Q4 2024 Earnings Call Transcript")

")

Introduction

Not many SPACs that have gone public have been as successful as Vertiv (VRT) has been in recent years. Since its IPO, it has managed to increase in value from $10 to over $100 in just over 4 years. Obviously, these returns cannot be coincidental, and there must be something behind this growth. Vertiv benefits from one of the biggest current macro trends, which is the transition to the cloud. However, from my point of view, it also benefits from another trend that the market doesn’t consider as much: hybrid environments.

In this article, we will delve into this company’s interesting business model and the macro trends supporting its future. I don’t think it’s the safest option for gaining exposure to its sector, but I certainly believe it’s worth giving it a chance. If you manage to buy it at a good price and the execution is good, we could obtain very good long-term returns.

Cloud vs Hybrid Environments

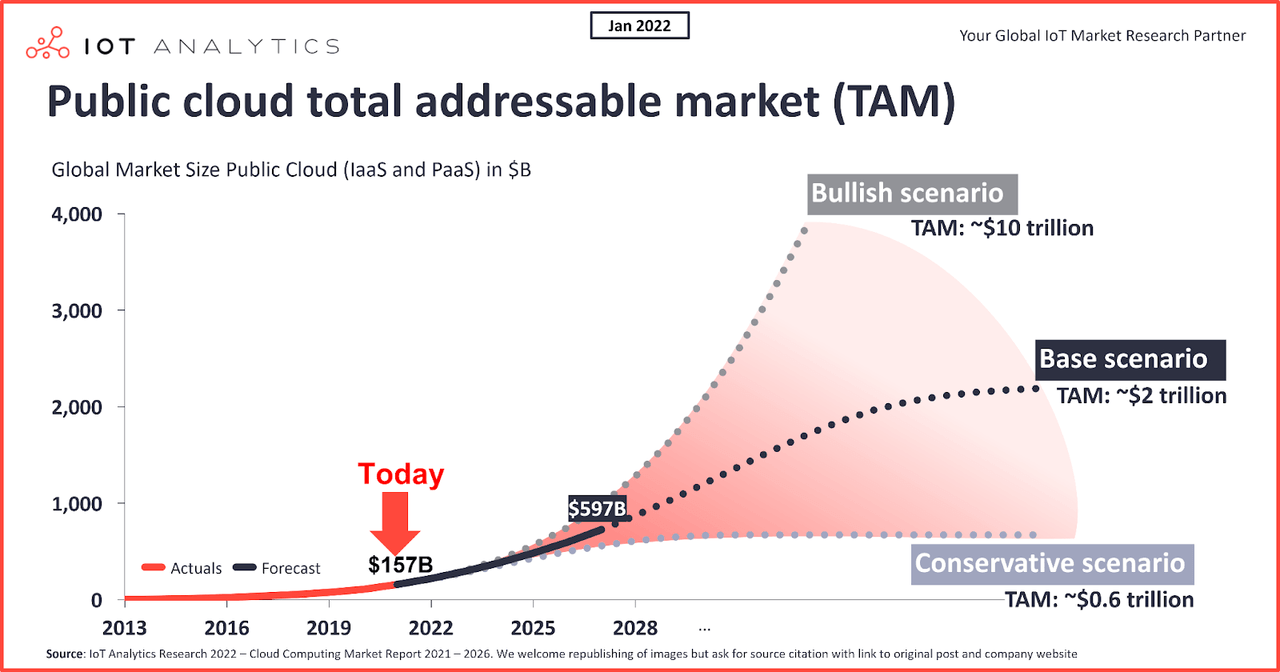

Surely you’ve heard about the advantages of transitioning to the cloud for businesses: cost savings, increased security, scalability, simplicity, and a long list of other benefits. Almost any estimate you look at projects double-digit growth in the coming years, as shown in the following image, which predicts that this market could reach $2 trillion in the baseline scenario and up to $10 trillion in the best estimates.

IOT Analytics

But what if I told you that the cloud isn’t as wonderful as it may seem at first glance? The advantages of the cloud are clear, but the transition to it isn’t as easy as it appears. In many cases, the cost isn’t worth it, and in others, organizations simply don’t want to host their most critical services on external servers. Don’t believe me? Take a look at this news from the end of last year, where LinkedIn canceled its migration to Azure due to difficulties in the process. If LinkedIn itself finds that migrating to the cloud isn’t entirely profitable (remember, it’s part of Microsoft), imagine how it might be for other companies.

Additionally, there are other issues, especially concerning data privacy. There are many services where it makes perfect sense for them to be in the cloud, but there are also many companies and governments that are not thrilled about having their data stored on some company’s servers. No matter how secure those servers are, you’re ultimately allowing an external company to have control and access to sensitive organizational data over which you have no control.

From my point of view, we’re heading towards hybrid environments where most organizations will have part of their data and services in the cloud and another part locally. There isn’t a “best solution”; each service of each organization has its unique characteristics, and it will make sense—or not—to transition to the cloud depending on those characteristics.

Nutanix

Therefore, although I am very positive about the cloud in the long term, I believe that hybrid environments will end up prevailing in most cases. Under this thesis, Vertiv, due to its characteristics, has an even larger market to expand into than just the cloud, as we will see below in its business model.

Business Model

Vertiv’s business model is organized into three main segments:

Critical Infrastructure & Solutions (CIS)

This segment is the largest and most significant for Vertiv, accounting for a substantial portion of their revenue. It primarily involves the design, engineering, and manufacturing of critical power, thermal management, and IT infrastructure solutions. These products are essential for maintaining the continuity and reliability of critical operations in data centers, communication networks, and other high-availability environments. Vertiv’s CIS products include uninterruptible power supplies (UPS), thermal management systems (cooling), power distribution units (PDUs), and modular infrastructure solutions.

Services & Software Solutions (SSS)

Vertiv’s Services & Software Solutions segment offers a comprehensive range of maintenance, repair, and support services, as well as software for monitoring and managing critical infrastructure. This segment is crucial for ensuring that the installed base of Vertiv products operates efficiently and reliably over time. The services range from preventive maintenance and emergency repair to remote monitoring and management through advanced software platforms. This segment also plays a key role in providing customized solutions to clients, helping them optimize their infrastructure and improve operational efficiency.

Integrated Rack Solutions (IRS)

The Integrated Rack Solutions segment focuses on providing complete and integrated solutions that combine power, cooling, monitoring, and management within a single rack or a small cluster of racks. These solutions are particularly relevant for edge computing environments, where space, power, and cooling efficiency are critical. Vertiv’s IRS offerings include pre-configured and modular racks that can be quickly deployed and scaled to meet the specific needs of small data centers, remote offices, and other distributed IT environments.

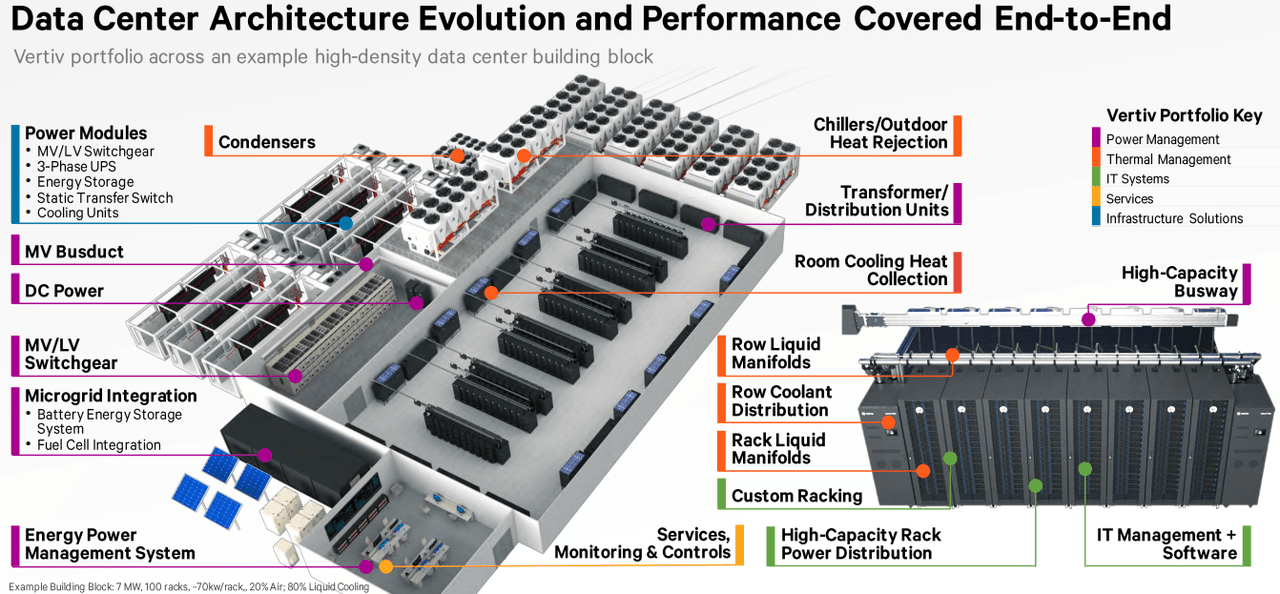

In the following diagram provided in their investor relations, you can see a data center and how the infrastructure and services offered by Vertiv play a key role in powering, cooling, securing, and maintaining it.

Vertiv IR

This is where the hybrid environments we discussed earlier come into play. All server infrastructure, both cloud and on-premises, requires the products and services that Vertiv offers. Therefore, if we add the already enormous demand from cloud providers like Amazon or Microsoft to the demand that organizations will have for their own local servers, we are looking at a market that can capitalize significantly on this trend. Having infrastructure both on-premises and in the cloud will eventually lead to redundancy and underutilization of servers, especially on-premises, which generally results in a kind of “diseconomies of scale.” This situation makes the overall spending on Vertiv’s infrastructure higher than it would be if everything were consolidated in the cloud.

Obviously, the key to this thesis is the enormous spending on cloud infrastructure that will continue to grow in the coming years and will undoubtedly be the main driver of sales. However, I believe the market may be underestimating this extra spending that could come from organizations themselves, which could push results above the estimated levels.

One advantage of this sector is that the products represent a small portion of the total cost of a data center, and they do not add much final value. This brings two positive aspects for Vertiv: first, an increase in their prices has little impact on the final cost for their customers, and second, the incentives for customers to vertically integrate are very low.

Capitalizing on the Investment in AI

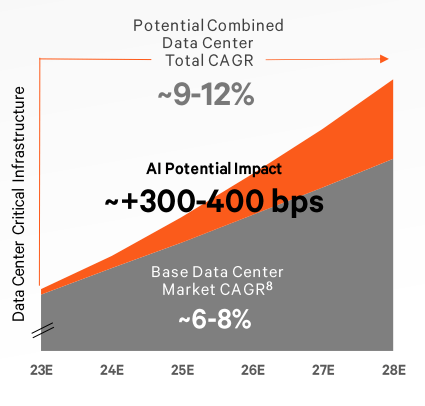

On the other hand, the other pillar supporting this thesis is AI. Vertiv is making smart moves by partnering long-term with Intel and Nvidia to design specific solutions for their products. This is undoubtedly very interesting because the electrical consumption for AI training, as well as the heat emitted by servers dedicated to this, is much higher than in traditional servers, which is driving demand for these products and requiring new solutions that Vertiv is capitalizing on. In fact, they estimate that the extra demand from AI could increase their top-line growth by up to 4% compounded annually more than without it.

The most interesting aspect for me is the contracts we’ve already mentioned with companies like Nvidia. If they manufacture specific products for Nvidia’s GPUs, Vertiv will be able to capitalize on Nvidia’s sales growth with minimal effort since their auxiliary systems are essential for maximizing the performance of the GPUs. If Nvidia provides the brains for data centers, Vertiv supplies the rest of the body, responsible for powering them and maintaining optimal operating conditions.

Vertiv IR

Financials

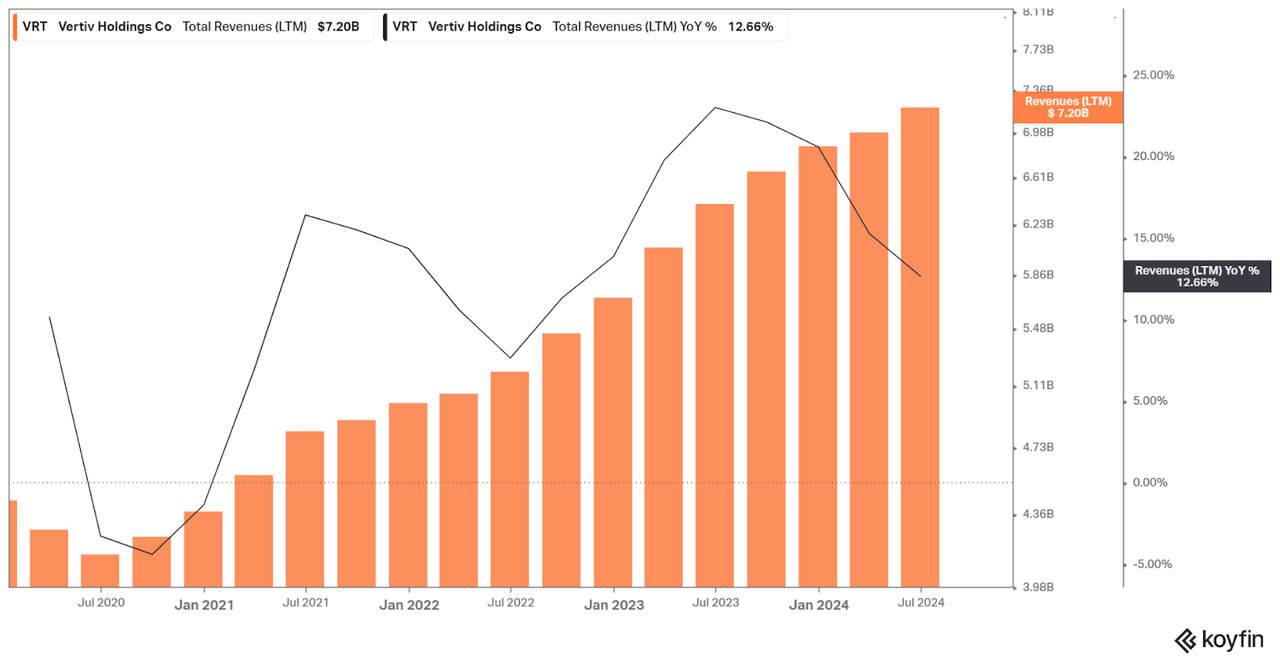

We don’t have an extensive history to review in Vertiv’s finances, as it started trading just a few years ago. However, we can see that revenue growth has been quite remarkable, with most quarters showing an increase of over 10%. Since their revenue mainly depends on the capital expenditure of other companies, it’s logical that revenue will tend to show some cyclicality. However, the important thing is that over time, these cycles will have higher peaks and troughs, thanks to the strong macroeconomic trend supporting them. Currently, sales are slowing down, and it’s expected that this trend will continue for a few more quarters, but I believe we’ll see a positive shift by early 2025. Additionally, they have a backlog of over $7 billion, which represents more than a year of current revenue.

Koyfin

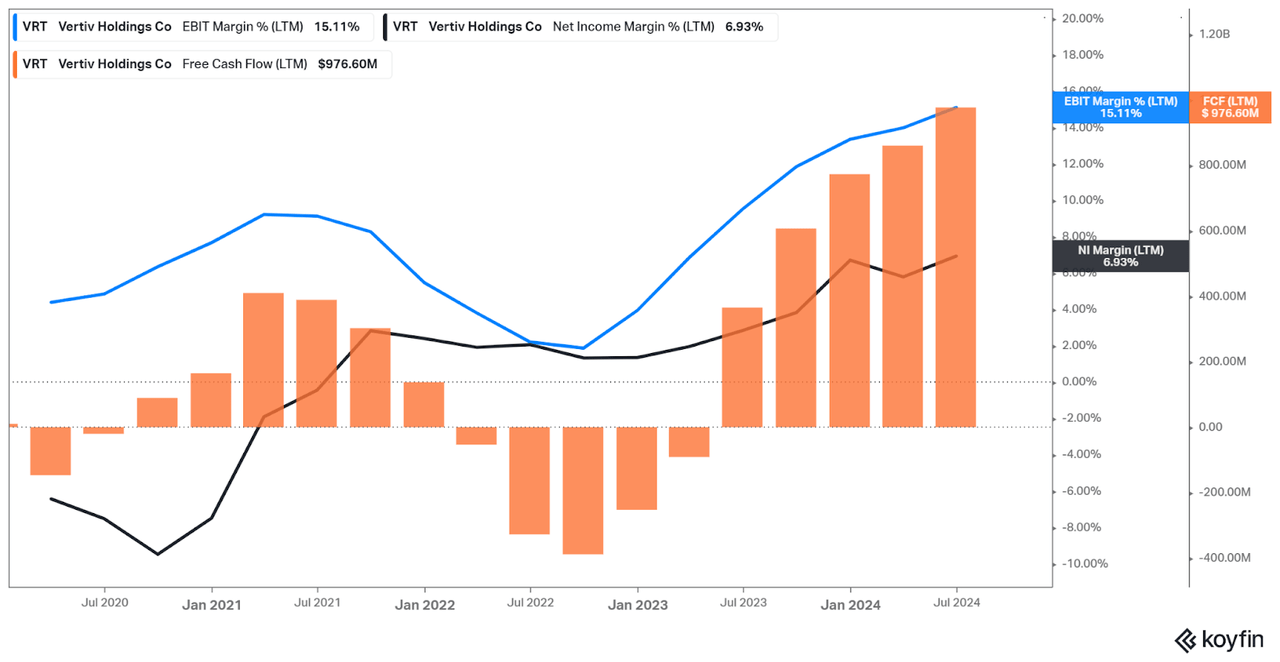

The best part, without a doubt, is how they are successfully converting this growth into cash flow for shareholders. As we can see from about three years ago, the business was generating losses, but thanks to operational leverage, it seems they have managed to cross the profitability threshold, and this should continue to improve gradually. Therefore, it’s likely that earnings and free cash flow per share will grow faster than revenue in the coming years. Their guidance is to surpass a 20% operating margin by 2028, which I believe is very possible if they maintain the expected growth.

Koyfin

Returns on capital have only recently started to turn positive, so I don’t think it makes much sense to focus on them just yet. If we look at the returns of some comparable companies like Arista (they’re not 100% comparable, but I think it serves as a good example), I estimate that they could achieve returns on invested capital above 20%. On the other hand, regarding the debt, it’s currently below 2x Net Debt / EBITDA, which is their long-term target. As long as it stays below this level, I don’t think we need to worry too much.

Valuation and conclusions

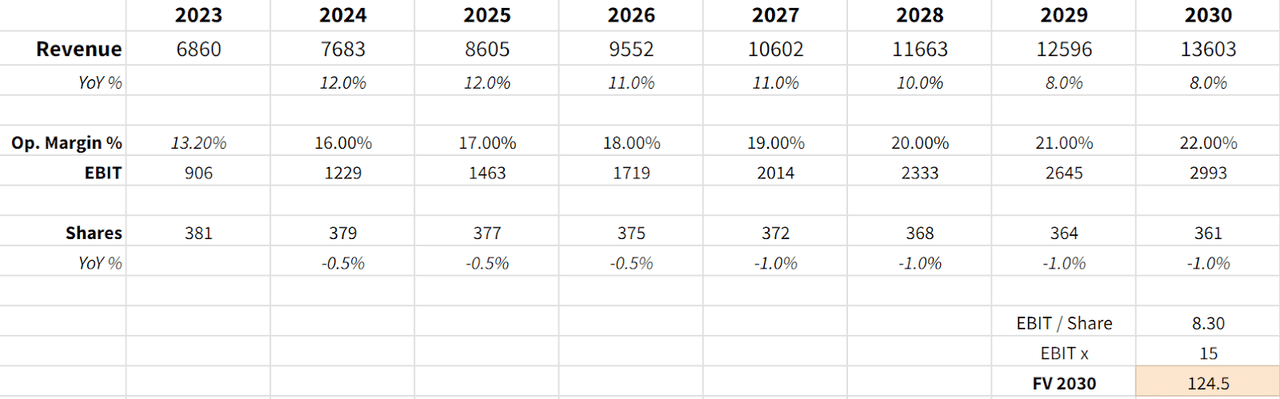

For my valuation, I have decided to partially follow the company’s guidance and analysts’ estimates, while being conservative with the final multiple. Given that the conversion between EBIT and FCF is between 95-100% and is expected to remain so, we will use EBIT as the metric to value the company, which I find fair. The projected revenue growth, both from the company and the consensus of analysts, is between 8-11%, so I have decided to use these figures, with a higher rate in the early years, gradually decreasing as the market matures, but still within this range of estimates.

As for the margin, we have mentioned that they expect to reach 20% by 2028, and I have estimated something slightly higher for 2030. Shares outstanding have already begun to decrease in recent quarters due to profit generation, and I estimate that this will continue, with at least 0.5-1% of shares potentially repurchased annually if the valuation does not become excessively high. I have decided to use a 15x EBIT multiple as it is in line with the company’s average trading multiple during its short life, and although it is lower than other comparables such as Arista (ANET), I believe that a discretionary business with some cyclicality like this should not be valued with significantly higher multiples.

Using this 15x multiple on that EBIT, the stock could be around $120-130 by 2030. From the $77 it is trading at the time of writing this, it implies a compound annual return of 8%, which seems rather modest for a company that has just begun to generate profits in such a dynamic market.

Author’s calculations

Personally, the minimum return I require from my investments is 10% for more stable and predictable companies, and slightly higher for riskier companies like this one, where I require a minimum of 12-15% to allow for a greater margin of error in case the thesis fails. Therefore, to demand a 13% annual return by investing in this company, we would need to buy it around $60-65. By being conservative with the numbers we project, the multiples, and allowing for a margin of safety like this, I believe we can minimize the risk when investing in companies with above-average market risk, without sacrificing good long-term returns.

It is also true that we could be more optimistic about Vertiv’s future, as I think there are reasons to be, but I believe it’s better to be conservative and focus on preserving our capital.

In summary, I think Vertiv is a very interesting company that will benefit from the development of AI, hybrid environments, and cloud development worldwide. It’s not a sure bet, but I think it’s worth considering if it reaches better price levels. I don’t think there’s a need to sell, as we are not in extreme overvaluation, which is why I’ve decided to assign it a ‘Hold‘ rating.

Read the full article here

Q4 2024 Earnings Call Transcript")

")

")

")

")