")

")

Investment thesis

Agora (NASDAQ:API) provides a B2B platform for real-time communication and interaction through text, voice and video. The company’s APIs and SDKs allow developers to integrate multiple communication channels in their applications, with a greater focus towards video communication. The company differentiates itself by leveraging its technology to deliver exceptional live video quality which gives an enhanced user experience. At the end of Q1 last year, the company was restructured into two independent business so that its international business operated under the Agora brand, while the Chinese business operated under the Shengwang brand. The former continues to show solid growth while the latter has faced several headwinds leading to revenue declines.

The company has demonstrated improving margins despite a lack of overall revenue growth through substantial expense reductions. Revenue growth is expected to improve in upcoming quarters as the business is likely to benefit from industry tailwinds. The current market cap which is well below the company’s net cash reflects a pessimistic view of the business that I do not share. Though upside depends on the company demonstrating solid organic growth and reaching FCF breakeven, downside is limited by its strong cash position and reduced cash burn. Meanwhile management continues to leverage its balance sheet strength to repurchase shares at discounted prices. I rate shares a hold as I wait to gain higher confidence in upcoming quarters that the company is on a sustainable path towards profitable growth.

Q1 earnings review

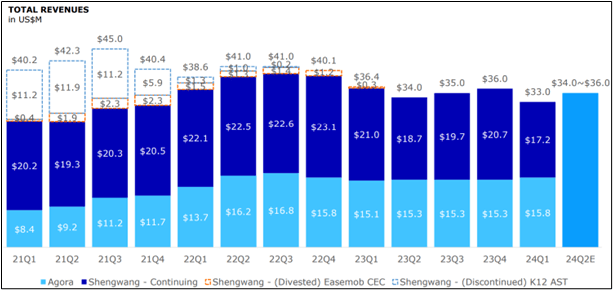

Q1 Investor Presentation

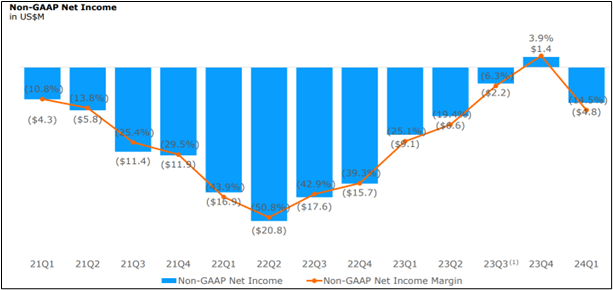

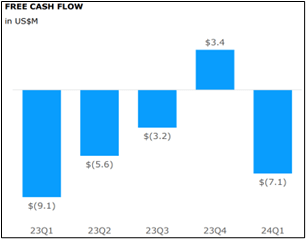

The company’s Q1 total revenue was $33 million, down 9% versus the prior year period as shown above. Revenue from the Agora business grew 4.6%, while in Shengwang revenue declined by 16% year over year. Overall results were impacted by a low season for its social and education customers but were still within management’s guidance. Non-GAAP income and FCF improved to -$4.8 million and -$7.1 million respectively, compared to -$9.1 million and -$9.1 million versus Q1 2023. The margin improvements depicted below were achieved despite lower revenue and weaker gross margins, driven by expense reductions of $7 million in the quarter versus Q1 2023. The Dollar-based net retention rate was 78% for Shengwang, though much stronger at 92% for the Agora business.

Q1 Investor presentation

Management’s guidance for Q2 of $35 million at the midpoint, indicates an expectation for solid sequential and year over year growth driven by certain growth drivers which I will discuss next.

Expectations going forward

Potential growth drivers

Management expects tailwinds for the business from the next generation of chatbots such as ChatGPT-4o which can reason across audio, video, and text in real time. Speaking about this on the Q1 earnings call its CEO discussed the opportunity in detail stating:

We anticipate a paradigm shift in the interaction between human and AI models, which will inspire the next generation of killer apps. As this shift will lead to a substantial increase in the amount of voice and video feed transmitted globally in real time, the importance of a low latency and highly reliable transmission network will be higher than ever. This will put us in the unique position to become the critical infrastructure in the AI first future of human computer interaction.

Management also expects the Shengwang business in particular to benefit from the European Football Championship and Olympic Games this summer, as it has partnered with leading sports broadcasting platforms in China. The advantages of its solution over legacy systems for broadcasting is expected to keep demand high for the rest of the year. This was further explained by its CEO when he said:

I believe this new experience will trigger a major transformation in sports broadcasting and our powerful, flexible and cost-effective solution will become widely adopted by additional platforms to power many other live sports — live sporting events throughout the year.

Margin improvement

The company has made major strides in recent quarters to right size its cost structure and divest non core assets. The company’s CFO expects the current expense run-rate to remain stable stating:

So looking forward this year, we are still very cautious about the overall operating environment. So we will continue to manage our expenses very carefully and we do not expect Opex in general and including R&D expenses to increase sequentially from Q1 onward.

I therefore expect margin improvements in upcoming quarters to be mainly driven by revenue growth. Given that the company continues to spend more than 40% of its revenue on R&D, I believe that there is room for management to further reduce expenses if the anticipated revenue growth does not materialize.

Capital allocation

The company has deployed approximately $107.5 million towards share buybacks and repurchased nearly 20% of the shares outstanding since initiating the $200 million share repurchase program in February 2022. The program runs until February 2025 and the company has more than $90 million left to deploy. I expect management to continue to buyback shares aggressively as long as the business does not drastically deteriorate and shares remain at these depressed levels. It is possible that the company initiates a special dividend towards the end of the year if losses continue to reduce.

Thoughts on valuation

The company’s balance sheet consists of $381 million in cash and $18 million in debt. This results in a net cash position of $363 million which corresponds to $3.94 per share, assuming 92.1 shares outstanding. At the current share price of $2.5, its market capitalization is $235 million, which is a 35% discount to its net cash. The negative enterprise value assigned by the market is due to the growth stagnation and lack of profitability of the company. I however argue that the market is too pessimistic and that free cash flow has shown an improving trend in recent quarters as shown below. This is mainly due to restructuring and cost control measures by management that began early last year. The FCF burn over the last four quarters was reduced to $12.5 million and is expected to reduce going forward as revenue growth improves.

Q1 Investor Presentation

Besides its massive net cash position relative to its market cap, I would also like to point out that the underlying business which has an annual revenue run-rate of above $140 million, though unprofitable, could demand a valuation of at least $100 million. This valuation would still be at a large discount to peers such as Twilio (TWLO) and Sinch (OTCPK:CLCMF) that trade at Price to sales multiples of up to 2. Therefore I argue that downside is limited at the current valuation as long as the company continues to reduce its quarterly cash burn. If the company can successfully reach FCF breakeven by the end of next year, it will likely have more than $300 million in net cash, which is still considerably higher than its current market cap.

Risks

Lack of profitability

According to me the biggest risk facing investors is that the company fails to ignite revenue growth and therefore struggles to reach sustained profitability. In order to mitigate this risk, management needs to show that they can convert some of the current opportunities that were highlighted into revenue for the company.

Exposure to China

According to its latest Annual report, more than half its revenue came from China. This portion of revenue has faced headwinds over the last two years relating to regulations and a weak macroeconomy.

Competition

Agora faces competition from larger global players such as Twilio, Sinch and Bandwidth (BAND). It, however, has managed to differentiate itself by specializing in video related communication while its rivals focus more towards text and voice-based communication.

Conclusion

While acknowledging the risks identified, I believe the current valuation of the company reflects excessive pessimism and does not fully account for management’s efforts for reducing expenses and and improving margins. Although I find the current valuation appealing, I remain cautious and stay on the sidelines until I gain greater confidence in the company’s path to profitability.

Read the full article here

")

")

")

")