")

")

Introduction

Adtalem Global Education (NYSE:ATGE) is due to report earnings on the 6th of August, and after a decent run over the last year, I wanted to take a look at the company’s financials to see if it would still be a good time to start a position. Even after a fantastic share price run, the company seems to trade at a decent discount, therefore, I am assigning the company a buy rating.

Briefly on the Company

Adtalem is a for-profit educational institution specializing in healthcare career progression. The company has under its wing Chamberlain University, which offers degrees in nursing and health professions in the postsecondary education industry. In the last few years, the company added Walden University, which offers online education for bachelor’s, master’s, and doctoral programs in a variety of different fields such as nursing, education, business, and psychology. It also has a Medical and Veterinary program which includes operations of the University of the Caribbean School of Medicine, Ross University School of Medicine, and Veterinary Medicine.

Financials

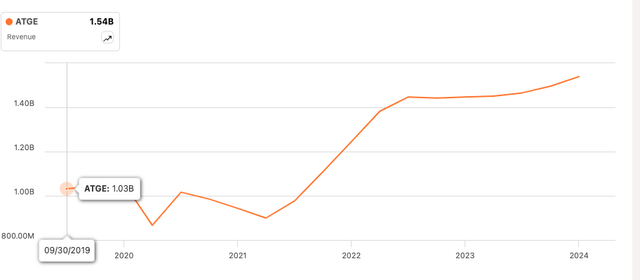

We can see the company’s revenues skyrocket sometime after mid-2021. This can be attributed to the company’s acquisition of Walden University primarily. Without it, the company would have had a decline of around 1% in total revenue since the other segments of the company experienced a decline.

Seeking Alpha

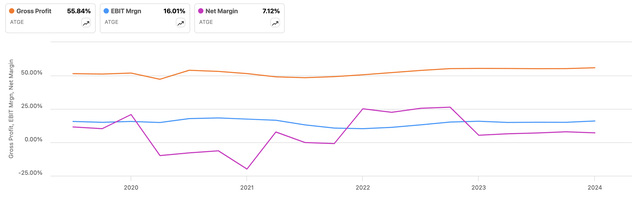

In terms of efficiency and profitability, the company’s margin profile has been somewhat consistent over the last 5 years, with a bit more jumping around on the bottom line, which is expected. Under GAAP terms, many non-cash items can affect the bottom line.

Seeking Alpha

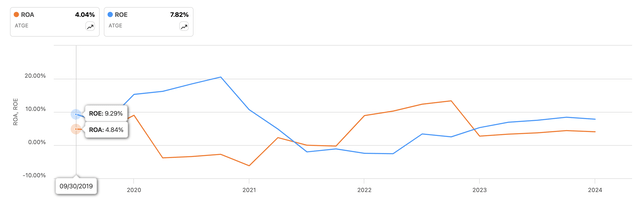

Unfortunately, the other efficiency and profitability metrics I like to look at have been trending down in the same period, which is not the end of the world, however, it does tell me that the company’s management is not utilizing the company’s assets and shareholder capital as efficiently as it had in the past. Even, then the returns weren’t very impressive.

Seeking Alpha

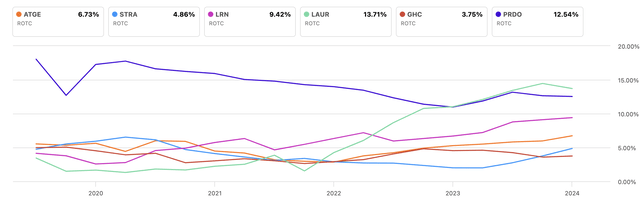

In terms of competition, I like to look at the company’s ROTC, or return on total capital, and compare it to its peers, however, the company with so many educational institutions, for-profit and not-for-profit that it would be tough to list them all. Therefore, I’ll just look at the default selection that SA offers on the site. I look for at least 10% (depending on the sector), which tells me that the company has some sort of competitive advantage, pricing power, and a strong moat. In the case of ATGE, we can see the company is somewhere in the middle of the pack, however, do note that its ROTC increased drastically from the lows at the end of FY21, therefore, I would like to see how it continues to develop over the next few quarters.

Seeking Alpha

Looking at the company’s overall financial situation, at the end of Q3 ’24, ATGE had around $180m in cash and equivalents, against $648m in long-term debt. That ratio would deter many investors who tend to avoid any company that may look overleveraged, but is this a problem for ATGE? Operating income came in at almost $62m while it paid $16.5m in interest expenses, which means its interest coverage ratio is around 3.7x. Many analysts consider anything over 2x to be healthy, therefore, according to them, the debt is manageable. However, I like to see at least a 5x, which allows for more variation in the company’s operations, for instance, when a company had a bad quarter or a year, an interest coverage ratio of 5x is much safer and will likely be sufficient in the bad times too. So, what I like to do in this situation is to discount the intrinsic value a bit more to be on the safer end.

Overall, I think the company’s operations are decent. The margins have been steadily increasing over time, revenue growth was helped by the acquisition, which isn’t a bad thing. The company’s efficiency metrics could be slightly better in my opinion, as well as the company’s financial position, which isn’t bad but not as safe as I would like it to be.

Comments on the Outlook

So, let’s quickly cover what could be the drivers of the company’s top-line growth above what it had experienced in the previous year. Since the acquisition of Walden, the company saw 5% growth y/y, which isn’t particularly high, however, since Q1 ’24, the company saw its top-line growth accelerating, going from around 5% in Q1 to over 8% in Q2 and around 12% in Q3. The strength of Walden and Chamberlain Universities were the primary drivers of growth recently, and the management expects this to continue throughout the remainder of the year and even into 2025. This is evident in the company’s increased guidance for the year-end to $1.56B-$1.58B for revenues, which is around 8% y/y growth, and an increase in EPS range to $4.80-$5.00. The company has a lot of confidence in its ability to market the programs effectively and it has paid off in the last couple of quarters. What I also think will help ATGE and many similar for-profit institutions is an increase in the unemployment rate across the US. The economy has been much more resilient than anyone expected when the FED started to raise interest rates to combat inflation. However, slowly we are seeing the unemployment rate tick up right now and as of June 30th, the rate stood at 4.10%, up 10bps from the previous month. If it continues to tick up, I will say there will be a positive effect for educational institutions that are offering hybrid models to upskill and will drive more enrollments if people are getting laid off.

With the pandemic event, there is a need for a lot more medical staff in the US. ATGE being the leader in the sector stands to benefit the most when it comes to upskilling the community and taking up important medical roles that are so vital to the future of medicine in the US. It is said that the US will have a big shortage of medical staff going forward, which will reach around 124,000 physicians by 2033. The pandemic played a huge role in this problem. A lot of people were put off by nurse and doctor positions due to burnout, and long hours because of the said shortages, so ATGE has a lot of work ahead for themselves to lessen the issue as much as possible. This means marketing the courses as much as they can to attract many more people to fill the roles.

In terms of margins, I think these are already quite decent, so anything extra would be great but if they remain stable going forward, it’s not a bad thing. In the latest transcript, the management did mention they expect margins to remain as they are for a little while, which already saw good improvement y/y, but in the long run, they expect margins to continue to expand, going into ’25 and ’26. With all this information, let’s look at some valuation assumptions, to see what the company is worth to me.

Valuation

For revenues, I went conservative, as I usually do. For the base case scenario, I went with 8% growth for FY24, which will taper off to 5% the next year and continue down to around 3% by FY33. This way the company will see a 5% CAGR over the next decade, which I think is more on the conservative end.

Author

For margins and EPS, I matched the margin profile to what the company expects to get for FY24 in terms of EPS. As mentioned, the range was $4.8-$5.0 a share, I went with $4.86 a share for FY24. From then on, for conservatism’s sake, I stuck with the static margins going forward, even though the company expects margin expansion in the long run. This way, I am getting more room for error in estimates, and it is better to be safe than be overly optimistic about the company’s prospects. It’s good to take the management’s comments with a grain of salt than at face value.

Author

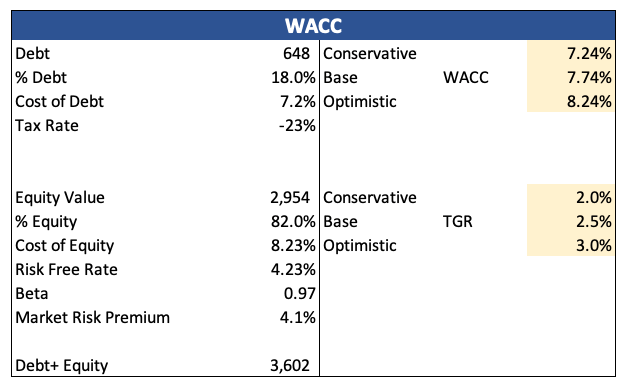

For the DCF analysis, I went with the company’s WACC of 7.7% as my discount rate, and 2.5% as my terminal growth rate because I would like the company to at least match the US long-term inflation goal.

Author

Additionally, as I mentioned in the first section, due to the company’s rather higher debt, which comes with a high interest rate, I decided to add a discount of 25% to the final intrinsic value, to be on the safer side. With that said, ATGE’s intrinsic value, with static margins and rather low revenue growth, is around $96 a share, meaning even after such a great year, the company is still trading at a discount.

Author

Risks to Consider

In the short run, the recent stock price performance, up around 80% in a year, may force some profit-taking, especially if the next few quarters are below expectations. This is only a short-term noise, which is a blessing as you could buy at even better prices if you are long-term-oriented.

To derail this bullish sentiment, the company’s margins would need to show weakness over the next couple of quarters, as that is the main reason the company’s valuation is so high.

Investors will also pay attention to the headline item, which is enrollment. If we see a meaningful dip, it means the company’s marketing efforts are not paying off or people are not interested in the medical field due to the aforementioned burnout risks and long hours of toil. I will monitor the company’s quarterly press releases to see if anything drastically changed and needs to be adjusted within the model.

As I mentioned, the competition is fierce, which means the company’s efforts to market itself will be of priority. If it fails to attract more people to enroll, we will see a deterioration in operations, and the share price will follow.

Closing Comments

Nevertheless, it seems that the company is trading at a decent discount even after such a great performance over the last year. Even with my conservative estimates, the company is a bargain. I will look at the upcoming few quarters to see how the top-line growth and margins progress, but if everything is fine, I will be considering opening a position because the risk/reward seems very enticing right now.

Read the full article here

")

")

")

")