")

As many of my readers have probably noticed, I am quite skeptical of office REITs except for two players: Alexandria Real Estate Equities Inc. (ARE) and Cousins Properties Incorporated (NYSE:CUZ). In my opinion, both of these REITs exhibit strong fundamentals, but at the same time they have been punished by the market together with the rest of the office segment. It is clear that the valuations should be lower than in the pre-pandemic period, when the monetary policy was extremely accommodative, yet, in my view, the discount has gone too deep, which, in turn, provides an opportunity for investors.

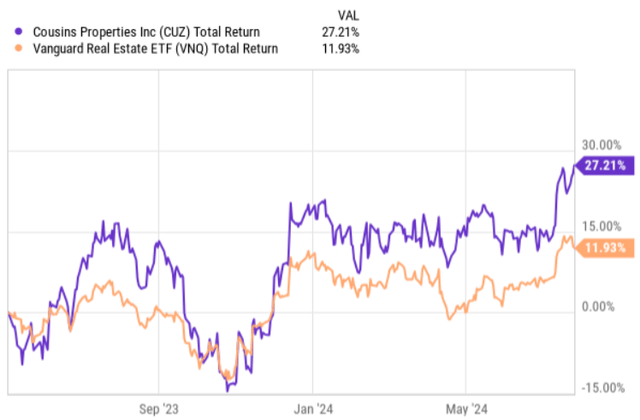

On CUZ, specifically, I have been following since mid-2023, when I issued my first article on this REIT. Since then, the stock has delivered outsized total returns, beating the overall REIT index despite being a pure play office player.

Ycharts

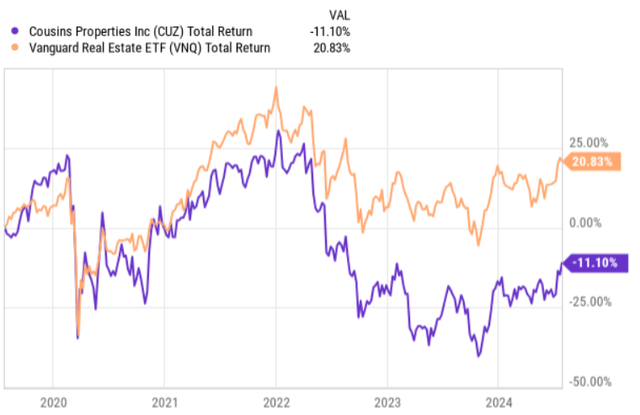

However, if we zoom back a bit more and assess the total return performance over the past 5-year period, we will notice that there is still a notable gap between the broader REIT market and CUZ. Once again, this, at least theoretically, provides an additional opportunity.

Ycharts

Now, recently CUZ circulated its Q2, 2024 earnings deck, which, in a nutshell, confirms my thesis on CUZ’s fundamentals and thus the potential for capturing juicy returns on a go forward basis.

Let me now dissect the earnings report and elaborate on why I think that it is worth holding CUZ in a portfolio.

Thesis review

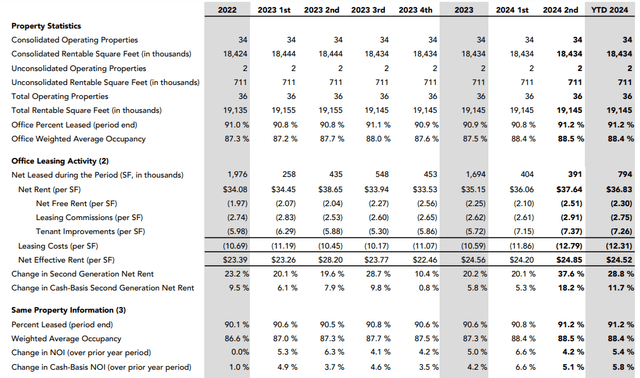

The Q2 2024 earnings figures came in strong. They had the same property net operating income on a cash-basis increasing by 5.1% and second generation net rent per square foot on a cash-basis expanding by 18.2% compared to Q2 2023. As a result of these dynamics and, in general, improved prospects, the Management has strengthened its funds from operations (“FFO”) guidance to between $2.63 and $2.68 per share from previous guidance of $2.60 and $2.67 per share.

If we take a look at the table below, we will observe a couple of important elements:

- CUZ has not made any acquisitions or divestitures since 2022; instead, it has kept its 34 trophy-like consolidated properties in its books, while directing some FFO generation towards refurbishments and maintenance.

- These key properties (including two unconsolidated ones, which are owned through JVs) have delivered consistent NOI growth each quarter that has occurred since the start of 2023.

- Meanwhile, the occupancy ratio has remained high at circa 88%, which is also really in line with the level that was recorded in the pre-pandemic period.

CUZ Q2, 2024 earnings deck

All of this confirms that the quality and location of office buildings matter, and that CUZ is inherently more protected from the secular headwinds than other peers that own Class B properties in subpar locations.

At the FFO generation front, which is effectively the key metric determining how healthy the REIT is, we can notice rather favorable dynamics as well.

The FFO per share has increased from $0.65 per share in the prior quarter to $0.68 now, which implies an FFO payout level of circa 48%. Yet, for office REITs it is typically better to assess the distribution coverage or actual cash payout level based on FAD, which primarily considers a second generation capital expenditures that are associated with new tenants moving in. In FAD terms, the payout level lands at 62%, which is still conservative, leaving ample liquidity in the books.

Finally, one of the main (if not the most important) advantages that CUZ embodies is its fortress capital structure. During times like this, having a robust balance sheet and access to a massive pool of fresh liquidity could be treated as a separate asset.

As I mentioned earlier in the article, the fact that CUZ has not ventured into new and sizeable M&A transactions has allowed management to keep the balance sheet in check. This in combination with consistent FAD retention (after covering the dividends) creates further opportunities to de-risk the balance sheet from an already conservative level (e.g., net debt to annualized EBITDAer of 5.12x).

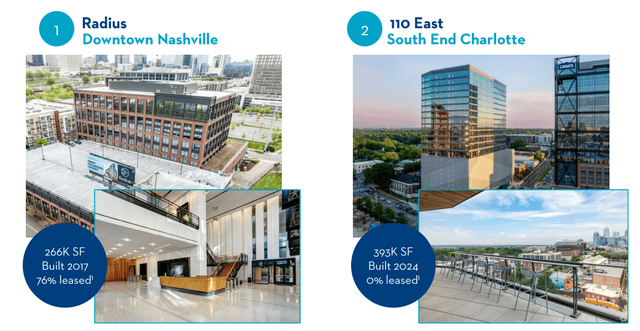

In July, we saw, however, the first minor moves of the Management deploying some part of the retained FAD into new investment opportunities. Namely, CUZ has injected circa $27 million into two separate mezzanine loans that yield SOFR + 8.25% (and 9.00% for the other) and are already accretive to their earnings.

CUZ Mezzanine loan presentation

The picture above shows the properties in which CUZ has assumed indirect interest via mezzanine loan investments. Both of these properties are located in the Sun Belt market and are consistent with high-quality strategy.

The bottom lines

All in all, the recent quarterly earnings report yet again proves that CUZ is a different kind of office REIT. It is more resistant to the structural headwinds and even has strong enough fundamentals, to record consistently growing like-for-like NOI figures.

On top of this, the balance sheet remains strong as each quarter there is an incremental cash retention in the business (from conservative FAD payout), which with a prudent management helps keep the financial risk level low.

Given that the multiple here is rather depressed — at P/FFO of 9.5x — and the dividend yield is still attractive at ~ 5% despite the conservative FAD payout, Cousins Properties Incorporated continues to be a clear buy for me.

Read the full article here

")

")

")