")

Q4 2024 Earnings Call Transcript")

")

Introduction

The last time I wrote about Games Workshop (OTCPK:GMWKF) was less than a year ago; in that article I described the company’s business model and tried to explain in broad strokes the “magic” behind the Warhammer brand. A year later, nothing fundamental has changed in GW’s business, but I thought it might be useful to write one more article about this remarkable company to talk about what has happened in the last year and to elaborate on some aspects that I had to leave out last time.

If this is the first time you are hearing about Games Workshop I suggest you catch up on the previous article and then continue the in-depth discussion with this one, since I will be taking some things for granted (e.g. what is Warhammer) to avoid unnecessary repetition.

Business

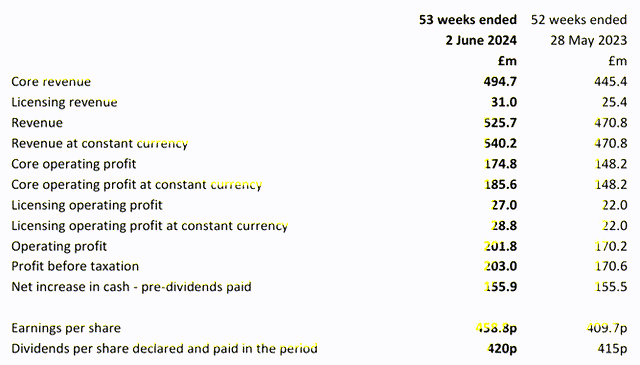

Annual Report FY24 (Games Workshop Group)

Over the past year, GW’s revenue increased by a very good +11.7%, above analysts’ expectations, to £525.7 million (slightly below what I had assumed in my best case scenario). On earnings, GW also managed to surprise analysts by achieving a PBT of £203 million, up 19% yoy. These results stem from a good performance of the Core segment and excellent results above expectations in Licensing Revenue (£31 million revenue, £27 million operating profit).

Annual Report FY24 (Games Workshop Group)

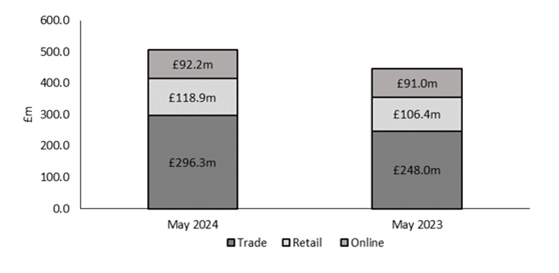

Core Revenue increased by 11.1% (+13.9% on a constant currency basis) to £494.7 million, mainly due to growth in the Trade channel (third-party stores not operated by GW). Revenues from this channel in fact grew by 16.3%, boosted by an addition of about 700 stores bringing the total number to 7.200. Direct sales from the site remained virtually flat compared to 2023, while the Retail segment grew by 8.6%.

-Retail:

Compared to the others I think the Retail sales channel deserves a more in-depth analysis. When we talk about “Retail” we are referring to Warhammer flagship stores run by Games Workshop. Most of these stores are run by one person and have the primary purpose of attracting new fans. Within these stores you will find mainly “starter sets,” which are suitable for getting beginners up to speed; they are also a great way to meet other enthusiasts with whom you can play games, participate in tournaments, or even simply paint your own miniatures together. Keep in mind that the customers who tend to spend the most are new players; in fact, the expense of building a new “army” can easily reach $1000 up to $2000. These stores are therefore critical to attracting new fans and building a community. Management is very careful about capital allocation and over time has opened new stores where they saw fit and closed those that did not meet their performance requirements.

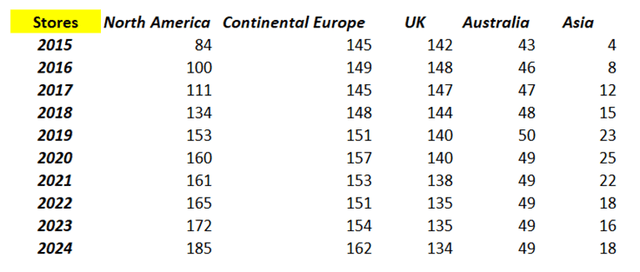

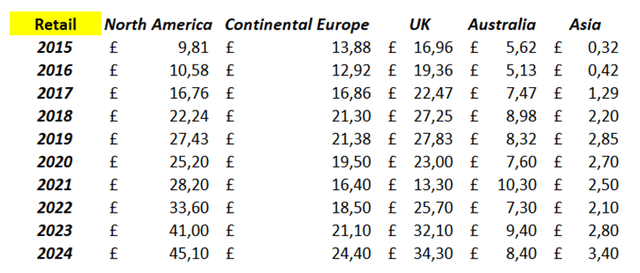

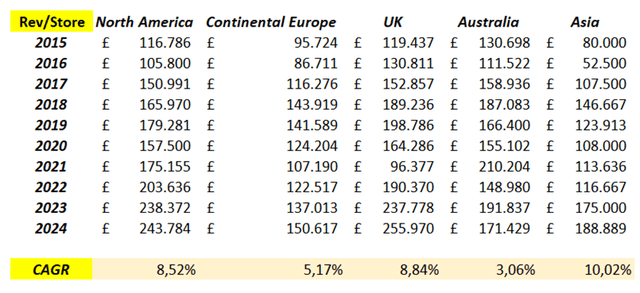

In the following tables I have summarized the trends in the number of stores, Retail segment sales, and average sales per store from 2015 to the present for each geographic area.

Notes to the financial statements -Segment Information (Games Workshop Group) Notes to the financial statements -Segment Information (Games Workshop Group) Notes to the financial statements -Segment Information (Games Workshop Group)

Looking at this data, we can get an idea of management’s ability to allocate capital and manage these stores. Starting with the UK as an example, we can see how in the face of a decrease in stores (from 142 in 2015 to 134 in 2024), revenues have more than doubled, bringing the average revenue per store from £119,000 in 2015 to £256,000 in 2024.

The best performing geographic area is clearly North America, since 2015 we have seen strong store expansion and a CAGR of sales per store of about 8.5%, resulting in Retail revenues that have more than quadrupled in nine years. In the latest annual report, management pointed out that they may decide to slow down on opening new stores in North America to give the team time to focus on the performance of existing ones, while always keeping open the possibility of reaching 200 stores soon.

Australia and New Zeland is the geographical area that is experiencing the most difficulties, due to organizational problems that they are trying to solve. In contrast, Asia, with Japan and China, are performing very well with Retail sales up 21.4 percent yoy. This geographical area still accounts for a very small part of GW’s sales, but it is also the market with the most potential for growth and development.

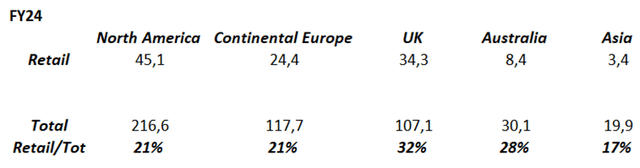

In the following image you can observe the weight of this sales channel in total sales for each geographical area.

Notes to the financial statements -Segment Information (Games Workshop Group’s Annual Report FY24)

-Trade:

As mentioned earlier, Games Workshop can currently count on about 7200 multi-brand stores to be able to distribute its products. The variety of products that can be found in these stores is much wider than in the Retail channel, while in the latter we mainly find products for new fans, in the former it is also possible to buy more “advanced” products. In 2024 almost 60 percent of Core Revenue was realized through this sales channel, with 700 more stores than in 2023 and revenues increasing by about 19.5 percent yoy.

It should be kept in mind that this calculation also includes sales made online by authorized distributors (only sales derived from Warhammer.com fall into the “Online” channel). That said, it is clear that increasing authorized outlets is a quick and effective way to reach fans and increase potential customers. It is not uncommon for even some of these stores to hold Warhammer tournaments to bring players together, and this is a great way to keep the community and passion for the game alive.

-Licensing Business:

the Warhammer IP is content-rich and virtually inexhaustible; the game’s lore has been expanded every year for nearly 40 years, and content and story creation is at the core of Games Workshop’s strategy. The Warhammer Studio team has succeeded over time in creating incredible worlds and stories that have millions of people hooked, and each year they continue to expand the horizons of what is already a vast universe. Although GW’s core business is selling miniatures, not leveraging this wealth of content to make video games, series, or movies is a waste, both for fans and shareholders.

As outlined in the annual report, the Warhammer Studio is the heart of Games Workshop, which, in addition to directly producing content such as the Black Library books, animations, and other content, is responsible for managing and approving IP with licensing partners.

The agreement between Games Workshop and Amazon to produce series, movies, and merchandise on the Warhammer 40k universe has been known for some time now, there is also an option for Amazon to obtain the rights to the Warhammer Fantasy universe following the release of content on Warhammer 40k. Currently we have no other news about this agreement, the only thing we know is that the two companies have until December 2024 to agree on creative guidelines, the agreement can only continue if this phase is successful. Needless to say, how much of a positive catalyst this agreement could be for Games Workshop, not only would it bring in significant revenues from fees (in the last year the operating margin of this segment was 87%), but it would also make the Warhammer brand even better known and could bring a lot of people into the hobby and keep the enthusiasm of fans alive. We will just have to wait a few months and see how the situation evolves.

It is very recent news of the extreme success achieved by the game “Warhammer 40k: Space Marine 2”, developed by Saber Interactive and officially released last September 9. Even before the official launch date, the game climbed the Steam charts, thanks to the possibility of having early access by purchasing a “premium” version of the game. Within 24 hours of launch, the game had a record high of 225,690 simultaneous players on Steam, shattering the achievements of any other Warhammer game and exceeding all expectations. Publisher Focus Entertainment reported on X on Sept. 10 that it had reached a record 2 million players. This is the seventh week it has been among the top 100 best-selling games on Steam and it is currently still in first place.

Focus Entertainment

If we consider that the base price is $60 (the Gold Edition and the Ultra Edition that entitled early access cost $90 and $100, respectively), and taking away a 30% retained by the distribution platforms, we obtain a minimum revenue per copy sold of $45, multiplying it by 2 million we arrive at a revenue of at least $90 million in a few days. As mentioned, the game has been an unexpected success, has been very popular with gamers, and would seem to have all the credentials to continue to be relevant for a long time, thanks to the presence of the online multiplayer mode.

This in addition to being great news for GW’s upcoming results, where revenues from the licensing business could easily exceed analysts’ expectations, is also an excellent catalyst for growth in the coming years. Indeed, it has been 11 years since the release of the previous chapter of the game “Warhammer 40,000: Space Marine”, which was not a huge success at launch but managed to perform well over time selling 2.8 million copies. Taking note of these outstanding results, however, it seems almost a foregone conclusion that a third chapter of the story will be published in the future, and we probably should not have to wait another 11 years. As in the case of the Amazon series, these products serve not only to earn fees for Games Workshop in the short term but more importantly to bring millions of people closer to the world of Warhammer.

Two other games were announced during the period, the sequel to the PC and console strategy game Mechanicus 2 and Talisman 5th Edition. As successful as the first Mechanicus was for the type of game, the numbers we can expect will not compare with those achieved by Space Marine 2.

To summarize, revenues from the Licensing segment are divided as follows: 70% console and PC games, 15% mobile, 15% other. In the period under analysis revenues from the Licensing Business were particularly high due to a high level of guarantee income on multi-year contracts concluded in the second half of the year (£17.6 million). Cash received from licensees amounted to £25 million (£26.5 million in FY23). Finally, the total licensing receivables balance was £28.3 million.

-Warhammer+:

Introduced three years ago, Warhammer+ is Games Workshop’s subscription service to further engage fans of the game. Within the platform you can find original animated shows, tutorials (such as how to paint your own miniatures) and much more. Of note is the possibility for subscribers to get some benefits in the new game Space Marine 2 or to have the opportunity to buy exclusive miniatures.

The subscription price is £5.99 per month or £49.99 per year, and according to the latest reported results there are about 176,000 subscribers (136,000 in FY23). If we assume that everyone bought the annual package, Warhammer+ sales in 2024 may have been around £8.8 million. It is certainly still a very marginal part of the business but it is also a great way to fund the Warhammer Studio business. As it takes time and the benefits offered increase, this service could become increasingly relevant, although I don’t think it will be able to move the needle too much.

Future Prospects

In this section I would like to talk about the future development prospects of Games Workshop, starting with the most concrete and likely scenarios, and then concluding with some of my own speculations and ideas about the long-term future of the company.

-Prime Video:

As discussed earlier, the most relevant catalyst at the moment is the potential agreement with Amazon to produce series and films about the Warhammer 40k universe. While in the previous chapter I described the obvious positive effects that the conclusion of this agreement could have, in this one I want to focus on the other side of the coin and highlight what are currently the most relevant worries and possible negative effects of a cancellation of the series.

In December 2022 it was announced that Henry Cavill would serve as actor and producer on the Amazon adaptation of Warhammer 40k. It has now been almost two years since the announcement and there have been no major updates. In December 2023 Games Workshop and Amazon were given 12 months to agree on creative guidelines, as we are now a few months away from the deadline and there have still been no updates, rumors have begun to proliferate about a possible cancellation of the series. These reports do not come from official sources and tend to be false or unfounded, stemming mainly from the absence of new official announcements and the approaching deadline. The two companies must also agree on the type of media to be used; they must actually choose whether it is more appropriate to start with a series, a movie, or both. The successful outcome of this negotiation would bring many benefits to both parties, and I think they want to use all the time they have to clarify the most relevant points and make sure that the eventual Amazon adaptation is faithful to the original material. The only thing we can do to draw conclusions is to wait for an official statement.

That being said, what would be the impact on Games Workshop’s business of any negative outcome of the deal? A major growth opportunity would undoubtedly be wasted, but GW’s core business would still remain in excellent health. In fact, we are not talking about a huge marketing ploy necessary to revive a dying brand, as in the case of Mattel with Barbie. The Warhammer brand is in full health and expanding, even without movies or series to sustain growth. Undoubtedly Warhammer fans would be disappointed not to see on the screen the first live action adaptation of the stories and battles that for the moment, they have only read about in books or experienced on the gaming table, but they certainly would not give up their passion that in many cases has involved them for decades.

Monish Pabrai’s words, from the book “The Dhandho Investor: The Low-Risk Value Method to High Returns”, are excellent to describe this situation: “Heads I win; Tails I don’t lose much.” Without an Amazon series or movie, a huge opportunity for revenue growth and profits would be lost, but this would not actually change anything for the millions of gamers and fans who are currently captivated by the wonderful world of Warhammer.

-Video games:

I have already spent several lines in discussing the unexpected success achieved by Space Marine 2, both in terms of numbers and in terms of fan ratings and appreciation. Although it is still too early to draw conclusions, it would seem to be a game that would stand the test of time, thanks to the engaging competitive multiplayer mode that could possibly provide longevity to the game.

The success of Space Marine 2, in addition to bringing excellent results in the Licensing Business to GW in the near future, may motivate the developers to develop additional chapters of the story (there is no shortage of creative material to work with) and to release them in a shorter time frame than last time. Space Marine 2 was released 11 years after the first chapter, given the results, I would not be surprised if a third and fourth chapter of the game were released in the same time frame in the future. As an additional side effect of releasing more video games, we could see an increase in Warhammer+ subscribers, as this would offer exclusive benefits within the various games.

-Geographical expansion:

In this section I want to reexamine Games Workshop’s Core Business and reflect on potential future developments in different geographic areas.

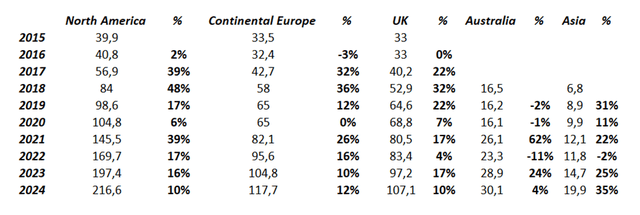

Notes to the financial statements -Segment Information (Games Workshop Group)

In the image you can see the historical trend (from 2015 to the present) of GW’s Core Revenue in different geographic areas. The company’s strategy is to continue geographic expansion in both the Retail and Trade channels. Management is very cautious and careful about capital allocation for new direct store openings, so there is no fixed target of new stores per year but it all depends on market conditions and opportunities glimpsed by management.

In the coming years I expect expansion especially in North America and Asia. While North America is already a mature market, but with further potential for growth, Asia (particularly China and Japan) is a geographic area yet to be really penetrated, with equally great potential for growth. In December 2022, the first Warhammer cafe store was opened in Tokyo, achieving considerable success by enlisting many new fans.

Australia and New Zeland is the geographic area where they are experiencing major organizational problems. In the latest annual report, CEO Kevin Rountree commented:

It’s going to be busy in Australia in the next few years as we upgrade their core financial systems and relocate the whole team to a new warehouse and office HQ too. Any IT solutions rolled out here will be the globally chosen solution. These projects will be a fair challenge; centrally run with the full support of the UK based team with an appropriately resourced local implementation team. My fingers are crossed – we will deploy more resources, if needed, to ensure they’re not crossed for too long.

-Ideas for the Far Future:

In this short paragraph I would like to try to describe some of my ideas about what the long-term future of Games Workshop’s business might be (by long-term I mean 10-15 years). I should point out that these are my personal assumptions not supported by objective data, so they have not been taken into account at the evaluation stage and are not relevant to my final judgment of the quality of the company.

That being said, I think that in the future the company may create a new business segment focused on content production (movies or animated series). As of today Warhammer Studio makes animated series available on Warhammer+, this business segment however is not very relevant at the moment. As management is very cautious in capital allocation, so far it has not made sense to invest large amounts of capital in the creation of more structured content. In the event that the deal with Amazon goes through and a Warhammer Cinematic Universe can then be created, management could observe and evaluate the audience response to this kind of content. Should there be a lot of interest (as is expected), they could begin to consider investing in content produced directly by Warhammer Studio, to be distributed not only on Warhammer+ but also in theaters or on other streaming platforms.

Making a series or movie about the Warhammer universe at the moment is like a leap of faith; it is expected to appeal to many people (and it probably will), but it is still the first time that this kind of product has been attempted and so there are no objective benchmarks to rely on. A collaboration between Amazon and Games Workshop could provide an opportunity to set precedents that can be used by Warhammer Studios, so that they can invest large sums in more elaborate content with more confidence.

From the amount of “ifs” I used in the previous lines, you can understand the impossibility of using these assumptions for reasonable evaluation and the necessity of the premise made at the beginning.

Valuation Update

As mentioned in the introduction, Games Workshop’s fundamentals have not changed in a year, this implies that even the valuation is not radically different to the previous one. The difficulties in estimating future results also remain; as much as I am fairly convinced that GW will have a bright future, it remains difficult to chart a definite trajectory.

In the previous article I used a discount rate of 12%, definitely high, but justified by the high uncertainty in estimating future results. Although the difficulty in estimating GW’s future has not reduced, after continuing to study the company for a year, I feel much more confident in the more optimistic assumptions I had made than the pessimistic ones. For this reason, I decided to use a lower discount rate in the new valuation.

Given the absence of leverage, we can approximate the WACC with the cost of equity. Using the UK 10-year bond yield as risk-free rate, considering an equity risk premium of 5.48% (I used the one estimated by Professor Damodaran) and a 3-year Beta of 1.13, we get a WACC slightly below 10%. In my evaluations I prefer never to use a discount rate below 10%, even if the WACC were to be lower. This is the minimum return I expect to get by investing in a single stock. I consider it pointless to use lower discount rates, even if they were to be justified by the formulas, if my goal was in fact to get 7-8% per year I would rather invest in a well-diversified index than take the risk of stock picking. Having closed this brief parenthesis, in this case the WACC and my minimum required return match.

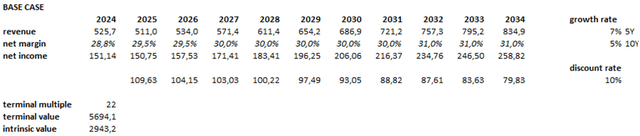

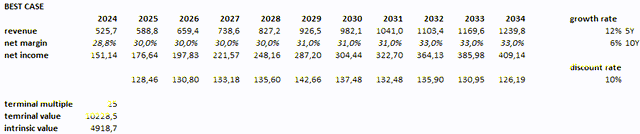

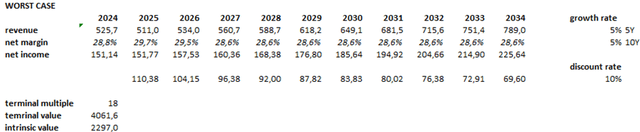

As you can see from the images below, besides updating the 2024 values with the company’s achievements, the rest has remained the same as a year ago, growth rates, margins, and projected multiples. This is because compared to a year ago besides the unexpected success of Space Marine 2, we have no new relevant information available to be able to more accurately estimate the future of Games Workshop. Probably only after we would have news of the outcome of the deal with Amazon could we make new assumptions, but for that we have to wait until December. As a result, the only thing that has changed in the DCF is the discount rate which has gone from 12% to 10% with the resulting increase in valuation.

Author’s estimate Author’s estimate Author’s estimate

In the base case scenario I do not consider the major impact that the development of a Warhammer Cinematic Universe might have. I assumed continued revenue growth in all geographic areas (higher growth rates in North America and Asia than in other areas), as well as a slight improvement in margins due to economies of scale and an increase in licensing revenue (video games only). In the best case scenario, on the other hand, I considered higher growth rates in the event of a successful outcome of the Amazon deal. To conclude, the worst case scenario considers the assumption that the Licensing Business does not develop particularly and consequently moderate revenue growth due to a slight increase in miniatures sales volumes and price increases in line with inflation.

On the other hand, with regard to the more “personal” and less numerically demonstrable part of the valuation, a year later I believe that the worst case scenario is much more unlikely to occur. With the developments that have taken place and the potential for future growth described in the previous paragraphs, I think it is unlikely that GW will be able to grow its revenues by only 5% per year. I also believe that the Licensing Business can have a strong development in the future, potentially growing the company’s margins further.If we therefore consider the base and best-case scenarios as more “reasonable,” I feel I can say that the company is currently correctly valued, according to the information currently available. In the case of a future realization of a Warhammer Cinematic Universe, current prices might even offer a margin of safety.

Conclusion

I hope I have succeeded in enriching the description of Games Workshop and the Warhammer universe, which I began with the previous article made almost a year ago. Games Workshop is an exceptional company with a unique brand that is extremely difficult to replicate and is run by an excellent management team, very competent in capital allocation and aligned with the interests of shareholders and fans of the game.

I do not currently own shares in Games Workshop, but I am seriously considering making an initial investment. What currently holds me back the most from investing a significant portion of my portfolio in GW are the same doubts that held me back a year ago, which are the high difficulty of estimating future results and the price. More precisely, the combination of these two factors. I tend to be willing to accept a high degree of uncertainty, but the price I pay must be low enough to give me a large margin of safety to bear the risk I am exposing myself to.

Although I believe the company is currently correctly valued, I do not believe the current price offers an adequate margin of safety for my investment criteria. Why then did I write that I plan to invest in it? As mentioned, I believe the current price is not too high, and being a business of extraordinary quality, perhaps it is wise to add it to the portfolio, waiting for the bargains that the market offers from time to time to increase at lower prices.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q4 2024 Earnings Call Transcript")

")

")

")