")

")

With decarbonisation urgently required to ensure climatic stability, green finance has naturally become a high growth sector. According to Arup and Oxford Economics research, it will be a USD 152 billion opportunity by 2050, growing by 7.2x from 2020. This underlines the potential for the Canadian investor in renewable energy Brookfield Renewable Partners (NYSE:BEP), with over USD 100 billion in AUM (see Slide 5 of the link).

Despite the potential however, the company’s stock, has seen underwhelming long-term price trends. The price is up by just 27% over the past decade. Over the past five years, the trends are even worse, with the price remaining virtually unchanged, with gyrations in the interim.

The past, however, over the longer-term might not be a good indicator of how the future will progress. Here are four reasons why.

#1. The promise of renewable energy

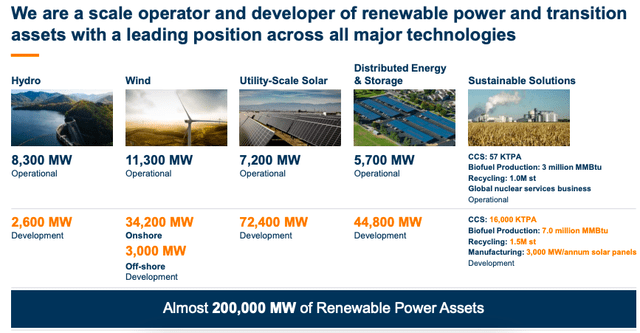

The company that buys renewable energy assets, enhances their value and then re-sells them, has a significant portfolio across the green energy spectrum. It has 200 GWh of assets in operation or under development (see graphic below). For context, this accounts for over 5% of global renewable energy capacity in 2023.

If renewable energy capacity were to continue expanding at the rate of 14%, as seen in 2023, by 2030 the absolute number would be at 9.7 TWh. If Brookfield were to maintain its current levels of contribution to it, its capacity would rise to 500 GWh capacity by 2030, up by 2.5x from the current levels.

This isn’t inconceivable, particularly as growing demand is backed by the policy push toward clean energy sources. For example, the company holds 61% of its assets in North America and mentions that it stands to benefit from policies like the Inflation Reduction Act, which provide incentives to the sector.

Source: Brookfield Renewable Partners

#2. Growing revenues and FFO

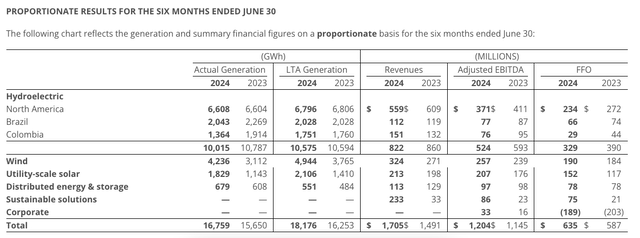

With this as the backdrop, it’s hardly surprising that the company’s latest earnings report released last month, is positive. For the first half of 2024 [H1 2024], its revenues grew by 17.3% year-on-year (YoY), driven by gains in its wind, solar and sustainable solutions’ portfolios (see table below), while hydroelectricity showed revenue contraction due to smaller actual generation compared to H1 2023.

The company’s earnings measures also increased, albeit to a smaller extent. The adjusted EBITDA was up by 5.1%, while its funds from operation [FFO] rose by 8.2% YoY. The company attributes this increase to “asset development, recent acquisitions, and strong all-in pricing.” Much like in the case of revenues, all segments save hydroelectricity, showed an increase in FFO.

Source: Brookfield Renewable Partners

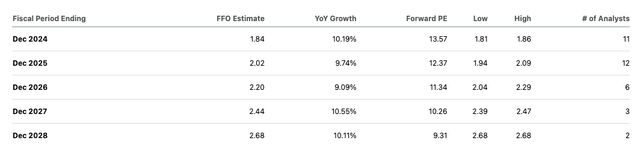

The company’s prospects look good too. The average of analysts’ estimates on Seeking Alpha brings the compounded annual growth rate [CAGR] for revenues at 9.1% between 2024 and 2028. This is slightly higher than the past five years’ CAGR of 8.7%. The FFO is expected to rise annually by ~10% as well (see chart below), with growth pencilled in for each of the next five years.

FFO Projections (Source: Seeking Alpha)

#3. Robust dividend payouts

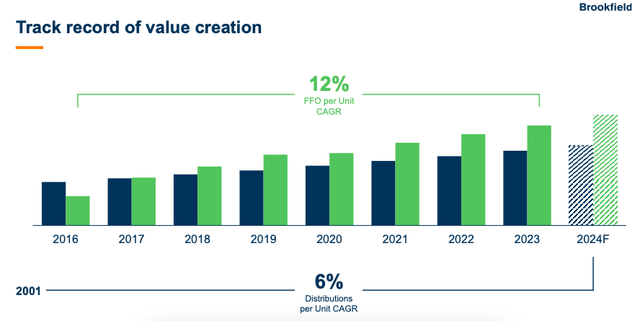

Next, even though BEP’s price returns have disappointed over the long-term, the total returns aren’t bad at all, at 171%, driven by its solid dividends. These have been supported by a CAGR of 12% in FFO in the past ten years, allowing it to increase the dividends at a CAGR of 6% as well.

Source: Brookfield Renewable Partners

Not only are FFO forecast positive, the company aims to increase distributions each year between 5% to 9% as well. This suggests that it can continue to be a rewarding stock for dividend investors. Its trailing twelve months [TTM] dividend yield at 5.6% is already higher than the average of 3.6% for the utilities sector. Also, expectedly, the forward dividend yield is slightly higher at 5.7% compared to the TTM yield as well.

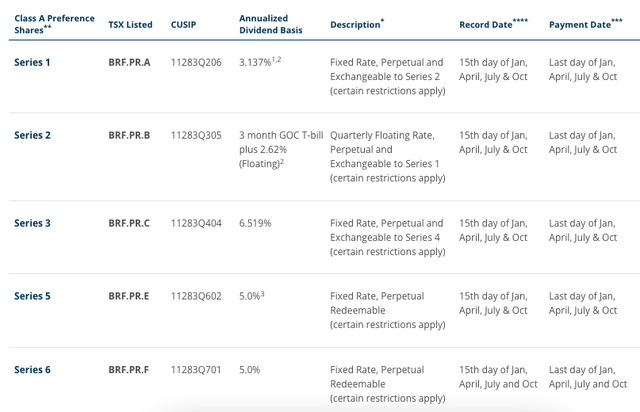

Additionally, the company also has multiple preferred share listings like (TSX:BEP.PR.R:CA) (TSX:BEP.PR.G:CA), along with others (see table below), with dividend rates ranging between 3.1-6.5% as well as one tied to the Canadian government’s T-bill rate, which comes to a rate of over 7%.

Preferred Stock Listings’ Dividend Rates (Source: Brookfield Renewable Partners)

#4. Favourable market multiples

With FFO increases forecast, the forward Price-to-FFO (P/FFO) ratio naturally significantly improves over time. From 13.5x for 2024, it declines to 9.3x by 2028.

With the company making net losses, however, it’s not directly comparable with similar stocks. In lieu of the P/E, the EV/EBITDA is considered here instead. BEP does look overpriced from this perspective, with a forward EV/EBITDA at 25.2x compared to Clearway Energy (CWEN) at 12.3x and Atlantica Sustainable Infrastructure (AY) at 9.5x.

Investing Takeaways

Short-to-medium term

The comparative EV/EBITDA levels don’t bode well for BEP in the short-to-medium term, implying that the stock can continue to decline. This can change, if its FFO were to rise faster than envisaged right now. But based on the data available, there’s no reason to believe so.

It bears mentioning, though, that a higher EV/EBITDA doesn’t reflect that BEP is heavily indebted. The company’s latest net debt-to-assets ratio is actually at a manageable ~39%. At the same time, the fact that its net loss making does make it less attractive and adds to reasons as to why the stock can continue to soften for now.

Long-term tip

However, over the longer-term its prospects look rather good. The company functions in the fast growing green sector, and as a spillover from that green finance is expected to increase multifold in the next decades. It’s past revenues and FFO have seen growth over time and the forecasts for future growth are positive as well.

The stock’s P/FFO is seen progressively improving over time as well. This also bodes well for its dividends. At the current price levels, its dividend yield also looks attractive and with dividends expected to continue rising with increasing FFO and according to the company policy, it should continue to be a good dividend stock. Based on this, for the long-term BEP is a Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q4 2024 Earnings Call Transcript")

")

")

")