")

Last week, BASF (OTCQX:BASFY) (OTCQX:BFFAF) reported its Q4 and FY 2024 results. Today, we are back to comment on the German Chemical players; however, before looking at the financials, we report the two following key takeaways: 1) Gas Price Continues to Decline, and 2) the EU Discount to the USA is unjustified. Aside from a positive forward-looking view on the EU chemicals, we anticipate these two macro trends could support BASF re-rating.

Gas Price Evolution

One year later, we believe our thesis might be the right one: Lower EU Gas Prices, BASF Is Our Top Pick. As a reminder, gas remains the most significant cost item for the European chemical industry, accounting for about 76% of their bills on average. EU chemical companies will continue to produce, buoyed by government grant packages. However, we noticed the profitability was weak, especially in ethylene and soda ash production. We were encouraged to hold the European chemicals thanks to an average sector net debt-to-EBITDA ratio of 0.9x, well below the 2008/2009 level of 1.4x.

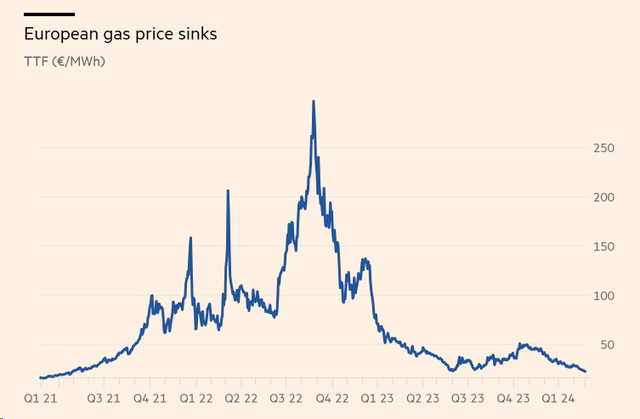

It is too early to declare the EU energy crisis over, but we believe we have already reached a milestone. Last week, the natural gas price returned to pre-crisis levels, falling below €23 per Megawatt hour. This is the first time since the Ukraine war.

There are three main reasons why the price is going down. Europe is approaching the end of the winter season with storage 65% complete, above its ten-year average of 54%. Warmer temperatures than usual supported this.

Secondly, there was a record import of liquefied gas. Thirdly, we should also mention a step-up in energy production from alternative energy sources such as nuclear and wind.

Additionally, energy-saving efforts have helped avoid a deficit. Russian natural gas exports to Europe are now marginal compared to the past. This was possible thanks to a higher dependence on North Africa (Eni Is Ensuring Gas Diversification).

European gas price falls to pre-energy crisis level

Source: FT

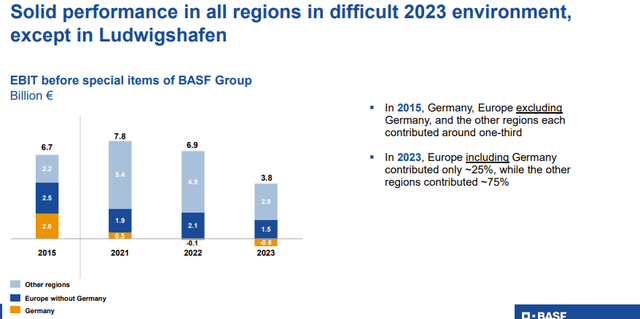

BASF CEO “remains strongly committed to the Ludwigshafen site.” That said, the Ludwigshafen site has been unprofitable since 2022. The precise aim is to transform Ludwigshafen into the leading low-CO2-emission chemical production site. This should support the company’s ongoing profitability.

BASF EBIT by Region

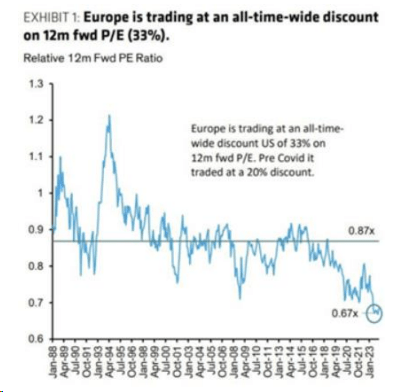

EU P/E Evolution

On a macro basis, the price-to-earnings ratio (expected for the next 12 months) of the EuroStoxx 600 index is at its lowest level compared to the S&P 500 index. European stocks are trading at a 33% discount to their US counterparts. This is a historic low.

P/E US vs EU

Q4 and Fiscal Year 2024 results

BASF’s 2023 ended with sales of €68.9 billion, down 21% from €87.3 billion in 2022. Last year, the company recorded an adjusted EBITDA of €7.7 billion, signing a minus 28.7% on an annual basis and an adjusted EBIT of €3.8 billion (-44.7%). The last line of the balance sheet returns to report a net profit of 225 million after a loss of 627 million in 2022. The free cash flow reached €2.7 billion, a decrease of 18.5%. In 2023, the company recorded a double-digit percentage of core operating profit in all regions due to a challenging market environment. Low demand and high energy prices were the main reason.

The CEO explained that “in absolute terms, BASF delivered a positive earnings contribution.” Results show that BASF’s home country suffered substantially negative earnings in Ludwigshafen. In Q4, the company’s sales declined by 17.9% due to lower prices and negative FX. We are not surprised by this performance. Last year, we analyzed BASF with a publication called ‘Disappointing Results.’ We anticipated a €3 billion free cash flow deficit, pointing out how BASF FCF will be negligible until 2025. Furthermore, we expected higher leverage, forecasting a flat DPS over the period while increasing net debt/EBITDA by 0.3x per year.

Changes in Estimates and Ongoing Upside

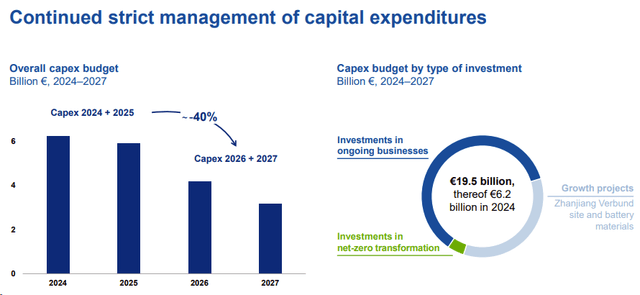

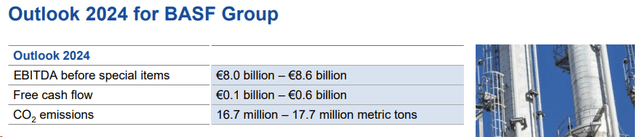

The company pre-released its Fiscal Year 2023 EBIT on 19 January. We viewed the results, but today, we update BASF estimates with the relevant new information. This includes a 2024 EBITDA outlook in the €8/€8.6 billion range and CAPEX of €6.2 billion. That said, BASF also lowered the investment CAPEX to €19.5 billion versus a previous estimate of €20.5 billion.

BASF CAPEX Outlook

The new EBITDA guidance implies an annualized pickup of approximately 3% compared to the H2 2023 results. Our team believes this is somewhat conservative. BASF projects Free Cash Flow guidance between €0.1 billion and €0.6 billion with a limited cash conversion of only 4%.

BASF 2024 Outlook

Following the Wintershall Dea agreement, BASF will receive $1.56 billion and new shares from Harbour Energy. The Wintershall Dea EV was $11.2 billion, encompassing the outstanding corporate bonds worth approximately $4.9 billion. BASF has exited the gas and oil business and has a potential value creation through Harbour’s listing on the LSE. In addition, considering BASF’s total dividend payment, the company will cash out €3 billion; Wintershall Dea’s disposal served to pay 50% of BASF’s 2024 dividend payment.

In addition, the company announced a new restructuring plan that would affect the Ludwigshafen site. Unfortunately, the program will lead to further job cuts, but BASF’s goal is to save €1 billion annually for the next three years. This is in addition to the €1.2 billion of cost savings previously announced.

Looking at the core business, excluding metals, Q4 volumes were up by +2.6%, implying that demand has bottomed out. We believe the company doesn’t expect a further weakening in demand (even due to lower destocking activities).

Valuation and Risks

We usually value chemical players using a mid-cycle earnings estimate. That said, BASF earnings have been disruptive since the evolution of gas prices. In our previous analysis, we were anticipating higher debt; however, BASF was able to exit Wintershall Dea and lower CAPEX investments. In a challenging economic environment, BASF targets a mid-EBITDA of €8.3 billion, compared to a mid-cycle EBITDA of approximately €10 billion. Valuing the chemical player with our 6.5x EV/EBITDA and considering the €17 billion in debt, we derive a price target of €55 per share ($15.4 in ADR). This valuation is also supported by a low price-to-book value vs. BASF’s historical 10y median (1.5x vs. 3.4x). A 7.3% yield offers the downside protection. On a 12-month view, this implied a total return of >25%.

On the risks, BASF’s earnings are linked to oil and natural gas prices. In addition, the company is affected by consumer slowdown and industrial production. BASF is linked to EU auto productions. There is also a downside to the execution of the new Chinese site.

Conclusion

BASF dividend was confirmed. We are more optimistic about debt evolution thanks to lower CAPEX and Wintershall Dea exit. The company’s guidance looks conservative, and considering the new cost-saving plan, we believe BASF is in better shape in the future. If we add the lower gas price, BASF could be (again) Our Top Pick.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

Q2 2024 Earnings Call Transcript")

")