Q2 2024 Earnings Call Transcript")

Growth stocks have had quite the run in recent months, and while it’s tempting to jump on the bandwagon, I remain skittish around plopping hard-earned capital at speculative valuations. While I may be missing out of short-term gains, I’m more interested in protecting long-term returns.

Besides, with the market chasing growth stocks, that capital has to come from somewhere, and it appears to be at the expense of quality dividend stocks, whose yields have gone up materially since December after falling out of favor with investors.

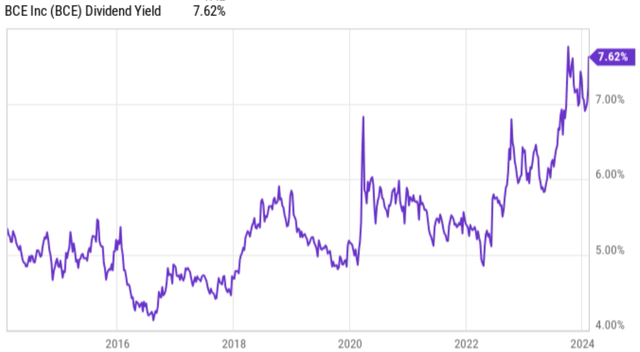

This brings me to BCE Inc. (NYSE:BCE), which I last covered in October with a “Strong Buy” rating, highlighting its outperformance over its American peers over the past 5 years and its growth prospects in 5G and fiber. The stock has seen its ups and downs since then, rising above $40 before falling back down to $37.53, at present, representing a 2.7% share price decline since my last piece and pushing the dividend yield to an appealing 7.6%, near the highest level in at least a decade.

BCE Stock (Seeking Alpha)

In this article, I revisit the stock to discuss its recent Q4 earnings and highlight why BCE is an appealing bargain for high income investors, so let’s get started!

Why BCE?

BCE is one of the Big 3 Canadian telecom giants and like in the U.S., has seen industry consolidation after Rogers Communications (RCI) finally closed its acquisition of Shaw last year. BCE is also the most diversified compared to peers, as it has wireless, broadband, and TV/Media offerings for its consumers.

While BCE’s less than stellar 17% decline in share price over the past 12 months has been disappointing, its operating fundamentals suggest otherwise. This is reflected by BCE’s recent full year 2023 results, during which BCE saw 2.1% YoY revenue growth. Specifically in Q4, BCE’s revenue grew by 0.5% YoY and saw healthy adjusted EBITDA growth of 5.3% YoY, driven by EBITDA margin expansion of 190 basis points to 39.7%.

Importantly, these results translated to bottom line growth as adjusted EPS grew by 7% YoY during the fourth quarter. BCE’s faster bottom line growth compared to the top line was a result of a deceleration in capital spending as it relates to the fiber network buildout. The fiber network spending reduction during Q4 was actually more than originally planned with $105 million in incremental pullback in CapEx.

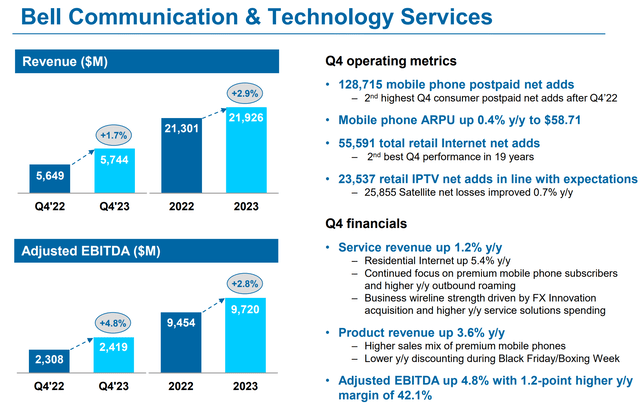

At the same time, BCE is seeing strong momentum in its bread and butter mobile business, with 129K mobile phone postpaid net adds during Q4, representing its second highest Q4 consumer postpaid net adds after a record breaking Q4 of 2022. BCE is also seeing a favorable pricing environment, as mobile phone ARPU (average revenue per user) grew by 0.4% YoY to C$58.71, and saw an impressive 44K total retail internet net additions, its second best Q4 performance in 19 years. As shown below, the Communication & Technology saw both sales and EBITDA growth in Q4 and full year 2023.

Investor Presentation

Looking ahead, BCE should continue to see benefits from its fiber buildout and from the surpassing of its 5G and 5G+ coverage objectives. These capital investments have enabled BCE to offer its customers symmetrical internet speeds of 3 GB in 6.5 million locations, marking an improved speed over cable competitors who cannot match this speed. This has enabled BCE to grow residential internet revenue by 7% in 2023, and I would expect for this momentum to continue at least in the near term, considering BCE’s leadership position in internet speeds.

Encouragingly, BCE recently secured new 5G+ spectrum licenses and now has the most 5G+ spectrum in Canada, which was acquired at the lowest cost among its competitors, and this could result in continued momentum around net new postpaid phone adds in 2024, especially in areas that didn’t previously have adequate 5G coverage.

Risks to BCE include higher interest expense in the current higher interest rate environment. This is reflected by the expectation of C$200 million YoY increase in interest expense in 2024. This, combined with higher depreciation and amortization expense due to capital investments results in guidance for a 2% to 7% YoY decline in adjusted EPS for the full year 2024. Given the wide range of this bottom line guidance, a number of factors including the direction of interest rates as well as the macroeconomic backdrop in 2024 can have outsized influences on this year’s results.

Nonetheless, BCE carries a BBB+ investment grade credit rating from S&P, which should help to buffer the impact of higher interest rates on debt refinancing. It also has sizable liquidity of $5.8 billion, comprised of untapped availability on credit lines and $547 million in cash on the balance sheet. BCE’s net debt to EBITDA ratio is somewhat elevated at 3.5x, due to capital investments related to 5G and fiber buildout in recent years, and I would expect for the leverage ratio to trend down with reduced capital spending this year and growth in EBITDA.

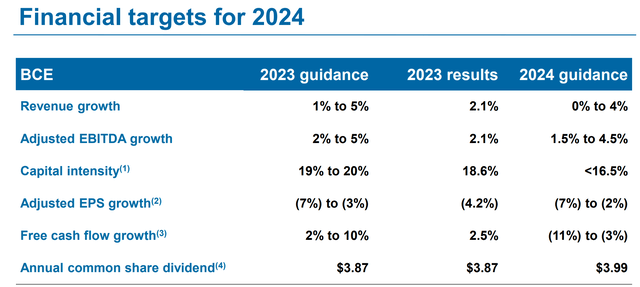

Importantly, BCE has well-laddered debt maturities with a long weighted average debt term of 12 years at an average 3% interest rate with low 18% floating rate exposure. As shown below, capital intensity for 2024 (as defined by capital expenditures divided by operating revenues) is expected to decline to below 16.5% this year compared to 18.6% in 2023.

Investor Presentation

Notably for income investors, BCE has grown its dividend annually for 16 consecutive years, and this includes the most recent 3.1% increase for 2024. The new dividend rate is also well-covered by a 45% payout ratio based on TTM operating cash flows, and this even assumes no growth in OCF. As shown below, BCE’s dividend yield currently sits at the top end of its 10-year range.

YCharts

Lastly, I continue to see value in BCE at the current price of $37.53 with a price-to-cash flow of just 5.7x, sitting at the bottom of its 5-year range (outside of the 2020 pandemic timeframe), which mostly trended between 6x and 8x, as shown below. With this pricing, I believe the market has more than baked in headwinds from higher interest rates while ignoring the underlying operating strengths of the business. Analysts also expect a long-term annual EPS growth rate of around 5%, which combined with the 7.6% dividend yield could result in above market average returns.

BCE P/CF 5-Yr Range (Seeking Alpha)

Investor Takeaway

BCE’s recent full year results have shown solid operating fundamentals, including revenue and adjusted EPS growth, driven by strong performance in the mobile and internet business. The company also has a favorable outlook with its fiber buildout and 5G coverage objectives. However, there are risks to be aware of, such as higher interest expenses in the current environment.

Nonetheless, BCE maintains a strong credit rating and liquidity position to help mitigate these headwinds. Income investors may like that the company has a long history of dividend growth and a well-covered dividend. With its current valuation at the bottom of its 5-year range, there may be potential for above market average returns for long-term investors. As such, I maintain a ‘Strong Buy’ rating on the stock.

Read the full article here

Q2 2024 Earnings Call Transcript")

")