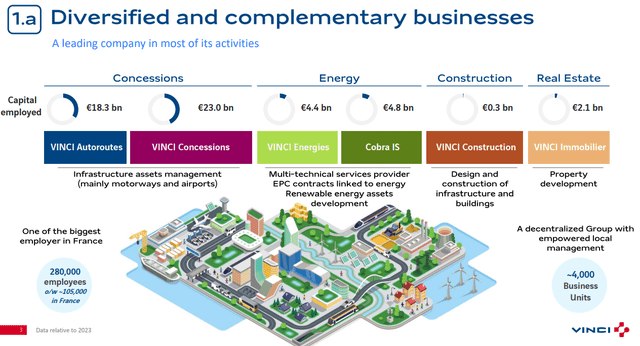

Vinci does a lot of things, and as such, has a lot of different competitors in a lot of different fields. Vinci builds infrastructure – both small and large – with competition both nationally and internationally. The company also does airport infrastructure and economics, automotive tolls, Vinci Energies (energy services), and the company’s segment known as EUROVIA, which focuses on surfacing.

The company has over 45,000 employees, is one of the very few A-rated construction businesses in the entire world, and offers you, the investor, a yield of at least 4.3% with an upside in construction, based on a current payout of €4.3/share on a native share price of €104.4. Looking at the ADRs of companies like this, the yield sometimes doesn’t tend to translate all that well, but as this is an article on the ADR – the ADR yield is based on SA data, $1.85 annually, which currently comes to 6.52% annualized with a bi-annual payout – but keep in mind that the second biannual payout for this company isn’t necessarily the same size as the first, which was paid in May 2024 for the ADR.

The company has very low overall debt – under 45% long-term debt/cap- and a mix of businesses that are somewhat atypical for the sector wherein they operate.

What are the investment arguments for Vinci then, aside from this?

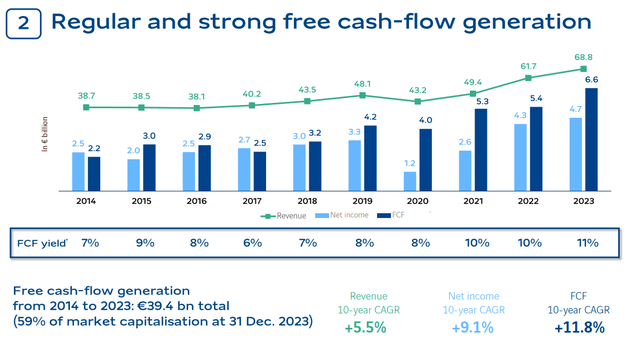

The company argues that a resilient business model with regular and strong FCF, good capital allocation strategies with proven results, M&A track records, a good shareholder base that’s shareholder-friendly, but not dictated by yield, and a liquid stock that’s, as the company itself would argue, is central to the world’s challenges. This argument makes sense, as it’s in line with what is being considered globally, and where it’s already set to change by 2030 not merely based on what companies like Vinci are doing, but by policies.

Vinci IR (Vinci IR)

Some would say that Vinci is mainly a French company. While this is technically true on the basis of a revenue mix, the company has nearly 57% of its revenues outside of France, which is an increase of almost 80% in less than 10 years time. Vinci has had a goal to diversify its revenues – and it has. It now has operations and projects in more than 120 nations, much of which are in Europe, with a small Asia exposure, and only a slight NA exposure. It’s therefore mainly a European player, with both the negatives and positives that come with this.

Where Vinci S.A differs from its construction peers such as Skanska is that it generates non-trivial cash flow from recurring operations which are not RE-based.

Vinci IR (Vinci IR)

Instead of the typically volatile RE-based home and property-selling arms, you have stable and technology-neutral automotive toll collection and similar segments, which offer a very nice cushioning in terms of cash flow. it doesn’t insulate the company, as you can see in 2020 during COVID-19, but it offers very good upside nonetheless.

The company’s maturities and repayments are very conservative. It has an NFD/EBITDA of 1.3x, fully reflecting the strong A-/A3 ratings that it has, and has liquidity of over €13B at around the time of writing this article.

For the capital it generates, Vinci has a sound allocation and working strategy that includes a 50% FCF payout ratio, M&A’s where needed, and share buybacks to offset any M&A dilution that comes in -while using the company’s remaining cash to de-lever.

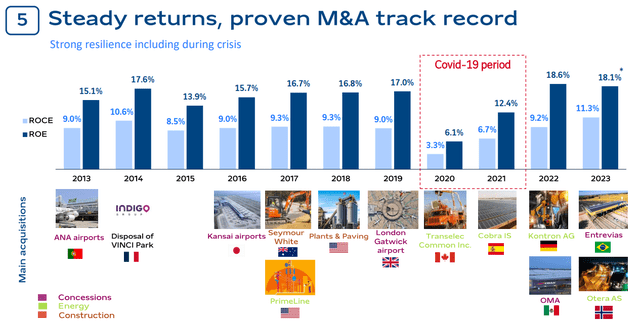

It is in fact, one of the best M&A’ers out there in this sector, and can prove this.

Vinci S:A (Vinci S:A)

Some investors ask me why I like French companies so much. My answer is when they work, they really work – and by that, I mean that French companies, compared to some German and Scandinavian ones, tend to be more apt at non-European M&As, which we prove with the mix we see above.

Over time, Vinci has averaged a TSR of 12% per year, or almost 200% since 2014. This is better than Stoxx600, better than CAC40 and better than many indices out there.

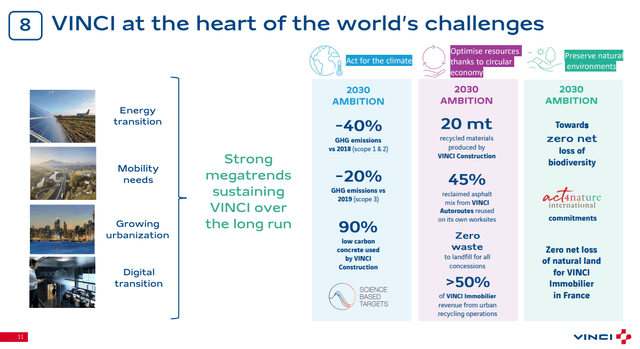

Vinci’s current operations and projects are further at the heart of what is making the world “tick” today and what’s bringing upcoming change. We do not need to take management’s word for this. The energy transition in particular is something that many argue must be transformed completely.

Vinci is certainly not unique in having appeal in these megatrends – Siemens (OTCPK:SIEGY) and other industrials are at the heart of it as well, but it’s in an attractive position given its multinational, 120+ country exposure, and with its concession business has an attractive “safety net” in terms of recurring income.

Vinci IR (Vinci IR)

Some of the interesting, non-typical segments are as follows.

Vinci Autoroutes manages 4,400+ km worth of automotive infrastructure under concessions, which comes to almost 50% of the conceded French toll roads. In short, if you drive in France, you’re likely at some point driving on a Vinci road.

This segment, which is super, generates revenues of €6.3B with an EBITDA margin of 74% as of the latest operations.

Second, Vinci Airports, because there is significant value here. Vinci now operates over 70 airports across 13 nations, with significant revenues. Here also, the company posts margins of over 63%. The EBITDA margins for these concessions are insane, and for this company, a single year amounts to over €7B in EBITDA from Concessions alone. And that’s not taking other concessions into account, which Vinci has in the form of over 3,100 km motorways in 10 countries, and over 30 projects managed in the form of stadiums, railways, and the like.

As such, this is a company with, as I see it, a very interesting mix of business that is quite atypical when compared.

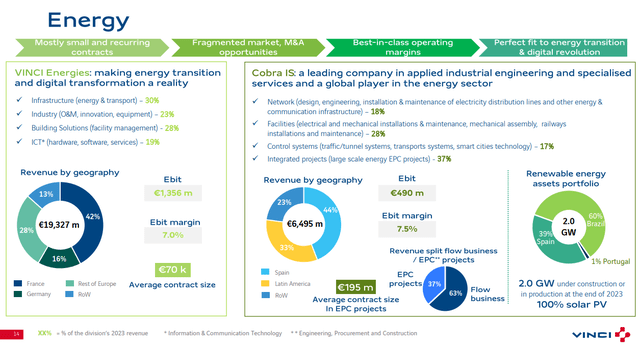

And that’s even without going into the company’s energy segment – which supports the ongoing energy transition.

Vinci IR (Vinci IR)

One of the major concerns held by some investors is French politics – so before we go into valuation for this business, let’s take a closer look at what potential risks and upsides we could see for this business.

Upsides and Risks for Vinci

Those positives about Vinci, like me, would point to the appealing company mix of diversified concession assets which act as an opportunity to own irreplaceable infrastructure across multiple fields. This, more than the construction segment, is why I invest in Vinci. The returns for these assets are supported by the fact that some of these contracts are extremely long-term. This is added to by the company’s attractive airport business, which is likely to further improve earnings and results, which will allow further room for payouts, and for the company to move forward with plans.

Overall, from a company-specific perspective, I don’t see many risks – instead, macro provides the biggest downside here, because Vinci has a solid order book with good projects. It enables Vinci, like my other builders such as Skanska and NCC, to be very selective about projects, which has become the norm in the sector for the past 10 years.

But, nothing positive without negative. If you believe that a somewhat socialist-oriented nation like France is going to accept 60-70% toll and concession margins from a company without a discussion, you need to read more about France. These returns in the concession segment have already been under scrutiny, and taxation is likely.

That’s one drawback. Secondly, these concessions are granted politically, which does introduce political risks.

Aside from the French political and regulatory risks, every other potential downside is “macro” to this company – as I see it.

This provides us with a fairly good visibility going forward.

Vinci – The company has quite a bit of upside at the right price

Estimating a fair value for Vinci is based on the continued stability and growth of its FCF, and the latest result supports positive assumptions here. Vinci continues to see record-high EBIT margins in most segments, and I further forecast that the company can manage to keep its elevated 12% operating margin over time for the group. This is an increase from my previous working assumption of about 10.5-11%. When combining this with the company’s leverage, you start to see a very interesting upside considering current revenue growth.

I don’t expect historical revenue growth to continue – more to 4-5% due to the recovery in passengers and volume being more muted as opposed to post-COVID-19 – but I believe this is made up for by the company’s excellent and well-filled order book.

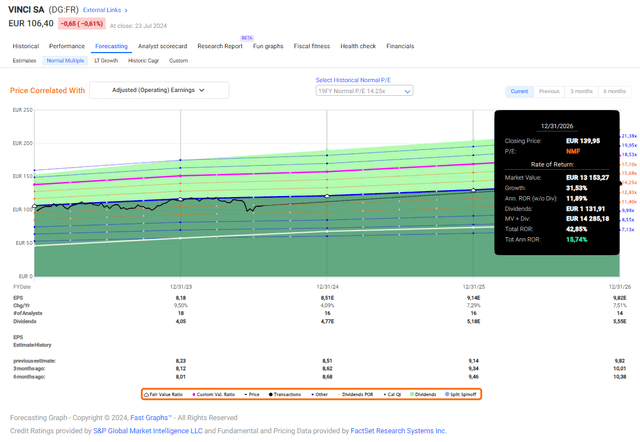

Vinci S.A. is far more stable than you’d typically expect from a construction company. This lends me the confidence to put high credibility to the 20-year P/E average as a target for the company. (Source: Paywalled F.A.S.T Graphs link)

Vinci is currently trading at about 12.52x for the VCISY ADR ticker. This is not an excessively cheap valuation for the company, and it doesn’t make it the “best alternative around”, but Vinci also rarely crashes down hard. I believe the best option for this company is to slowly add shares, taking into account that the company may drop more, but aware of the fact that it already is appealing. At the current valuation, when averaging around a 20-year P/E average with a 15% annualized upside, there is appeal here.

F.A.S.T graphs Vinci Upside (F.A.S.T graphs Vinci Upside)

I would give the company a “cheap” description at a double-digit native share price close to €90/share for the native – now it’s merely attractively priced for an FV estimate of roughly €140/share, which is also where I put my introductory price target for Vinci. When looking at the ADR VCISY, which is a 0.25x ADR to the native, this translates to a fair value of $37.99 at today’s price, around $38/share for VCISY, and becoming cheap at around $24/share.

At the 5-year average, Vinci has a far higher premium of 16-17x, which opens the possibility of 20%+ annualized RoR, but I believe the more conservative assumption is the one to go with here.

My stance is that Vinci offers an appealing way to make 15%+ annualized at this time, from a conservative perspective, and this makes the company a “BUY” at today’s price. The only way the company is worth long-term less than $34-$38/share is if it does not grow – and I don’t see this as being valid.

Here is my current thesis for Vinci.

Thesis

- Vinci has one of the most interesting business mixes and revenue mixes in all of Europe for a construction company. The toll and concession segments offer, as I believe it, one of the most interesting and advantageous upsides in this entire sector at the right price, and a superb cushion for the volatility typically inherent to these types of businesses.

- With a healthy 4% dividend yield supported by strong capital allocation, very good margins and a good order book visibility, risks for Vinci are what I would consider limited. At most, they are relegated to taxation and regulatory scrutiny, aside from macro.

- Because of this, I would consider this company to be a “BUY” here, with a conservative PT of $38 for the VCISY ADR, with around €140/share for the native ticker.

- I have recently added a position due to the company’s moaty concessions business coupled with the fundamental appeal of its construction and energy businesses.

Remember, I’m all about:

-

Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

-

If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

-

If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

-

I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

-

This company is overall qualitative.

-

This company is fundamentally safe/conservative & well-run.

-

This company pays a well-covered dividend.

-

This company is currently cheap.

-

This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The only issue here is that the company isn’t really “cheap” – aside from this, there is plenty to like about Vinci here, and I say “BUY”.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")