Q2 2024 Earnings Call Transcript")

")

Agenus Inc. (NASDAQ:AGEN) is a biotech which has in its pipeline a very special drug, botensilimab, which is capable of treating cancer patients with tumors not normally responsive to immuno-oncology agents. When I last wrote about the company in October, I rated the stock a buy, based on the strength of the clinical data seen to date with botensilimab and the company’s focus on getting the drug to market. Despite what I consider positive updates, however, and the biotech market rallying since that time, AGEN is down since I wrote about it. This article takes a look at where AGEN stands now.

Botensilimab/Balstilimab remains strong

Phase 2 in CRC completed enrollment months ago

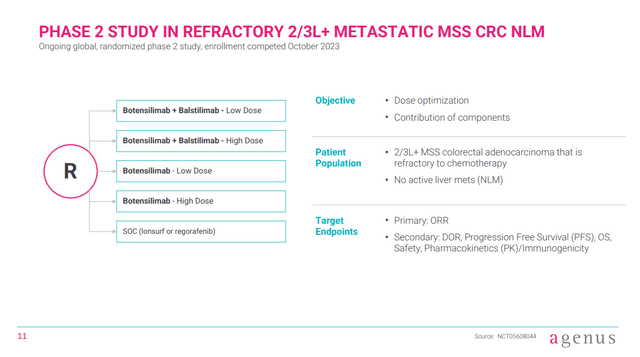

AGEN’s next-gen anti-CTLA-4 antibody botensilimab is currently in a phase 2 study, in second and third-line (2L/3L) patients with micro-satellite stable colorectal cancer who don’t have active liver metastases (MSS-CRC NLM). That trial also includes combinations with AGEN’s anti-PD-1 antibody, balstilimab, and a standard-of-care arm. The trial has an enrollment of 230 patients.

Figure 1: Overview of AGEN’s phase 2 trial of botensilimab plus balstilimab. (Corporate Presentation, January 2024.)

Since enrolment of the study completed in October 2023, and AGEN plans to submit a biologics license application (BLA) for the combination in 2L/3L MSS-CRC NLM in mid-2024, we might expect some data from the trial around that time too.

Phase 1 data in 2L/3L MSS-CRC NLM are strong

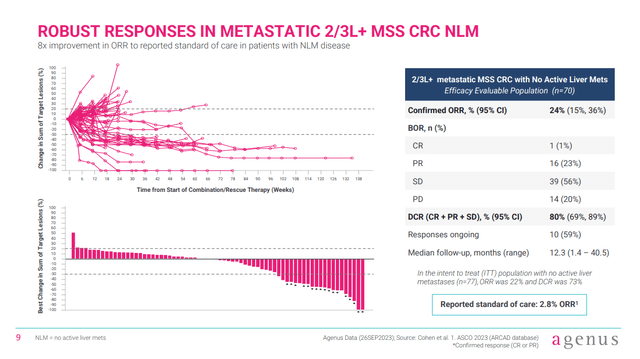

AGEN has already repeatedly presented data from an expanded phase 1 trial of botensilimab and balstilimab in a variety of cancer types. Looking at the subset of patients from the phase 1 trial with 2L/3L MSS-CRC NLM, we see an overall response rate of 24%, where the reported standard-of-care arm ORR is 2.8%. Of course, that 2.8% number does not come from within trial comparison, so results from the phase 2 study will be helpful for that.

Figure 2: Data from AGEN’s phase 1 trial in patients with 2L/3L MSS-CRC NLM. (Corporate Presentation, January 2024.)

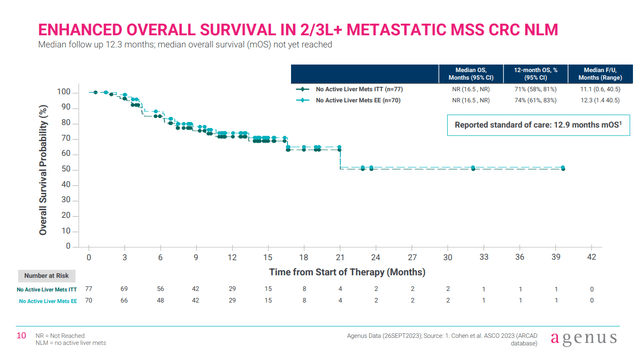

Further, the phase 1 data points to extended overall survival, where the median overall survival in 2L/3L MSS-CRC NLM patients is expected to be 12.9 months with standard-of-care. With botensilimab/balstilimab, however, the median overall survival had not been reached with a median follow up of 12 months, but seems to be in excess of 16.5 months (lower bound of the 95% confidence interval).

Figure 3:Survival data from AGEN’s phase 1 trial of botensilimab with balstilimab. (Corporate Presentation, January 2024.)

Data in the neoadjuvant setting are promising (NEST-1)

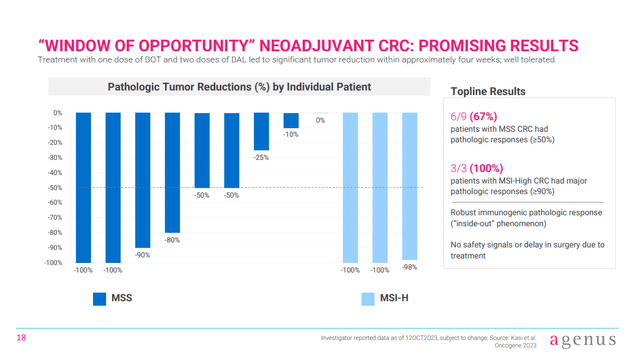

More recently, data using botensilimab/balstilimab in CRC in the neoadjuvant setting (a treatment given to make the main treatment work better, in this case drugs before surgery) have been presented. That data comes from an investigator sponsored trial called NEST-1, where six from nine MSS-CRC patients (67%) had pathologic responses (greater than 50% reduction in tumor volume). By comparison, a recent poster presentation of the data at the ASCO-GI conference notes that ipilimumab (a first-gen anti-CTLA4 antibody) in combination with nivolumab (an anti-PD-1 antibody) produced a 29% rate of pathologic responses in a previous trial.

Figure 4: Data from an investigator sponsored trial of botensilimab plus balstilimab in the neoadjuvant setting. (Corporate Presentation, January 2024.)

Of course, this is a cross-trial comparison but I’d like to see botensilimab/balstilimab developed further in the neoadjuvant setting. Indeed, patients had just one dose of botensilimab and two of balstilimab, before undergoing surgery, in some cases just a few weeks later. According to the poster presentation of the NEST-1 data, the trial has “expanded enrollment to evaluate an 8-week course over the current minimum 3-week course for MSS.,” meaning NEST-1 could still produce even better results.

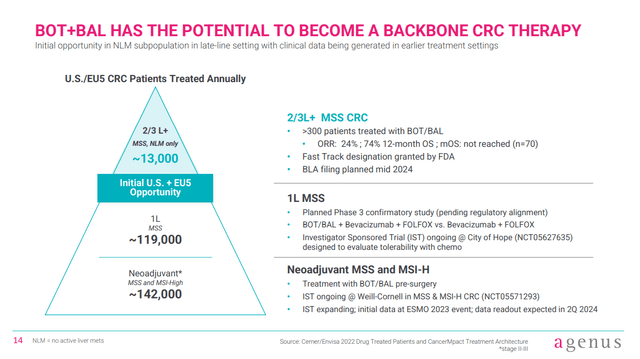

Data in 1L MSS-CRC expected in H1’24

Another catalyst still expected in H1’24 is data from an investigator sponsored trial in first-line (1L) treatment of patients with MSS-CRC. As with the neoadjuvant setting, the 1L setting in MSS-CRC represents a much bigger potential market than 2L/3L MSS-CRC. Given the combination of botensilimab/balstilimab has been impressive in the neoadjuvant setting and 2L/3L MSS-CRC NLM, it isn’t that hard to suggest the combination might produce impressive data in 1L MSS-CRC.

Figure 5: Market overview in the US and EU5 countries. (Corporate Presentation, January 2024.)

Further, the trial in 1L patients includes a comparator arm, where patients receive bevacizumab and FOLFOX alone, without botensilimab/balstilimab. As such, the readout might be considered higher impact, as no cross-trial comparison will be needed.

SaponiQx

Beyond the botensilimab and balstilimab pipeline, AGEN’s adjuvants have attracted the interest of The Department of Defense. Notably, SaponiQx, a subsidiary of AGEN, has an adjuvant called STIMULON QS-21, that is already used in an approved vaccine, GSK plc’s (GSK) Shingrix. On February 15, the Defense Threat Reduction Agency awarded a 5 year contract worth up to $31M to Ginkgo Bioworks (DNA) and SaponiQx. The contract covers the development of next generation vaccine adjuvants. While that contract has just been awarded, developments in the progress of developing those new adjuvants provide a future catalyst for AGEN, and it is nice to have funding coming from the government given AGEN’s cash position.

Financial Overview

AGEN had cash, cash equivalents and short-term investments of $106.3M at the end of Q3’23, and reported a net loss of $64.5M for Q3’23. R&D expenses were $51.4M during Q3’23 and G&A expenses were $18.9M during the same quarter. Net cash used in operating activities was $183.8M during the first nine months of 2023, and based on that rate of cash burn, we might expect AGEN to run out of cash in just over 5 months from the end of Q3’23, i.e., February/March 2024. AGEN also had $13.4M in principal debt outstanding as of September 30, 2023, so taking that into account, AGEN’s cash wouldn’t even make it to March 2024 if it had not taken steps to raise more cash and reduce expenses.

AGEN has previously taken steps to reduce its expenses, however, announcing in August 2023 it was reducing its workforce by 25%, and postponing clinical and preclinical programs other than botensilimab and balstilimab. AGEN said at the time it expected this to produce $40M in savings by year-end 2023. As such, cash burn in the first nine months of 2023 is probably not an ideal estimator of cash burn going forward. Further, AGEN’s Q3 financials came with the acknowledgement that the company would try to raise more cash, but without issuing shares.

We are actively pursuing immediate prospects for additional cash infusion that don’t involve stock issuances, including a milestone payment from one of our partnered programs, expected by the end of 2023. In addition to this expected milestone, we are in the process of selling two non-strategic assets and the partial sale of other milestones and royalties due to Agenus from our partnered programs. These three sales are expected to close by the end of the first half of 2024. With our end of third quarter cash, cash equivalent, and short-term investment balance of $106.3 million, along with these four planned transactions, we believe we are sufficiently funded through the end of 2024. In addition to these planned transactions, we are also in advanced discussions for a potential structured financing for BOT/BAL as well as a potential corporate collaboration with a large pharma or biotech company.

AGEN Q3’23 earnings release, November 7, 2023, emphasis mine.

Indeed, on December 11, 2023, AGEN reported it would receive a $25M milestone from Bristol Myers Squibb (BMY) as BMY was dosing patients in a phase 2 study of a drug AGEN licensed to BMY in 2021. On the other hand, we still haven’t heard about the selling of non-strategic assets, and I wonder if a potential acquirer is attempting to lowball AGEN given it is known the company needs money. The fact that management at least delivered on the milestone payment increases my confidence they can sell at least one of the assets or partial milestones/royalties. Lastly, AGEN has an at-the-market facility that it has used previously to raise cash.

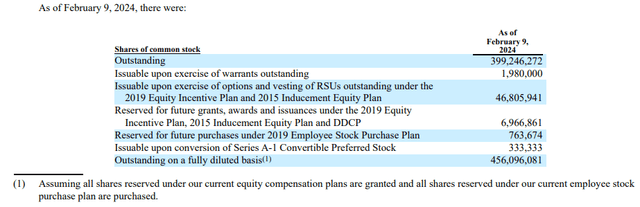

As of February 9, 2024, there were 399,246,272 shares of AGEN’s common stock outstanding.

Figure 6: Screenshot of table from AGEN proxy statement discussing stock outstanding and issuable. (February 15, 2024, PRE 14A filing.)

That information comes from a PRE 14A filing, where AGEN has noted it plans to put to a shareholder vote, on April 3, a potential 1-for-20 reverse split. A potential rationale for this is to get the stock above $5, as many institutions might not be able to buy into a stock with a price below $1 or indeed below $5.

There still has been some institutional support, even with the share price below $1, however. For example, a subsequent SC 13/G filing by Point72 Asset Management and Steven A Cohen notes a number of 414,246,272, as Point72 Associates had purchased 15,000,000 shares in an at the market offering from the issuer (AGEN). At a price of $0.68, 15M shares would raise AGEN gross proceeds of $10.2M. Using the 414M number for the shares outstanding then gives a market cap of $281.7M.

Conclusions, rating and risks

I’m pretty confident botensilimab is set to be a rockstar drug, and is set to demonstrate that again in 2024, both with data from an investigator sponsored trial in 1L MSS-CRC, and the 230 patient phase 2 study in 2L/3L MSS-CRC NLM. I’d be rating AGEN a strong buy if the company wasn’t in a position where it might have failed to raise enough cash, through asset and royalty sales, soon enough and instead issue some more stock. Nonetheless, I rate the name a buy because even if the company has to do that, I think a private placement to raise funds would allow the stock to rally as a funding overhang is probably what is holding this stock down. Recent support from Steven A Cohen’s Point72 shows that the name is still getting support from institutions and a reverse split, if passed, might help other institutions support the company.

The risks of any long in AGEN are several fold, a few of which are worth discussing here. Firstly, if AGEN’s upcoming Q4’23 earnings show cash burn continues at too high a rate, the fact that the company has brought in $25M from a milestone payment and ~$10M using the ATM won’t be too reassuring. Of course, the company could have brought in more than that using the ATM, we just don’t know since it could have been sold gradually using the ATM to no single investor. This is especially true since we haven’t had news on the sale of non-strategic assets or the partial sale of milestones/royalties.

Further, delays in the company’s trials are also a risk, investigator sponsored trials, like the trial in 1L MSS-CRC, are sometimes subject to delays. Further, the company’s own trials can be subject to delays, although AGEN has a little more control in that situation and the phase 2 in 2L/3L MSS-CRC NLM is already fully enrolled.

Lastly, there is the risk that new clinical data disappoints. AGEN’s phase 2 study in 2L/3L MSS-CRC NLM is going to be a major part, if not the centerpiece of a mid-2024 BLA filing. As such it doesn’t produce data that looks as good as the phase 1 data, then the stock could fall.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here

Q2 2024 Earnings Call Transcript")

")