")

")

Written by Nick Ackerman, co-produced by Stanford Chemist

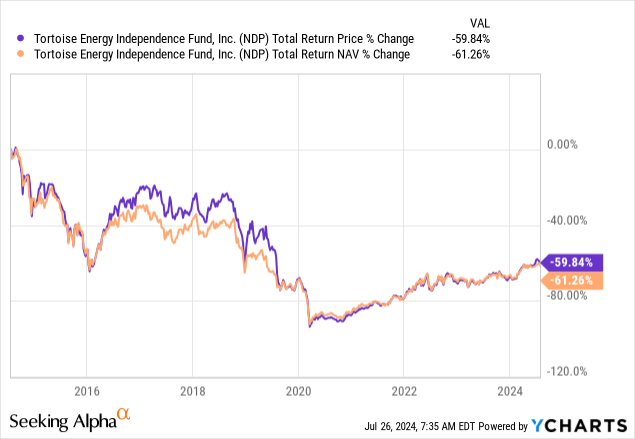

It’s been nearly a year since we last touched on the Tortoise Energy Independence Fund (NYSE:NDP). During this time, the fund delivered attractive total return results, and some of that was the result of the closed-end funds discount narrowing a bit. However, the majority of this was just driven by the strength of the underlying performance of the portfolio.

NDP Performance Since Prior Update (Seeking Alpha)

In fact, over the last three years, the energy sector has been the best-performing sector, which has helped to drive solid results for NDP these last few years. The energy sector could have some more room to run higher as well, as human civilization’s reliance on producing power only increases over time. That said, this is one fund that was damaged significantly during the Covid crash as they were highly leveraged.

Today, the discount remains attractive and could be worth considering—and running with less than half of the effective leverage should mean we shouldn’t get a repeat of a Covid crash. However, to be fair, any leverage will amplify results both up and down, so there is always a risk for greater losses with a leveraged fund due to increased volatility.

NDP Basics

- 1-Year Z-score: 1.19

- Discount/Premium: -12.00%

- Distribution Yield: 7.23%

- Expense Ratio: 1.93%

- Leverage: 13.20%

- Managed Assets: $77.1 million

- Structure: Perpetual

NDP seeks “a high level of total return with an emphasis on current distributions paid to stockholders.” To achieve that objective, the fund “invests primarily in equity securities of upstream North American energy companies that engage in the exploration and production of crude oil, condensate, natural gas and natural gas liquids that generally have a significant presence in North American oil and gas fields, including shale reservoirs.”

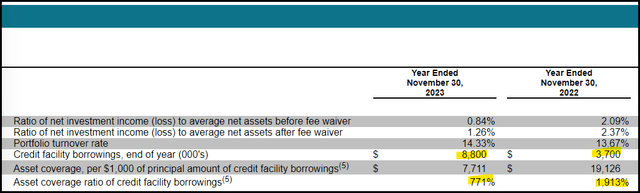

The fund’s expense ratio is quite high, and when including leverage expenses, the total expense ratio comes to 2.30%. That was an increase from last year’s 1.60% as borrowing costs have increased, as well as the amount of borrowings the fund has outstanding also increased.

NDP Leverage (Tortoise (highlights from author))

Since the end of the last fiscal year, borrowings are up further at $10.2 million as of the last report.

These leverage levels are still down from the $26.5 million on the credit facility outstanding that worked out to an asset coverage ratio of 332% compared to today’s asset coverage ratio of 752%.

The small size of this fund—being sub-$100 million in AUM—can make it difficult for larger investors to get into or out of the fund as the average daily volume comes to just 6647 shares.

Activist Pressure And Shake-Up Potential

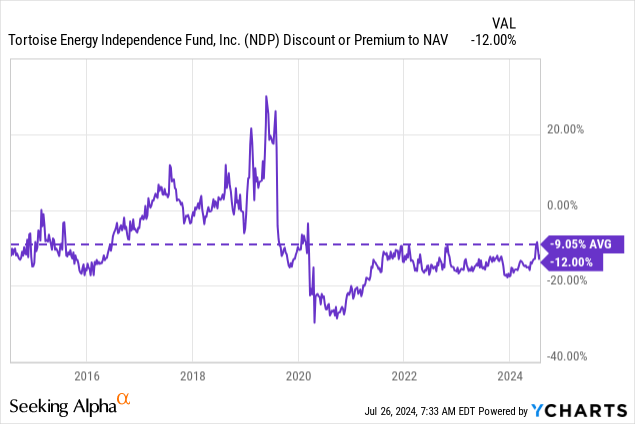

NDP is trading at a fairly attractive discount that is below its longer-term average. However, prior to Covid, the fund enjoyed a rich premium before its collapse. That collapse in the premium to a deep discount would have made the negative for investors that much worse going through Covid as the underlying fund itself was collapsing.

Ycharts

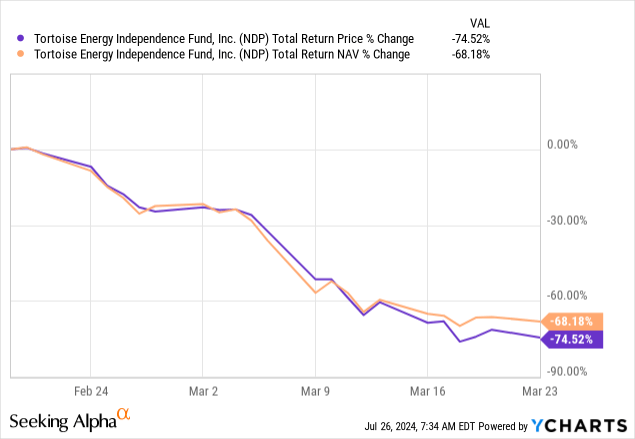

To get a sense of the drop, we can see the total returns during the Covid crash. This was from February 19, 2020, to March 23, 2020. The drop here was exacerbated by the fund’s high leverage at the time.

Ycharts

Going over the last ten years, the fund is still down but for those that bought during or shortly after the Covid crash, they are certainly going to see a different picture.

Ycharts

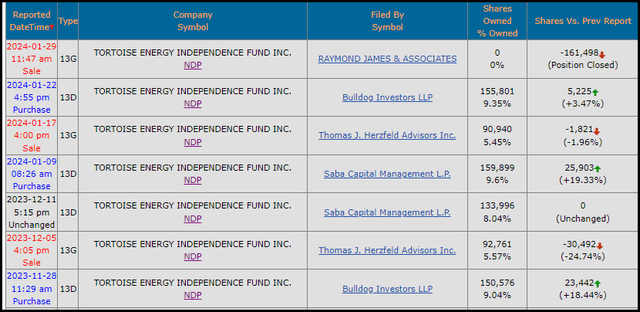

With all that being said, there is potential that NDP might get a bit of a shake-up. There are known activists in this fund carrying some sizeable positions, Bulldog Investors holds 9.35% of the outstanding shares, with Thomas J Herzfeld Advisors at 5.45% and Saba Capital Management At 9.6%. So, while being a smaller fund with low trading liquidity, it clearly hasn’t deterred these well-known and large institutional investors.

NDP Ownership (Secform4)

Further, there is another under-the-radar group that isn’t known for targeting CEFs, but they have also taken an interest in the fund. That would be ATG Capital Management, with the managing partner, Gabriel Gliksberg, looking to get a seat on the Board of the fund in the upcoming annual meeting set to take place on August 8th. Along with Gabi Gliksberg, they are hoping to also get Aaron Morris elected to the Board of NDP as well.

They are running up against a bit of a snag, though, as Tortoise has elected to reduce the Board size from 5 to 4 after one of the other independent members is retiring. Of course, that makes it more difficult to get activist representation during Board meetings if they can only elect one member instead of the two they were hoping to get.

In advance of the Annual Meeting, ATG has nominated two highly qualified candidates for election to the Fund’s Board of Directors (the “Board”)— Gabriel Gliksberg (“Gliksberg”) and Aaron T. Morris (“Morris”) (together, the “Nominees”). Pursuant to this Proxy Statement, ATG is soliciting proxies in favor of both Nominees, who will introduce fresh perspectives into the boardroom, as well as the proposals described below. We intend to vote all shares FOR the election of the Nominees to the Board and FOR the Proposals 2-5 below. We urge you to do the same.

We note that the Fund’s definitive proxy statement states that “[s]ince the Board has elected to reduce the total size of the Board of Directors to four members effective upon completion of the annual meeting, only one director nominee will be considered for election and you should vote for only one director candidate.” As discussed in further detail below, JID believes the Board’s stated position is legally erroneous and constitutes a breach of fiduciary duty, and has filed a lawsuit seeking, among other things, equitable relief allowing stockholders to elect directors to both Board seats available for election at the Annual Meeting. However, as stated in the GOLD proxy card and in the description of Proposal 1 below, in the event that it is determined that only one director may be elected at the Annual Meeting, all proxies on the GOLD proxy card will be voted for Gabriel Gliksberg unless such votes are to WITHHOLD as to Gabriel Gliksberg, in which case such votes will not be cast as to Proposal 1.

Along with ATG’s efforts to get elected members elected to the Board, Saba and Bulldog are also proposing some actions that shareholders can vote on.

Saba’s proposal 3:

RESOLVED, that the shareholders of Tortoise Energy Independence Fund, Inc. (the “Fund”) request that the Board of Directors of the Fund (the “Board”) take all necessary steps in its power to declassify the Board so that all directors are elected on an annual basis starting at the next annual meeting of shareholders. Such declassification shall be completed in a manner that does not affect the unexpired terms of the previously elected directors.

Bulldog’s proposal 4:

RESOLVED: The stockholders urge the board to consider measures to allow all shareholders to monetize their shares at a price at or close to net asset value (NAV).

Bulldog’s proposal here would indicate a tender offer, conversion to an open-ended fund or a full liquidation, as those are really the main ways to realize the fund’s NAV per share for investors. Being such a small fund already with under $100 million AUM would seem to make a tender offer not too appealing for long term investors. A merger with another Tortoise fund and then a tender offer could be an option. They had tried to merge this fund with Tortoise Pipeline & Energy Fund (TTP) previously, but that was unsuccessful.

We also have recently seen First Trust merge their energy infrastructure funds into an ETF wrapper, which is the FT Energy Income Partners Enhanced Income ETF (EIPI) now. That could also be a viable way of seeing shareholders realize NAV per share.

Combined, these large shareholders are likely to put some significant pressure on NDP as they own a sizeable sleeve of the outstanding shares.

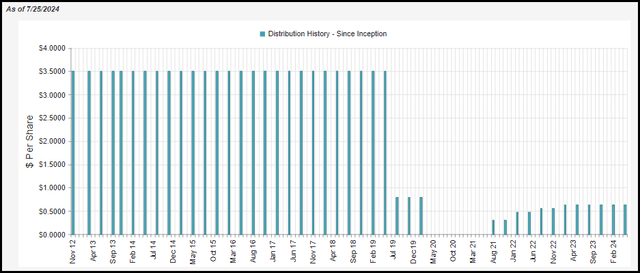

NDP’s Distribution

The fund’s current distribution works out to 7.23% and is paid quarterly. Thanks to the substantial discount, the NAV rate comes to 6.36%. Another highlight reflecting how bad things got for this fund during Covid is that they had actually suspended their distribution for a period after the crash.

NDP Distribution History (CEFConnect)

We covered its other sister fund recently, Tortoise Energy Infrastructure Corporation (TYG). Just like TYG, NDP has a 7-10% NAV distribution rate target—which also means like TYG, we could potentially see them announce an increase in the payout with the next declaration coming up soon.

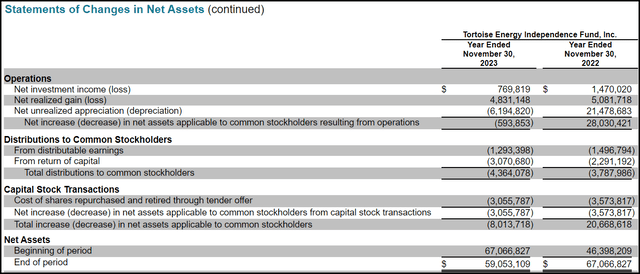

To cover the distribution, the fund will rely on capital gains as the net investment income isn’t sufficient to cover the entire payout. That isn’t dissimilar to most equity-focused CEFs. We should be getting their next semi-annual report sometime in the next few weeks, but here is a look at the figures from their last annual report available.

NDP Annual Report (Tortoise)

NII coverage here worked out to about 17.5%. However, similar to other energy-focused funds like its sister TYG, we can add back in return of capital distributions as they hold an allocation of MLPs and energy-related investments that distribute ROC themselves. For NDP, that would add back $966,317 and bring distributable cash flow coverage up to nearly 40%.

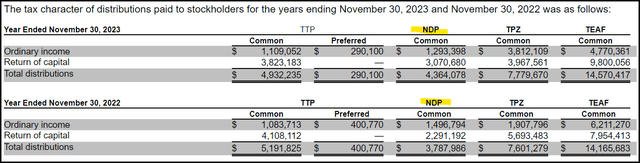

For tax purposes, we’ll see that return of capital show up as well. A portion of this would be considered non-destructive due to receiving the ROC distributions from the underlying investments. In particular, the last few years have been strong for NDP, and that has seen its NAV increase, meaning none should be considered destructive ROC.

Distribution Tax Classification (Tortoise (highlights from author))

NDP’s Portfolio

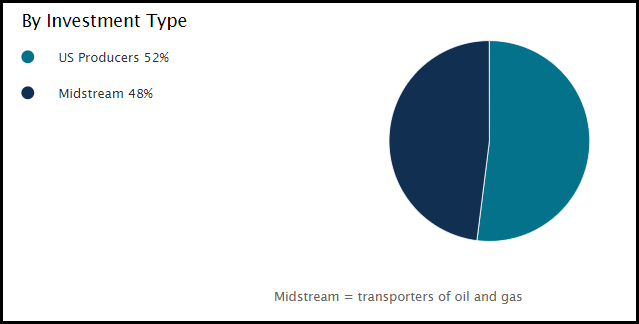

The turnover rate on this fund has been fairly low the last couple of years, coming in at 14.33% and 13.67% for fiscal years 2023 and 2022. That generally means we don’t see too many differences in terms of positioning on this fund between updates. Where NDP is a bit different is that it takes meaningful positions in producers and not just mainly midstream and MLPs like most of the other Tortoise funds. That can make NDP riskier than its peers.

NDP Investment Allocation (Tortoise)

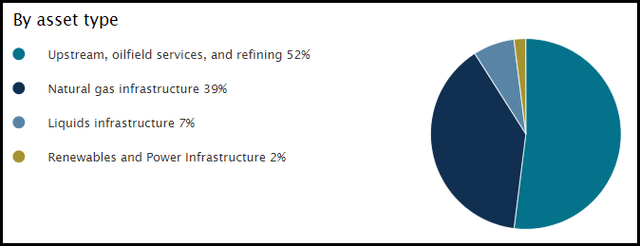

Within the portfolio are 81% allocated to common stocks, and 19% invested in MLPs. The largest asset type is “upstream, oilfield services, and refining” at a 52% weight. Of course, that’s reflecting the significant U.S. Producers’ sleeves also shown above.

NDP Asset Allocation (Tortoise)

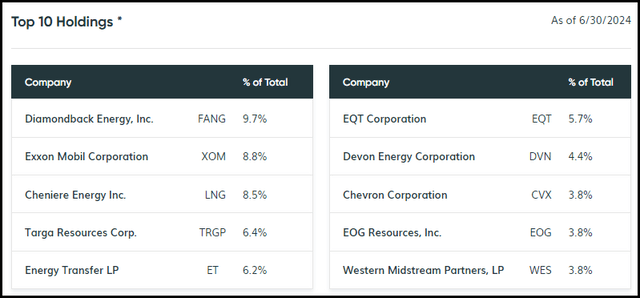

The top ten include some sizeable weights to each underlying investment. In fact, even just the top five represent nearly 40% of the fund’s total invested assets—with the entire top ten coming in at a 61.1% allocation.

NDP Top Ten Holdings (Tortoise)

This is another characteristic we see from most of the Tortoise funds and several other infrastructure-related CEFs is that they run more concentrated portfolios. A lack of diversification can sometimes be a positive, or it can be a negative.

If the management team is successful, it can be a big positive as the fund’s performance can benefit from potential outsized gains—assuming they are picking the right concentrated bets. However, the reverse of that is also true. A lack of different holdings means that a few going sideways can lead to outsized losses relative to benchmarks.

Conclusion

NDP is being targeted by several known activists and a not-so-well-known group as well. That could lead to a shake-up for NDP soon, and that is something investors in NDP should monitor as the annual meeting draws closer. Perhaps these efforts will be successfully thwarted by Tortoise, and business will continue as usual. That said, with a small fund, it can be quite difficult for any changes to be done, even if they are seemingly positive, like when they attempted to merge NDP and TTP together. So, one way or another, hopefully, investors will get out there to vote on what they believe is in the best interest of their investment fund.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")