")

When I last wrote about MercadoLibre (NASDAQ:MELI) on April 11, 2024, I recommended it as a strong buy. That analysis has worked out so far. The stock is up 32.22% compared to the S&P 500’s (SPX) 6.57% rise. My previous article discussed how investors were disappointed in the company’s fourth quarter 2023 earnings report, as it displayed shrinking margins and missed analysts’ GAAP earnings-per-share (“EPS”) estimates.

Since then, the market has been far more pleased with the company’s earnings reports. The company’s first-quarter earnings report beat analysts’ revenue and earnings estimates by a vast amount. On August 1, it reported an equally solid second-quarter 2024 earnings report. It beat analysts’ revenue estimates by 8% and earnings estimates by 26%. The stock rose 11% the day after reporting its second-quarter results.

The company has become a leader in Latin American e-commerce and digital payments. Although a regional player, the company has built one of the most popular websites globally. Its website states that it is “one of the top 10 most visited e-commerce websites in the world.” Although e-commerce and digital payments are businesses that are easy to start and create competition against existing players, MercadoLibre has maintained its dominance in the region against numerous multinational and regional competitors by being among the first to start an e-commerce operation in Latin America (MercadoLibre started in 1999) and a digital payments platform (Mercado Pago began in 2003). Its first-mover status allowed it to build a growing marketplace of buyers and sellers, a double-sided network effect moat, well before encountering significant competition. According to the company, the e-commerce platform currently has 65 million buyers and 12 million sellers. The more consumers that shop on the platform attract more sellers. The more sellers that offer their wares on the platform create more product choices, attracting more consumers. Once MercadoLibre reached critical mass, it became difficult for any competitor, including Amazon (AMZN), Alibaba (BABA), and Walmart (WMT), to displace it.

This article will discuss the company’s competitive advantage with its logistics operation, Mercado Envios, and briefly review its second-quarter earnings report. It will also discuss one significant risk that investors need to be aware of before investing in the company, examine the valuation, and explain why I downgraded the stock from strong buy to buy.

Mercado Envios is a competitive advantage

MercadoLibre established Mercado Envios in 2013, taking a page from Amazon’s playbook. Amazon became dominant in the U.S. market because it built the best package delivery platform, which became crucial in delivering the products consumers wanted faster and more reasonably priced than other providers. A logistics game plan in Latin American markets may be even more critical for e-commerce than the U.S. market.

Historically, Latin America has had poor logistics due to inadequate infrastructure (less-than-ideal roads, railways, ports, and airports), high trade barriers, and highly bureaucratic customs and border procedures. MercadoLibre was the first e-commerce company to establish an extensive logistic network in Brazil and Argentina. It will likely be difficult for any company to replicate what Mercado Envios built over the last decade. For instance, Sea Ltd. (SE), a global e-commerce company based in Singapore, has shown that it could create a capable logistics operation in Southeast Asia. It made a big show of entering Brazil in 2019 and several other Latin American countries in 2021. Some thought it would be able to compete with MercadoLibre. That boldness ended in a whimper. Although Sea still operates in Brazil, it has exited several South American countries. MercadoLibre has multiple advantages over competitors in Latin America. One of them is that it can deliver a wider variety of products faster and more reasonably priced than competitors.

MercadoLibre Investor Relations Officer Richard Cathcart said on the second quarter 2024 earnings call:

Our logistics network plays a major role in enabling e-commerce in the region and driving more offline retail online. It has become a key competitive advantage for MercadoLibre.

Cathcart also discussed how Mercado Envios opened a fulfillment center in Texas in the U.S. in the second quarter of 2024. He highlighted the reasons the company opened up the fulfillment center on the second quarter earnings call (emphasis added):

This is the first fulfillment center outside of Latin America and it was opened to expand the assortment of products we offer to Mexican consumers by plugging U.S. sellers into our ecosystem. This is complementary to our existing cross-border business from China into Mexico. We are offering a great shipping service for our U.S.-based assortment. Buyers are receiving their packages from the USA within a couple of days in the north of Mexico and within approximately three days in Mexico City. Shipping is free, and we also offer interest-free installments.

There are four things to note in the above commentary that help to widen MercadoLibre’s moat:

- MercadoLibre is expanding the variety of products on its Mexican platform.

- It is increasing the number of sellers on its Mexican platform.

- Mercado Envios is providing Mexican consumers with relatively speedy delivery.

- The company is providing free shipping.

Perhaps Walmart and Amazon can remain competitive in Mexico, but this new service makes it extremely difficult for new entrants and some traditional brick-and-mortar companies to compete.

Cathcart also discussed on the earnings call that the company is expanding its use of robots in fulfillment centers. He announced:

In June 2024, we took another major step in our innovation journey with the launch of robotics in our distribution center in Cajamar, just outside the city of Sao Paulo [Brazil]. A total of more than 300 robots will have arrived by the end of the year, with 100 of those already up and running. These robots will collaborate with the human workforce and will handle tasks such as transporting shelves containing products from storage areas. This optimizes processing time by 20%.

What robotics means in practical terms for consumers in the region is that Mercado Envios can deliver products faster. It also means that the company can store more products in a distribution center, making more effective use of space. The company claims it will be able to save “up to 15% per square meter” in space. To learn more about the company’s logistics operations, listen to Richard Cathcart’s interview with the head of Mercado Envios, Agustin Costa, on the company’s website.

Company fundamentals

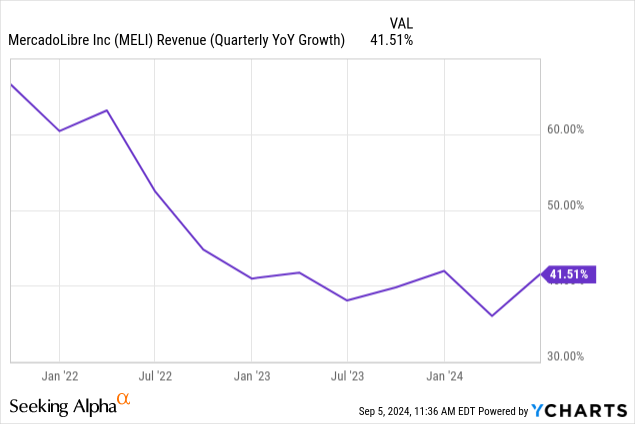

MercadoLibre’s revenue growth year over year rose to 41.51%, up approximately 113% when excluding currency effects (FX-neutral). This revenue growth has been the fastest since the third quarter of 2022.

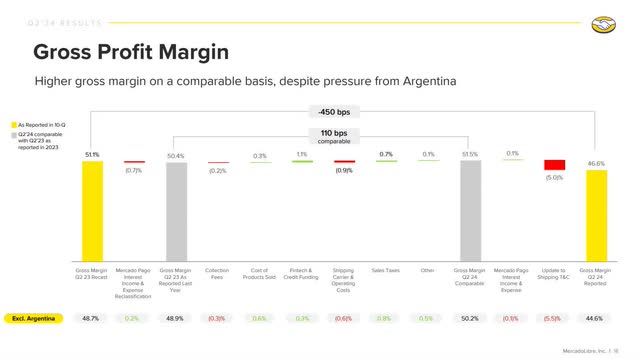

MercadoLibre’s reported second-quarter 2024 gross margin was down 450 basis points (“bps”) to 46.6%. However, most of the company’s reported gross margin decline occurred because of changes in how it accounts for certain shipping transactions. Those changes reduced gross margin by 5% and are listed on the bar chart below as an “Update to shipping Terms & Conditions (T&C).” Its first quarter 2024 investor presentation shows the updated T&C on page 25. The two gray bars are an apples-to-apples comparison of second-quarter results using the T&C from 2023. On a comparable basis, MercadoLibre’s second quarter 2024 gross margin rose 110 bps year-over-year.

Mercado Libre Second Quarter 2024 Investor Presentation

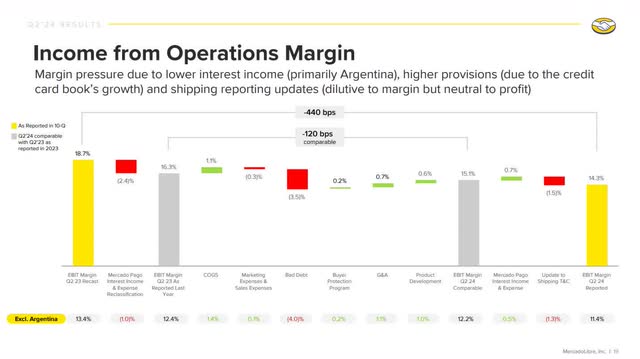

MercadoLibre’s reported operating margin was 14.3%, down 440 bps year over year. Changes to its shipping T&C reduced operating margins by 1.5%. Additionally, the company reclassified Mercado Pago’s interest income and expense, which impacts the operating margin but leaves the profit margin unchanged. MercadoLibre explains these changes on page 24 of its first quarter 2024 investor presentation. The reclassification reduced the operating margin by 2.4%. On a comparable basis, MercadoLibre’s second quarter 2024 operating margin only declined 120 bps year-over-year. This decline resulted from the 350 bps negative impact of bad debt, partially offset by the company’s growing operating expenses slower than revenue growth.

Mercado Libre Second Quarter 2024 Investor Presentation

MercadoLibre’s second quarter 2024 shareholder letter stated (emphasis added):

We also scaled G&A, Product Development, and Sales & Marketing expenses on a reported basis, with 2.8 ppts [percentage points] of operating leverage. This reflects our continued focus on operational efficiency and ability to deliver cost dilution as the business scales.

The bolded statement indicates that the company has operating leverage, meaning it can grow its profits faster than its revenues — attractive to investors.

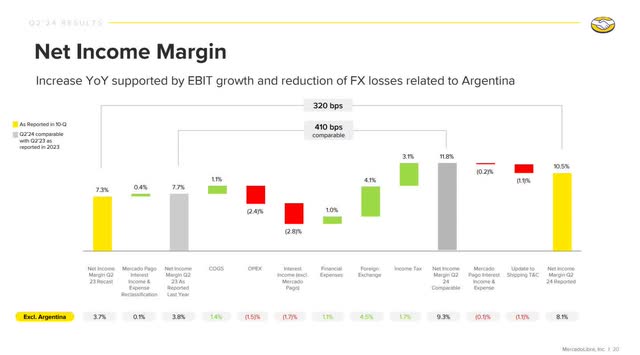

MercadoLibre’s reported net income margin increased by 320 bps to 10.5%. On a comparable basis, MercadoLibre’s second quarter 2024 net income margin rose 410 bps year over year.

Mercado Libre Second Quarter 2024 Investor Presentation

The company generated diluted EPS of $10.48, which is an earnings growth of 103% year over year.

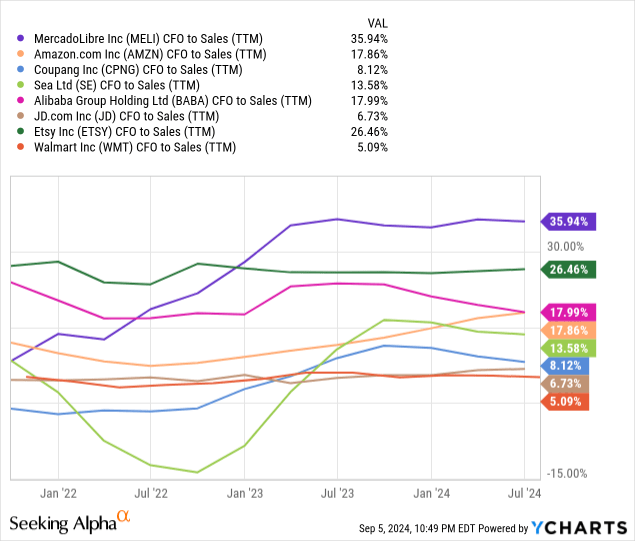

MercadoLibre’s cash flow from operations (“CFO”) to sales is 35.94%, the highest among publicly traded e-commerce companies. Maintaining or increasing this number from the current level would bode well for future free cash flow (“FCF”) generation.

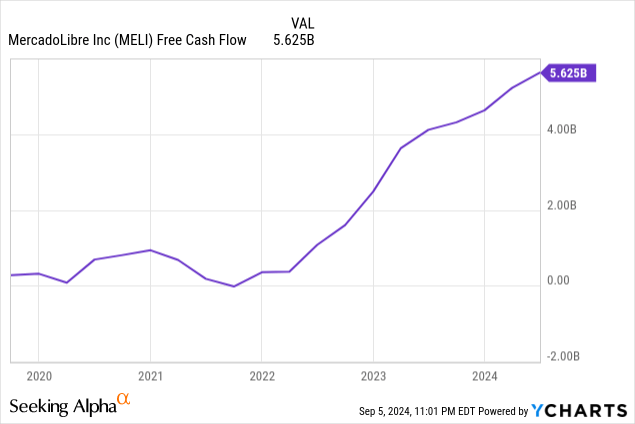

The following chart shows that FCF took off around the end of 2021. In the second quarter of 2024, the trailing 12-month (“TTM”) FCF was $5.625 billion.

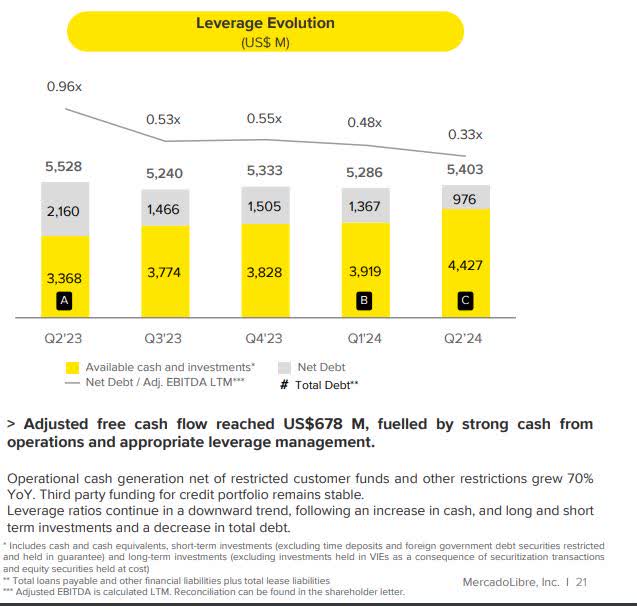

MercadoLibre ended the June 2024 quarter with $4.427 billion in cash and short investments. Total debt was $5.403 billion, and net debt was $976 million.

Mercado Libre Second Quarter 2024 Investor Presentation

Its second-quarter 2024 net debt-to-TTM adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) was 0.33. This metric means the company can quickly repay all its debts with cash and core profits. MercadoLibre is in a solid financial condition.

Risks

Latin America may be one of the most challenging places in the world for a business to operate. For instance, on the ease of doing business index, Brazil ranks 124, and Argentina ranks 126 (only one place ahead of Iran). The highest countries on the list in which it operates are Chile at 59 and Mexico at 60. This list only has 190 countries/regions on it. The ease of doing business index considers taxes, enforcing contracts, construction permits, and more.

The region also has an extensive history of governments mismanaging their economies. One of the biggest offenders is Argentina, MercadoLibre’s now third-largest market. The country has mismanaged its economy for many years, reaching a near-crisis in 2023. It had triple-digit inflation and devalued its currency by 50% against the dollar. MercadoLibre CFO Martin de los Santos discussed Argentina during the company’s first quarter 2024 earnings call:

In Argentina, we face two things happen. The devaluation of Argentina [Peso], which reduced the size of our business, and as you know, Argentina is a high-margin, heavy-margin business operation. And then we have the macro situation that obviously puts some pressure in terms of consumption. We’ve seen reduced volume and demand, even though, as you know, we manage a marketplace which is very resilient to this type of situation. So I think we outperformed the consumption in general in the country, but we did suffer some loss of volume in Argentina in the commerce side of the business. In terms of cost mismatch, I think we saw some inflation in terms of our shipping cost in Argentina. There was some pressure in that line of our P&L [profit and loss statement].

To give an idea of Argentina’s financial woes’ impact on MercadoLibre, the company reported that Argentina’s EBIT (Earnings Before Interest and Taxes) share dropped to 19% in the first quarter, compared to approximately 60% a year ago. In the second quarter of 2023, the country was the second-largest by revenue at 23.8%. By the second quarter of 2024, Argentina was the third largest by revenue at 17%.

Mercado Libre Second Quarter 2024 10-Q.

The company was fortunate that Brazil and Mexico performed much better and compensated for Argentina’s underperformance. Still, other countries’ performances coming to the rescue may not always be the case. If Brazil’s performance ever lags, MercadoLibre could have significant issues. Be aware that the company’s largest market has its own problems and risks. If you choose to invest in MercadoLibre, consider the risks of investing in the Latin American region when deciding how much to invest.

Valuation

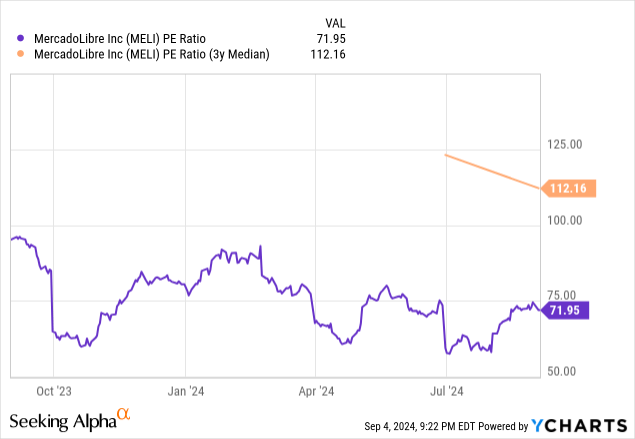

MercadoLibre’s TTM price-to-earnings (P/E) ratio is 71.95, well below its three-year median of 112.16, suggesting undervaluation. The company achieved annual EPS profitability again in 2022 after becoming unprofitable during the pandemic, so it doesn’t have a five- or ten-year median.

One potential flaw in using TTM P/E to value a stock is that it is a backward-looking metric, and the market values stocks based on their future prospects. So, let’s look at the company’s forward Price-Earnings-to-Growth (“PEG”) ratio, which is its forward P/E divided by analysts’ estimated EPS growth. MercadoLibre has a forward PEG ratio of 0.93 (forward P/E of 64.97 divided by 58.52), which some consider undervalued. If the stock traded at a PEG ratio of one, which some consider fairly valued, the stock price would be $2119.00, a 6.4% rise over the September 4 closing price.

Seeking Alpha

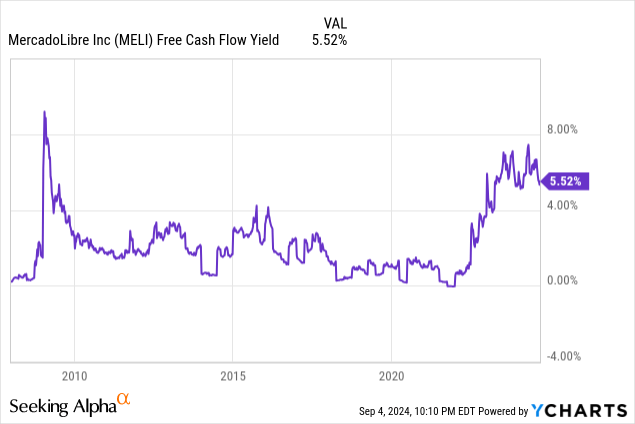

MercadoLibre’s FCF yield of 5.52% is historically high. Since the middle of 2021, its FCF has increased faster than the company’s market capitalization. The market may undervalue MercadoLibre’s FCF generation capabilities at the current FCF yield.

Let’s analyze MercadoLibre’s reverse discount cash flow (“DCF”) analysis. This DCF uses a terminal growth rate of 3% because the company should continue steadily growing its cash flow above the market average after the ten-year analysis period. I use a discount rate of 10%, the opportunity cost of investing in MercadoLibre, to reflect the high-risk level of investing in Latin America. This reverse DCF uses a levered FCF for the following analysis.

Reverse DCF

|

The fourth quarter of 2023 reported Free Cash Flow TTM (Trailing 12 months in millions) |

$5,625 |

| Terminal growth rate | 3% |

| Discount Rate | 10% |

| Years 1 – 10 growth rate | 7.6% |

| Stock Price (September 4, 2024 closing price) | $1,991.59 |

| Terminal FCF value | $10.086 billion |

| Discounted Terminal Value | $55.550 billion |

| FCF margin | 32% |

If it maintains an FCF margin of 32% over the next ten years, MercadoLibre would only have to grow its revenue at 7.6% annually over the next ten years to justify its current valuation, which it should easily be able to do. Although I don’t expect it to grow revenue at a compound annual growth rate of 40.78% as it has over the last ten years, it should increase revenue between 10% to high teens annually over the next ten years. Let’s examine why that is feasible.

Statista has estimated that Latin America’s total addressable market (TAM) for e-commerce is $272 billion. Virtue Market Research has estimated that the Latin American fintech market was $66 billion at the end of 2023. Just e-commerce and the fintech market alone may be around a $338 million opportunity. Suppose you add other areas in which MercadoLibre has established growing operations like logistics, advertising, and, most recently, streaming video through Mercado Play; the company may have at least a $500 million TAM. I have seen others estimate its TAM as high as $1 trillion. At the end of the second quarter of 2024, the company generated $17.91 billion in TTM revenue. If you believe that MercadoLibre has a TAM of $500 million, it will have only penetrated 3.5% (17.91 divided by 500) of its TAM. Suppose you think it has a $1 trillion TAM; it will have only penetrated 1.8% of its TAM.

Considering the company has only lightly penetrated its TAM, it has plenty of room to grow. Suppose it can reach 10% of a $500 million TAM; the company would generate $50 million in annual revenue. MercadoLibre would only need to average 13.20% revenue growth annually to reach that mark. If the company maintains a 32% FCF margin and grows revenue at an average of 13.2% annually, the stock’s estimated intrinsic value is $2976.23 or 49.43% over the September 4 closing stock price.

MercadoLibre is now a buy

The Brazilian online newspaper Brasil de Fato recently reported good economic news. It stated (emphasis added):

On the other hand, the government had anticipated a higher growth rate of 1.35%. This was not as surprising to the market because, according to economists interviewed by Brasil de Fato, it was the government’s actions that led to such a significant quarterly increase in [Gross Domestic Product] GDP. This rise was the highest since the end of 2020, a period when the country was recovering from the pandemic. “The result is very positive. This is due to the fiscal impulse, especially last year’s data,” summarized economist and professor at the State University of Campinas (Unicamp) Pedro Rossi. The “fiscal impulse” he mentions concerns government spending aimed at stimulating economic activity. The government of President Luiz Inácio Lula da Silva (Workers’ Party) resumed this type of public policy despite resistance from austerity-minded sectors.

The article above also mentioned how Brazilian household consumption is up, which is excellent for MercadoLibre’s e-commerce and fintech marketplaces.

In some more good news, the Mexican economy continues growing, and the Argentine economy may soon recover from a severe downturn. So, if MercadoLibre’s three largest markets trend higher, the company will hit on all cylinders and potentially achieve excellent results for at least the next several quarters.

However, the bad news is that Brazil’s political and economic situation has been historically unstable. The current government’s attempts to stimulate the economy may clash with the more conservative efforts of the Brazilian bank to control inflation. There is a genuine risk that inflation could rise to undesirable levels due to current fiscal decisions, potentially forcing the central bank to raise interest rates and possibly hurting economic growth a year or two out. Argentina’s political and economic stability can often be worse than Brazil’s, and its economic recovery could easily stall. Mexico continues to struggle with inflation. Although I like MercadoLibre’s prospects in improving Brazilian and Argentine economies, and it is still selling at a reasonable valuation, Latin American companies face much higher risks than American ones. Therefore, out of caution, I am lowering the stock’s rating from a strong buy to a buy.

Read the full article here

")

")

")