Q2 2024 Earnings Call Transcript")

")

BECN’s Business Prospect

Beacon Roofing Supply (NASDAQ:BECN) distributes building products, including roofing materials, through 500 branches in the US and Canada. It offers its own private label brand, TRI-BUILT, and has a digital account management suite, Beacon PRO+. Pursuing its long-term plans (Ambition 2025), it has made Investments in greenfields and gained market share through M&As. The acquisition of new branches has contributed significantly to its FY2023 topline. Also, the digital integrations with solutions providers helped improve operating margins.

The decline in new residential construction and strong seasonal decline can hold back BECN’s growth prospect in the near term. The company will look to even it out through inventory reduction and productivity enhancement. Cash flow improvement in 2023 is a testament to its improving health. However, despite robust liquidity, the company’s debt level is too high for comfort. The stock appears reasonably valued versus its peers. Investors can expect limited returns in the short term before the stock price picks up over the medium term. I suggest investors “hold” it.

In Pursuit Of A Long-Term Strategy

BECN’s Q3 2023 Earnings Presentation

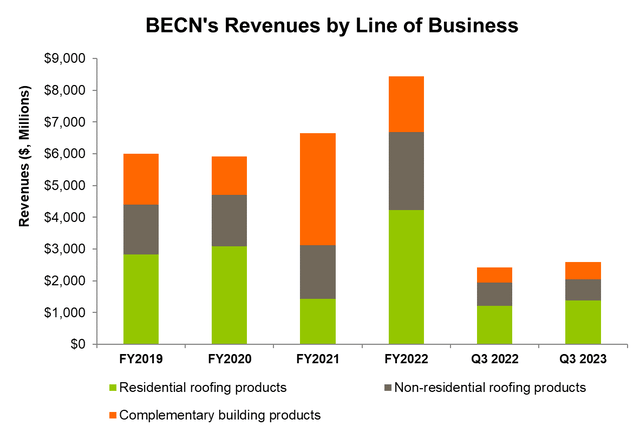

Beacon Roofing’s primary business revolves around repairing and replacing exterior weatherproofing products in the building and construction sector. In 2023, economic uncertainty adversely affected the new builds and existing for-sale units. Channel destocking reduced sales of new commercial construction activity. However, the overall construction activity has not abated significantly. Some other companies in the construction industry have changed their strategies. For example, BrightView Holdings (BV) recently lost some interest in the residential market. Instead, they started looking at the commercial business (commercial landscaping) because of a lackluster residential market, as I discussed in my article here.

In these circumstances, BECN will strengthen its service model by supporting its sales organization, digital offerings, and private brand categories. In addition, it will increasingly depend on inorganic growth through M&As. In February, it acquired Roofers Supply, which is expected to grow its service geography and design services in the Carolinas. In October 2023, it acquired Garvin Construction Products, which supplemented its waterproofing business. It also helped it expand in the Northeast.

Earlier, in Q2, it acquired four companies – All American Vinyl Siding Supply, S&H Building Materials, Crossroads Roofing Supply, and H&H Roofing Supply. As part of its The Ambition 2025 strategies (announced in February 2022), it acquired 15 new branches in 9M 2023, opened seventeen new branch locations, and concentrated on increasing digital sales (22% higher than a year ago).

Related Strategies

Investments in greenfields and acquisitions are key levers to BECN’s growth plans. It began with a plan to open 15 locations at the start of 2023 and ended up with at least 19 (or more). Additional branches shortened the average distance and time to serve our customers’ orders. This gives the company the ability to gain market share. The company estimates the new branches will contribute nearly $250 million to the FY2023 top line. The company approaches this lumpsum with OTC or on time and complete. An OTC is an operating model in which networked branches share inventory, systems, equipment, and employees. The goal is to improve customer service levels, lower service costs, and optimize inventory levels.

The other leg of BECN’s current strategy is to build online capability. The company’s digital integrations with solutions providers resulted in a 22% year-over-year increase in digital sales. In Q3, sales through the online platform delivered a better margin (150 basis points higher) than the offline channels. It also channeled a high percentage of sales from the residential category (22%). So, I think the company will continue to invest in this area.

Q4 Outlook

Seeking Alpha

Although BECN’s non-residential business underperformed in 9M 2023, its management expects all three operating segments to register sales growth in Q4. In October, sales per day grew by 13%. It estimates sales per day to grow by 11% to 13% year-over-year in Q4, including the added revenues from Coastal Construction Products (recently acquired). Its gross margin can decline marginally from Q3 by 50 basis points to 25.5%. According to the company’s preliminary results announced in January, Q4 net sales can decrease by 11% compared to Q3, while its adjusted EBITDA can decline by 32%. Gross margins, however, would be relatively resilient at 25.7%.

A lower margin in Q4 can stem from higher product costs. In Q4, it will look to balance the margin with increased product availability through inventory reduction and productivity enhancement. In comparison, in Q4 2022, its gross margin expanded from significant inventory profits. The company’s cash flows can also improve in Q4. It also revised its adjusted EBITDA guidance to a range of $910 million-$930 million from its previous guidance.

Industry And Economic Factors

FRED data

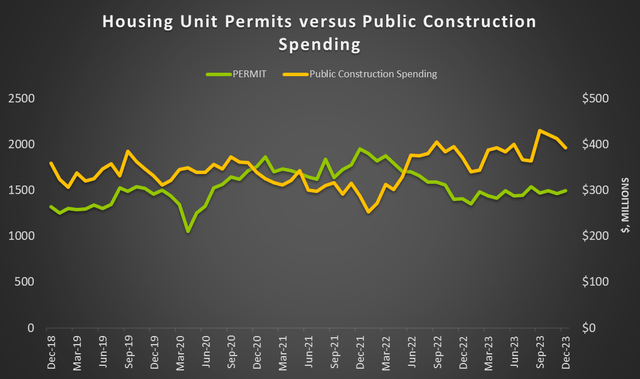

Over the past two years, the number of new privately owned housing unit permits has declined by 23%. However, the market appears to be stabilizing, as it moved up marginally in Q4 (Sep-Dec). Over the past two years, public construction spending increased by 36% until December 2023.

Although it declined in Q4, it has far outpaced the dwindling residential market. Quarter-over-quarter, the US GDP and the US consumer price index (or CPI) increased almost equally from Q2 to Q3. Over a longer period (two years), the US GDP growth rate has outpaced CPI. So, the economy does not throw any warning signs for BECN’s near-term outlook.

Analyzing The Q3 Performance

BECN’s Filings

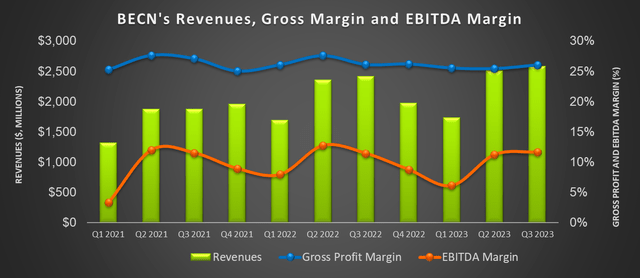

Year-over-year, BECN’s revenues increased by 7% in Q3 2023 due to increased organic volumes and slightly higher average selling prices. In August 2023, its asphalt shingles price increased, contributing to a higher margin. Investors may note that asphalt shingles comprise the largest share of the company’s residential market products. While organic Greenfield’s volume contributed 1% of the revenue rise, pricing contributed slightly less. Non-discretionary residential R&R demand was high in Q3 and offset new construction headwinds. However, non-residential roofing sales declined by 6% per day due to destocking and lengthening project cycles.

BECN’s gross margin remained steady over the past several quarters until Q3. Its EBITDA margin improved significantly in Q2, following improved labor productivity and indirect cost input management. Increased operating profits and active working capital management generated substantial cash flow, which the company deployed for growth initiatives and returns to shareholders.

Cash Flows And Balance Sheet

In 9M 2023, BECN’s cash flow from operations increased significantly (5.4x) compared to a year ago. However, the company’s revenues remained relatively unchanged, and favorable change (i.e., lower) in inventories, accounts payable, and accrued expenses led to a rise in cash flow. Free cash flows increased even more impressively (34x up) in 9M 2023 from a year ago. I expect the company to continue generating positive free cash flow as it grows profitably and invests in its greenfields.

BECN’s liquidity was $1.06 billion as of December 31, 2023. Its leverage (debt-to-equity) of 1.26x, however, deteriorated (i.e., increased) from a year ago and is lower than its peers’ average (BCC, MSM, and JELD). During Q3, it repurchased preferred shares, reducing the as-converted share count by 13% of the equity outstanding. As a result, its preferred dividend was lowered by $24 million annually. Plus, it repurchased common shares worth $100 million year-to-date. This was a part of its Ambition 2025 program. So, since 2022, its as-converted share count has been reduced by ~21%.

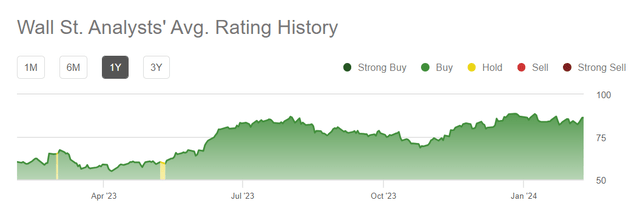

Analyst Rating

Seeking Alpha

Eight analysts rated it a “buy” (including “Strong buy”) in the past 90 days, while six sell-side analysts rated BECN a “hold.” None of the analysts rated it a “sell.” The consensus target price is $100.8, suggesting a 17% upside at the current price. I think, given the medium-term drivers, sell-side analysts are reasonable in their estimates.

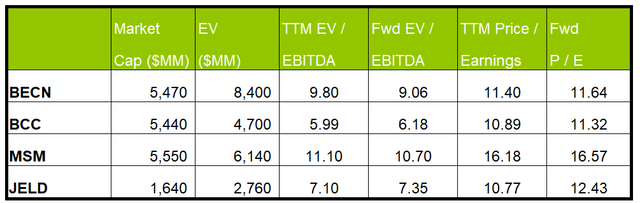

Relative Valuation

Author Created and Seeking Alpha

BECN’s forward EV/EBITDA multiple contraction is steeper than its peers, typically resulting in a higher EV/EBITDA multiple. This means its adjusted EBITDA is expected to rise more sharply than its peers. The company’s EV/EBITDA multiple (9.8x) is higher than its peers’ (BCC, MSM, and JELD) average (8.1x). So, the stock appears to be reasonably valued.

If the stock trades at the past average, it can increase by 24% from the current level. If the stock trades at the industry average, it can decline by 12%. Given the near-term drivers, I think the stock may rally down now, but it should back up to yield steady returns in the medium term.

What Are The Risks?

As I discussed above, BECN’s business critically depends on residential and non-residential construction, which, in turn, depends on credit availability, interest rate, and foreclosure rates that directly affect new housing demand. The interest rate hike in the US reduced demand in the residential market, as we saw over the past several quarters. Economic indicators like employment levels, consumer confidence, and the economy’s health also influence consumer behavior. The housing sector becomes relatively vulnerable in an economic downturn because consumer spending shifts to essential products. Although the economic parameters are healthy for now, the global geopolitical uncertainty can spell concerns in the near-to-medium term.

BECN typically experiences low demand for the quarter ended March 31. The cold weather patterns and winter construction cycles hurt new construction. Given the seasonality, I expect the company’s sales to slightly downturn in Q4 2023 through Q1 2024.

What’s The Take On BECN?

Seeking Alpha

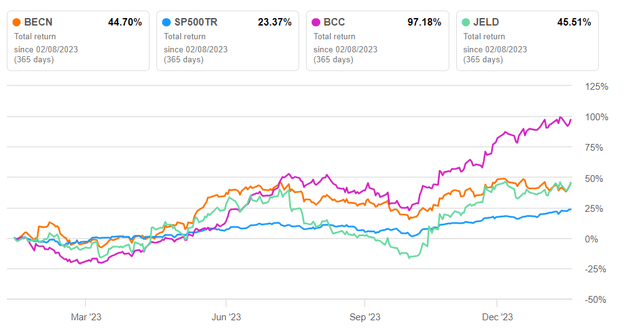

BECN wants to push sales through its sales organization, digital offerings, and private brand categories. As the end markets, especially the residential market, slowed down, the company aspires to grow inorganically. As part of its The Ambition 2025 strategies, it acquired and opened several new branches in 2023 that augmented its roofing and waterproofing business. The additional footprint should also lower the cost to serve and optimize inventory levels. Lower inventory will also help the company’s cash flows by decreasing working capital requirements. The rise in asphalt shingles prices also contributed to higher margins in Q3. So, the stock underperformed the SPDR S&P 500 Trust ETF (SPY) in the past year.

However, concerns remain over the sedate residential market and the global economic outlook. Although cash flows improved substantially in 9M 2023, high leverage can trigger financial risks in the event of a high cash requirement as share repurchases continue. The fundamental drivers and the relative valuation should prompt investors to “hold” it at this level.

Read the full article here

Q2 2024 Earnings Call Transcript")

")