Q4 2024 Earnings Call Transcript")

Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company (“BDC”) sector from both the bottom-up – highlighting individual news and events – as well as the top-down – providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the last week of August.

Market Action

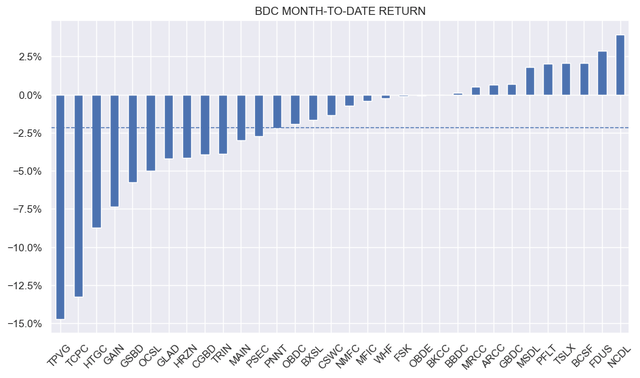

BDCs had a good week with a total return of around 1%. For August, however, the sector finished around 2% lower. Six out of the top eight performers on the month were our holdings which was good to see (out of 8 our overall BDC holdings).

Systematic Income

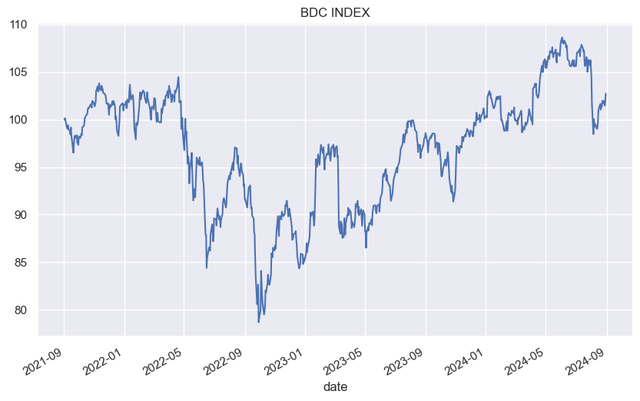

The sector continued to climb out of the early-August drawdown.

Systematic Income

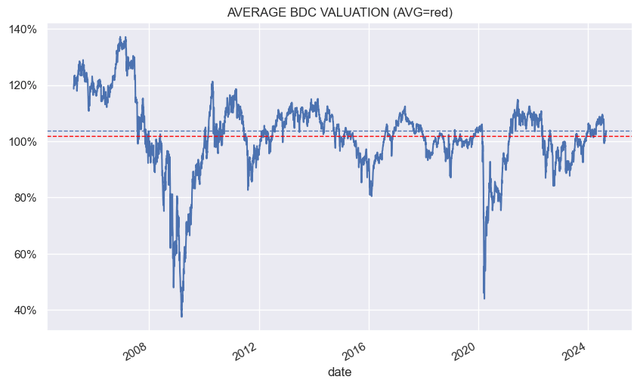

The average valuation once again moved above its longer-term historic level.

Systematic Income

Market Themes

Private lenders are taking ownership of Pluralsight. The group which includes the larger BDCs is putting in an additional $275m of capital into the company in the form of new loans. The existing debt is restructured into equity. This outcome was communicated in recent earnings releases and was entirely expected. It’s not clear where the new equity holdings will be valued – the loan was marked a touch below 50% in Q2.

JP Morgan was recently looking to sell the debt to interested parties so existing lenders may be looking to lighten their exposure. The overall experience is a good one for the private credit market. Recall that the sponsor Vista shifted the collateral into a related subsidiary to raise additional debt in order to pay interest on the existing debt. This kind of thing had the look of lender-on-lender violence where new creditors shaft the old ones; however, it ended up being much more benign than that. Apparently Vista wanted to raise additional capital to pay the interest to existing lenders rather than to try to pit one group of lenders against another.

There is some upside hope for the lenders if they manage to turn the business around. Recently, a number of BDCs such as TRIN and BBDC closed out their Core Scientific loans at a gain after CORZ defaulted on the original loans and the loan was converted to equity. The lenders then lucked out on a gain in the bitcoin price which allowed CORZ to emerge out of bankruptcy and for the lenders to sell their equity at an overall gain. This was more a stroke of luck rather than a brilliant behind-the-scenes example of a corporate turnaround.

Overall, the Pluralsight event is not a bad result. For one, what actually happened was not an example of lender-on-lender violence as was originally suggested in the press. And two, because the original loan was not as watertight as would be ideal, private credit lenders have taken notice and their comments in the wake of the deal suggest that documentation will tighten going forward in order to prevent this from happening again.

Market Commentary

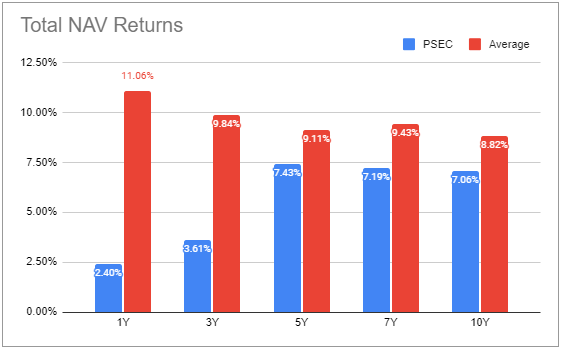

Prospect Capital (PSEC) delivered poor results. Total NAV return for the quarter was -0.8% vs. 2.2% median in the sector. Over the past few years the stock has generated more fees for its managers than it has delivered for investors which is not the way it’s supposed to work.

An underperforming quarter by OCSL (which was still 1% better than PSEC) caused management to lower its fee to 1% on total assets. PSEC is earning twice that and it’s not doing anything about it as management think it’s perfectly fine to consistently and massively underperform the sector while earning a fee that’s miles higher than the average.

In the past year the stock underperformed the median BDC in coverage by more than 10% and by 7% per annum over the last 3 years in total NAV terms. It’s hard to have a rational discussion of whether it’s a buy or not because the performance is simply too low to justify even its 43% discount. Investors who think it’s a buy right now need to have an argument of why its performance will turn around.

Systematic Income BDC Tool

Stance And Takeaways

The average BDC sector valuation moved past a 5% premium and now stands above its historic average. Given this continued richening we have not added to our BDC portfolio since it was topped up in the first half of August due to a number of very attractive opportunities. We continue to see value in BCSF, FDUS and OBDE however a number of other opportunities have seen their mid to high-single-digit discounts almost vanish in the most recent rally.

Check out Systematic Income and explore our Income Portfolios, engineered with both yield and risk management considerations.

Use our powerful Interactive Investor Tools to navigate the BDC, CEF, OEF, preferred and baby bond markets.

Read our Investor Guides: to CEFs, Preferreds and PIMCO CEFs.

Check us out on a no-risk basis – sign up for a 2-week free trial!

Read the full article here

Q4 2024 Earnings Call Transcript")

")

")

")

")