")

Today, we put First Interstate BancSystem, Inc. (NASDAQ:FIBK) in the spotlight for the first time. This traditional bank holding company has seen some recent insider buying in its stock. The shares also carry a big dividend yield. An analysis follows below.

Seeking Alpha

Company Overview:

This bank holding company has been around since 1971 and is headquartered in Billings, MT. The company through its 304 branches offers a range of banking products and services such as checking, savings and time-deposits to individual as well as loans. It also provides a variety of different loan and other products to small and mid-size companies including in commercial real estates, agricultural, etc. The stock currently trades just over $30.00 a share and sports an approximate market capitalization of $3.1 billion. The bank had just over $30 billion in assets and $22.9 million in deposits as of the end of the first half of 2024.

Second Quarter Results:

The bank posted its Q2 numbers on July 25th. First Interstate BancSystem, Inc. delivered GAAP earnings of 58 cents a share, three pennies a share above expectations. Net income was $60 million in Q2. Revenues did decline nearly seven percent on a year-over-year basis to $244.3 million, almost $2 million below the consensus.

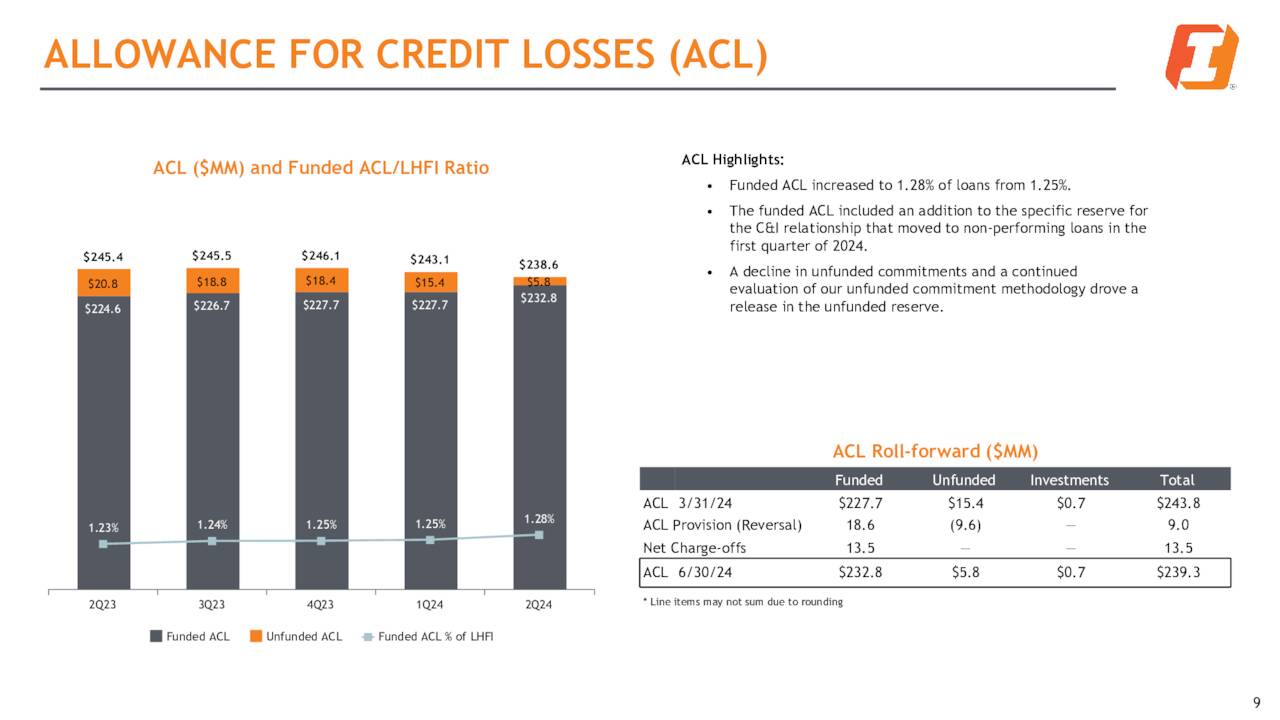

July 2024 Company Presentation

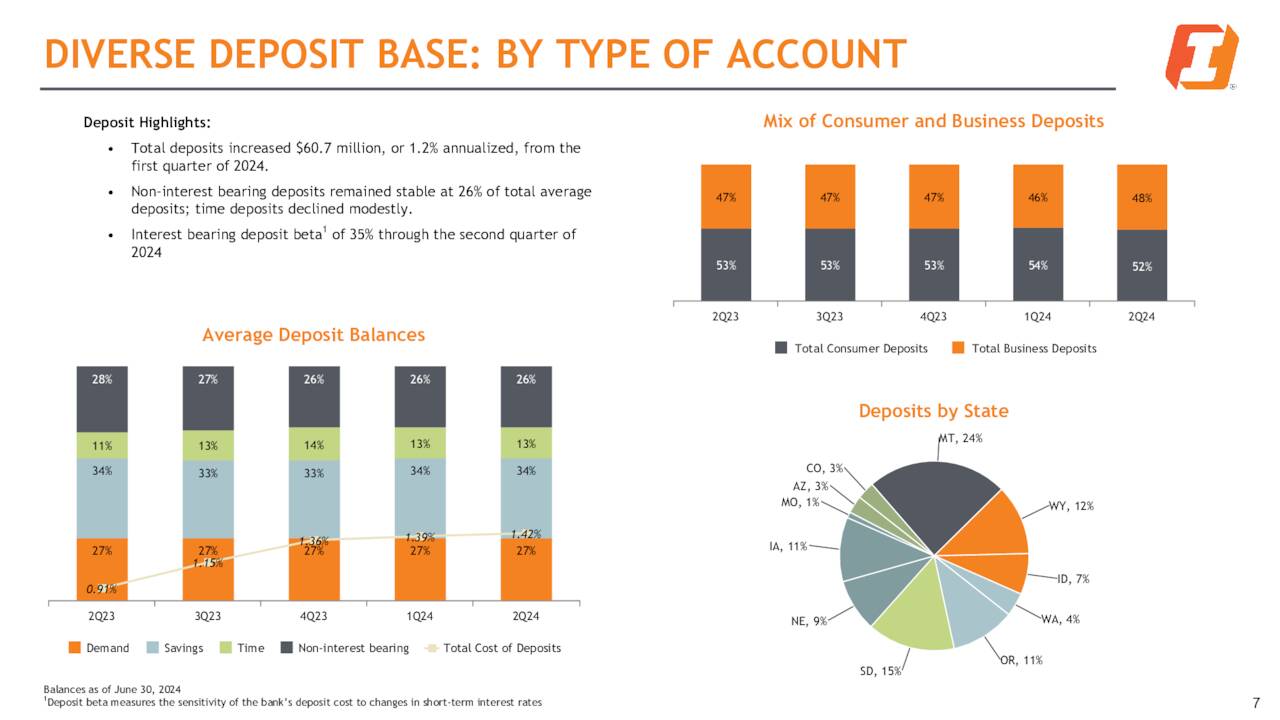

Deposits increased slight ($60.7 million) during the quarter and net interest margins increase seven basis points sequentially to three percent. Net revenues from non-interest income rose 1.2% from the first quarter to $42.6 million. Net interest income rose $1.6 million from the prior quarter to $201.7 million.

Loan Portfolio:

July 2024 Company Presentation

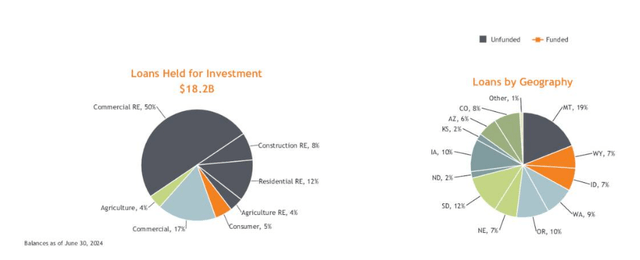

Just under 20% of its loan book in the state of Montana. It also serves major metro areas such as Phoenix, Seattle, Denver, Kansas City and Minneapolis. Now, some 58% of the loans FIBK has kept on its books or $10.6 billion is around commercial real estate or CRE.

July 2024 Company Presentation

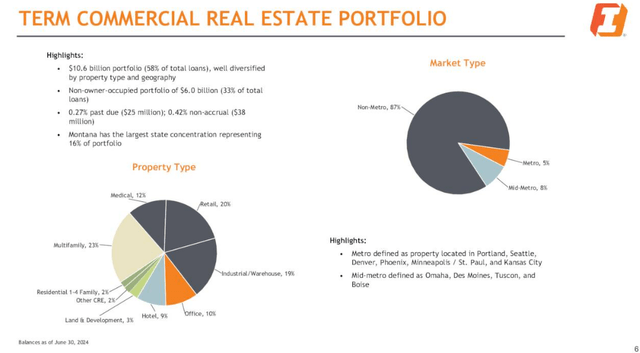

Given the increasing delinquency rates is some categories of CRE, especially office collateralized loans where office values are plummeting, that is a concern. However, only 10% of the loan book in CRE is against office properties, another 20% is in Retail which has significant but lesser challenges at the moment. Now it should be noted that approximately 30% of CRE debt is held by regional banks, which also generate around 70% of overall CRE loans. I would be more worried about a regional bank like Bank OZK (OZK) which I posted an in-depth article around in late May. It appears to have significantly more exposure than First Interstate BancSystem to the riskier areas of CRE such as construction lending going to build the massive number of new skyscrapers going up in Miami for example.

Commercial Mortgage Backed Securities (CMBS) Delinquency Rates (Trepp)

Now, as an article here on Seeking Alpha in August pointed out, First Interstate BancSystem need to make extensive use of the BTFP (Bank Term Funding Program) credit facility due to the unrealized losses on its bond portfolio. This relatively high cost of funding was made available by the Federal Reserve after the second, third and fourth largest bank failures in U.S. history in the first half of 2023. FIBK still has just over $2.4 billion from that facility that will be paid in the coming quarters.

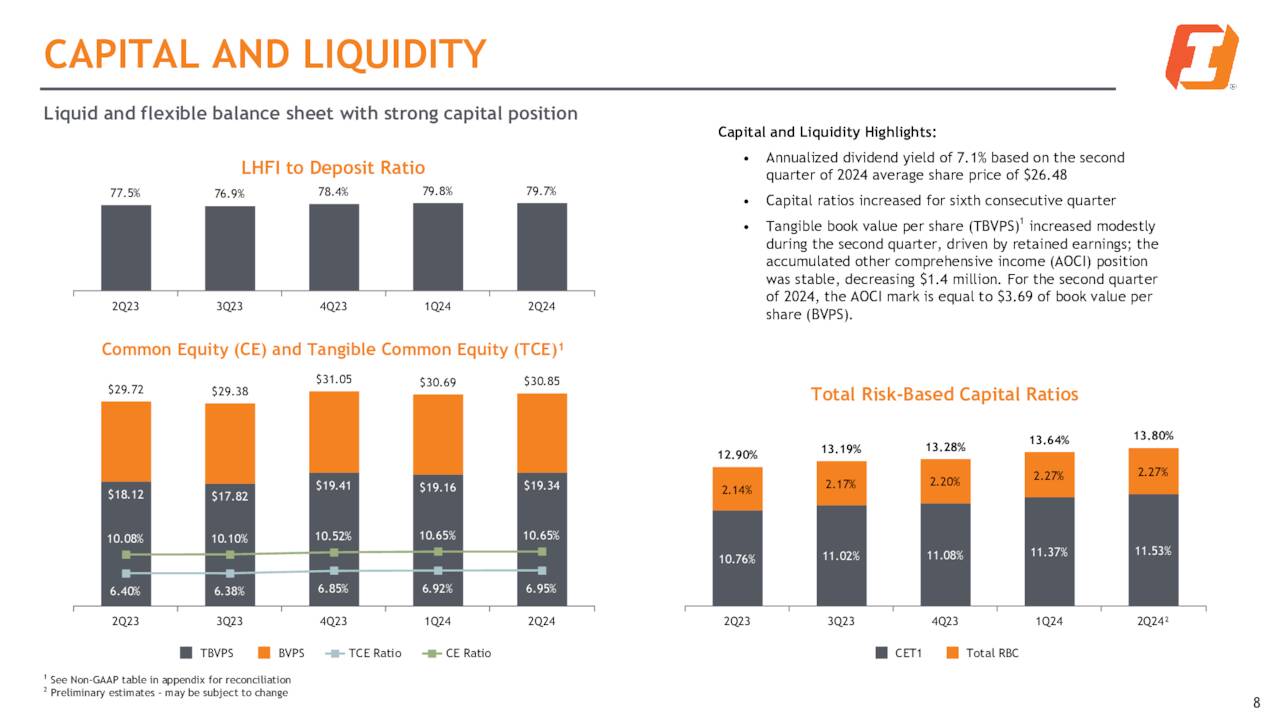

Loan balances increased by $32.2 million in the quarter. Construction loans fell while Commercial and Industrial loans rose by just over $130 million. The CFO was pointed in noting only .65% of the bank’s loan book was on ‘Metro Office‘ properties. Common equity Tier 1 capital increased by 16 basis points to 11.53%. The bank’s capital structure and loan loss reserves look like they are good shape.

July 2024 Company Presentation

July 2024 Company Presentation

Analyst Commentary & Insider Buying:

The current view from the analyst community skews negative. Since second quarter results hit the wires, D.A. Davidson, Barclays ($31 price target, up from $29 previously), Wells Fargo ($30 price target, up from $25 previously) and KBW ($31 price target, up from $29 previously) maintained Hold ratings, but most boosted their price targets. Stephens ($36 price target, up from $32 previously) and Piper Sandler ($37 price target) reissued Buy ratings on FIBK.

The bank’s CEO did add a net $125,000 to his holdings in late July and early August. The last insider purchase in the stock was in June of 2023 by the same individual and the stock did gain some 25% over the next six months. Only two percent of the outstanding float in the stock is currently held short.

Conclusion:

First Interstate BancSystem made $2.48 a share on 989 million of revenue in FY2023. The current analyst firm consensus has profits falling a bit in FY2023 to $2.32 a share on $994 million in sales. In FY2025 they see profits rebounding to $2.53 a share on revenue growth of six percent.

The stock trades at approximately 13 times forward earnings. This is a reasonable valuation considering the shares also have a 6.2% annual dividend yield. It should be noted that based on this year’s projected EPS, FIBK’s dividend payout ratio is over 80%. Meaning, there is unlikely to be meaningful growth in quarterly dividend payouts in the coming years.

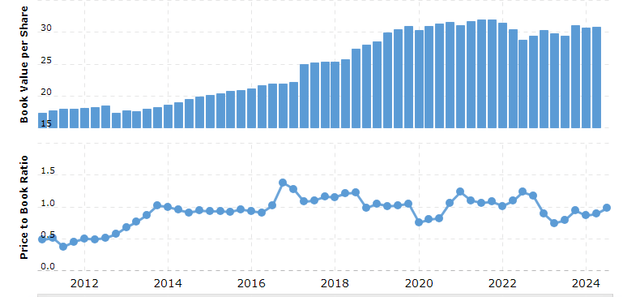

Outside the dividend yield, the stock’s valuation is not compelling given that EPS in FY2025 is projected to be not that much above FY2023 and profits should fall slightly this fiscal year. I also continue to believe the worst is yet to come for the commercial real estate sector as far as delinquency and default rates rising well into 2025. This continuing trend will remain a headwind to regional banks. Finally, the company’s book value per share (A good way to value banks) has been very stagnant for years as can be seen below.

MacroTrends

Therefore, I am passing on any investment recommendation around First Interstate BancSystem at this time. Now if the shares moved back down to the $23 to $25 range during a continued sell-off in the overall market, and there was no notable deterioration in the bank’s loan book, I would pick up some shares at those levels.

Read the full article here

")

")

")