Q4 2024 Earnings Call Transcript")

")

Almost five months ago, I wrote that patient Arcadium Lithium plc (NYSE:ALTM) investors would be rewarded in the long term. Since then, ALTM stock has cratered more than 45%, testing the patience of Arcadium bulls, including mine. There was some positive news last week as China’s CATL, the world’s largest lithium producer, revealed a plan to slash production, potentially leading to an increase in lithium prices. Arcadium Lithium jumped 10% on the news. Although I welcome this positive development, it is difficult to ignore that many of the growth challenges I discussed in my previous article are still prevalent. Some of these challenges include the slowdown in EV sales and the supply growth. After revisiting the prospects for Arcadium Lithium, I continue to believe the company is a best-in-class bet in the lithium market, but only for investors who are willing to stay for the long haul.

No Reason To Be Too Excited About A Reversal In Lithium Prices

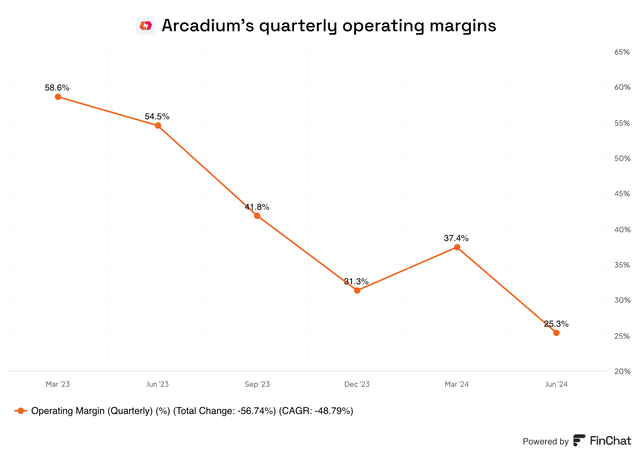

Arcadium’s lackluster market performance this year (down 64%) stems from macroeconomic headwinds faced by the lithium industry. As I discussed in-depth in my previous article, most of the factors that contributed to record-high lithium prices in 2022 have reversed, exerting pressure on the profit margins of lithium producers. Arcadium has not been an exception.

Exhibit 1: Arcadium operating margins

FinChat

Last week’s production cuts announced by CATL are likely to have a positive impact on short-term lithium prices. Although this is good news, a closer look at inventory levels, demand trends, and supply chain dynamics suggests lithium prices are unlikely to sustain these gains in the next 6-12 months.

Let’s look at inventory levels first.

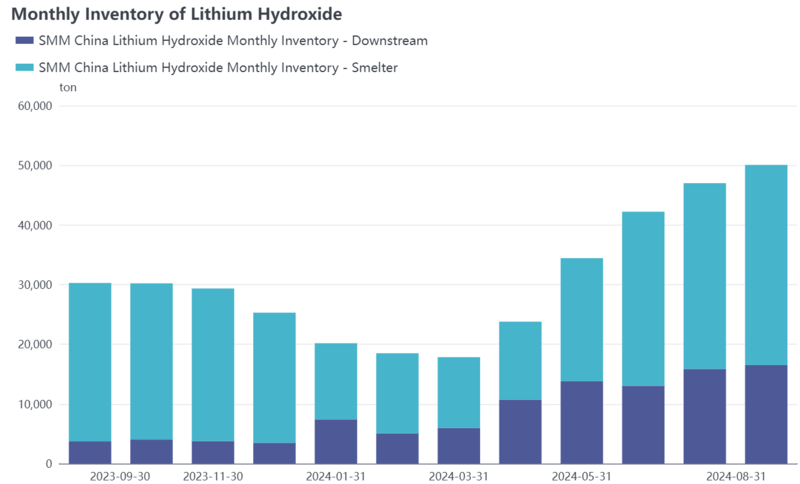

Recently, lithium hydroxide inventory levels have risen, including a 7% MoM increase in August. These increasing inventory levels are a clear indication that demand for lithium products is still falling behind supply – not good news for lithium prices. From a lithium producer’s perspective, the accumulation of stockpiles is a warning sign of potentially lower demand for lithium products in the current period. End users often postpone signing new contracts to benefit from the expectations for lower prices in the foreseeable future.

Exhibit 2: Monthly inventory levels of lithium hydroxide

SMM

The accumulation of lithium hydroxide stockpiles is a clear sign of the demand slowdown in the EV sector. Closely monitoring these inventory levels may help investors identify potential inflection points in lithium prices.

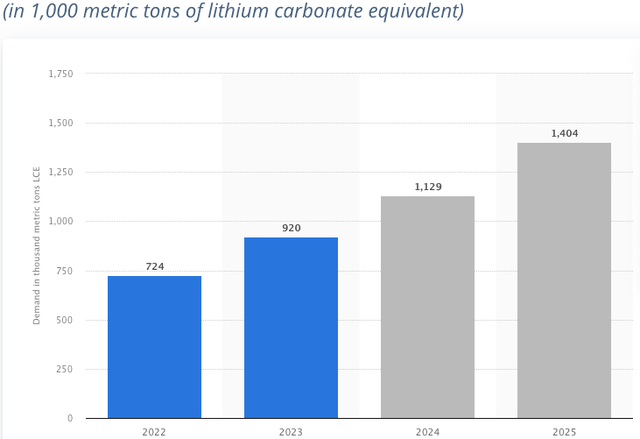

Let’s look at the demand and supply trends now. Analyzing recent demand and supply trends simultaneously should help us understand where lithium prices are headed. According to Statista, lithium demand will grow just over 22% in 2024 to 1.129 million metric tons of lithium carbonate equivalent. This momentum is expected to continue next year, with the demand for lithium exceeding 1.4 million metric tons.

Exhibit 3: Demand for lithium

Statista

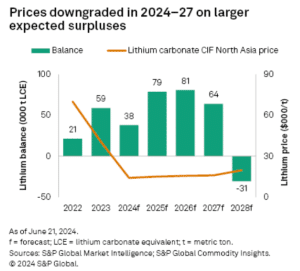

The ongoing automotive industry transformation to embrace EVs is at the center of these lithium demand growth projections. Although demand growth is expected to be stellar, so is supply growth. According to S&P Global, the surplus of lithium is expected to hit 38,000 tons this year. Even more concerning, demand is not expected to outstrip supply until 2028.

Exhibit 4: Lithium market surplus

Carbon Credits

This oversupply, as you can imagine, is not resulting from a major slowdown in demand but from the substantial new supply that is coming online.

- China is expected to add 39 new refinery assets in the upcoming years. According to recent estimates, China will add 874 kilotons of LCE by 2025 alone.

- Arcadium is expected to increase lithium hydroxide production volumes by 40% this year to a production range of 50,000-54,000 tons of LCE.

- The Finniss lithium project in Australia is expected to add 11,000 tons of LCE in 2024.

- Other notable projects expected to come online in the upcoming months include the Cauchari-Olaroz Project in Argentina, the Thacker Pass Project in Nevada, the Rhyolite Ridge Project in Nevada, and the Greenbushes production expansion in Australia.

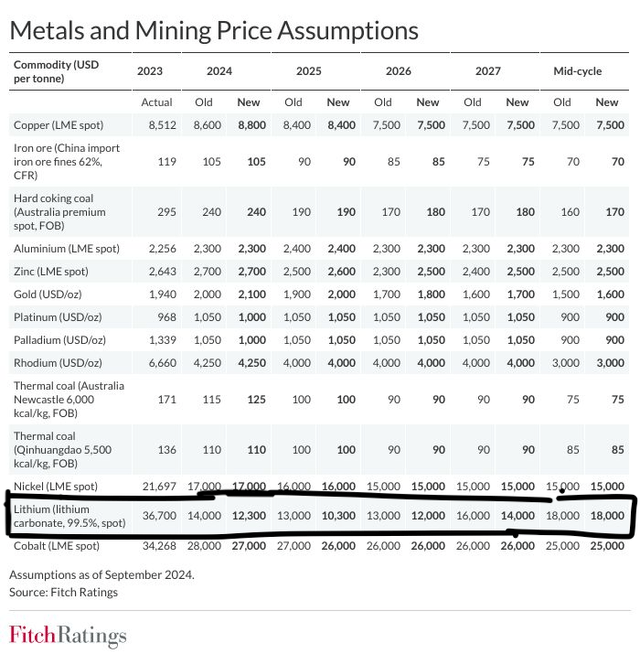

Taking this expected oversupply into account, Fitch Ratings recently slashed long-term price targets for lithium.

Exhibit 5: Fitch Ratings’ price targets for metals and mining

Fitch Ratings

Recent commentary by Citi analysts captures what is happening in the lithium market to perfection. Here’s an excerpt from the Market Talks segment published by the Wall Street Journal on September 12.

Expect a near-term rally in lithium prices as investors cover their shorts, say Citi analysts, raising their 0-3 month price target for carbonate to $14,000/metric ton and for hydroxide to $14,200/ton. The analysts had a prior forecast of $10,000/ton for each of those products. “Taking a 6-12-month view, we do not expect the rally to have ‘follow through’ as higher prices could very well trigger a supply response, potentially leading to loosening of lithium balances,” they say. The analysts pare their carbonate forecast on that time horizon to $13,000/ton, from $14,000/ton before. Their hydroxide forecast goes to $13,200/ton versus $13,000/ton previously.

If lithium producers delay supply expansion projects, there is potential for a short-term rally in lithium prices. However, as noted earlier, I am skeptical of the sustainability of such a rally.

Arcadium Lithium Is Positioning Itself For The Future

As I discussed in my previous article, I believe lithium demand will eventually exceed supply in the coming years. Thereafter, demand is likely to persistently remain above supply, resulting in elevated lithium prices. Arcadium, as a low-cost producer, will be a big winner in a sustainable recovery in lithium prices. The growth in the affordable EV options available to the consumer will be a key driver of lithium demand.

I believe Arcadium is strategically aligning its business to benefit from the expected recovery in lithium prices. It is investing in expanding its production capacity while making the necessary spending adjustments to push back some capital spending plans to coincide with the expected recovery of the lithium market. I appreciate the company’s continued interest in expanding its production capacity despite rising lithium hydroxide stockpiles. This positions the company to benefit from a dramatic increase in lithium prices resulting from an unforeseen lithium shortage which may stem from underinvestment in mining projects by its peers.

Some strategic decisions taken by the company to follow a cautious yet optimistic path toward expanding production include pausing the Galaxy project in Canada while continuing to invest in the Nemaska project. The company’s decision to revise the completion timelines for the Fenix project and the Sal de Vida project to ensure sequential completion to avoid a supply overload is also commendable.

ALTM Stock Valuation Is Attractive

Arcadium is currently valued at a forward P/E of 12.5 compared to the materials sector median P/E of 16. After revisiting the company, I updated my cash-flow model to reflect double-digit revenue growth expectations in the next four years but a modest single-digit decline in 2028. Some other notable assumptions include a 3% terminal growth rate and a WACC of 9%. I expect EBITDA margins to improve from around 35% this year to just over 50% by 2028 as well. Based on these assumptions, my intrinsic value estimate for Arcadium Lithium comes to $7.43 per share, which implies an upside potential of 204% from the current market price.

Takeaway

Arcadium Lithium stock may benefit from a short-term rise in lithium prices in the coming months, but I do not expect such a rally to be sustainable in the next 12 months given the unfavorable market developments highlighted in this article. However, in the long term, I expect lithium prices to rebound sharply. Arcadium Lithium, which is attractively valued today, is well-positioned to benefit from this expected reversal in lithium prices. I am comfortable with a less than 5% exposure to ALTM in my portfolio as I believe the risk-reward profile is strongly in favor of long-term investors despite the lack of a catalyst to drive shares higher.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q4 2024 Earnings Call Transcript")

")

")

")

")