")

Bioceres (NASDAQ:BIOX) is an agricultural supply company with an established position in adjuvants and breaking into the seed genetics and biopesticides markets.

I have been covering BIOX with a Hold rating since April 2021, with the latest article in December 2023. I have been generally skeptical of Bioceres because of its debt structure, some aspects of its governance, and price.

In this article, I review the company’s 2Q24 and 1H24 results, published last month. I analyze the reasons for the substantive quarterly YoY revenue growth and soft developments in their HB4 pipeline and warn about news on the company’s debt.

I maintain my Hold rating, specifically on the lack of clarity around the company’s high current debt maturities.

Thesis summary

My thesis on Bioceres is that the company has several growth potential products but has mishandled that growth in debt and dilution.

The company is famous for having commercialized (not invented, and not owning) the drought-resistance HB4 gene trait for wheat and soy. These are the first drought-resistance traits for soy and wheat and the first GMO wheat variety in the world.

As an important caveat, Bioceres does not own the core IP for these products. It has to pay royalties to the Argentinian science institute and a holding company (Bioceres PLC), the technology owners.

The company has also acquired other agrotech companies, like Moolec (MLEC), a developer of cultivated protein, and Marrone (ex-MBII), a developer of biobased pesticides.

Neither the HB4 nor other developments are profitable. These are growth markets that require investment in R&D and commercialization.

The company’s profit engine is the Argentinian Rizobacter, a leader in more traditional adjuvant and crop protection products. This business segment can only be analyzed yearly with 20-F data but is not growing much.

The problem was that to accelerate growth, the company invested too much in these new technologies, adding debt and diluting the company shareholders.

In addition, the company has not been good at communicating key aspects to minority shareholders. These include the royalty scheme with Bioceres PLC, not reporting information on Rizobacter quarterly, and not reporting clearly on its debt maturities and refinancing plans.

2Q24 results

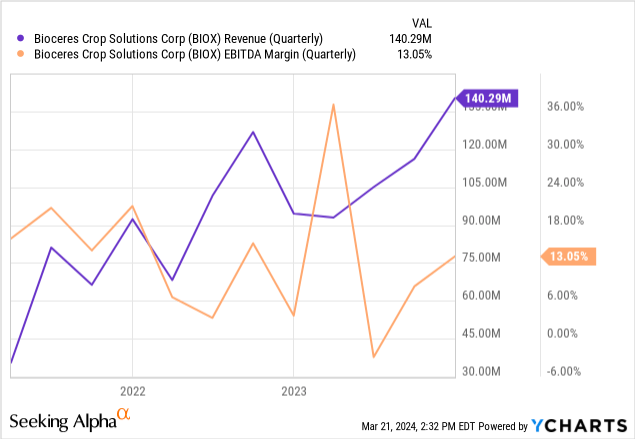

Expected revenue recovery: Bioceres posted a good YoY quarterly comparison, growing 50% for the quarter (16% for the 1H24 period vs 1H23). This recovery was expected given that the company suffered the setback of one of the worst historical droughts in its core Argentinian market in 1H23. This affected the purchase of Rizobacter’s crop protection and nutrition products.

Good operating leverage: On the other hand, the company’s cost structure was stable, with total operating expenses of $75 million despite the revenue growth. This helped the profitability metrics. It also evidenced some of the positive aspects of the company’s business model in terms of incremental growth at high margins. Overall, the quarter ended with operating profitability of $16 million, from which $7 million is removed via interest on its debt, leaving about $9 million in pre-tax profits or $6 million in net profits (using normalized tax rates). 2Q is a strong quarter for the company in terms of seasonality because Rizobacter sells crop protection and nutrition products to farmers in its core Argentinian and Brazilian markets.

Argentinian peso devaluation: The company also reported $8 million in income taxes. Compared to $9 million in pre-tax profits, this seems excessive. The reason was that the Argentinian peso devaluation caused a peso-based increase in the value of certain assets, which cannot be offset yet via inflation accounting. The result is a deferred tax that should be reversed in future quarters.

Soft developments

There were also comments on the soft side of the business in the quarterly earnings call for 2Q24.

HB4 ‘grows’ via inventories: As commented on in my latest article, the Seeds segment is growing fast, at 80% YoY rates in 2Q24. This segment contains sales from the wheat HB4 varieties. HB4 soy will start commercialization in FY25 and is currently under breeding programs only.

However, it is difficult to grasp how much of this growth comes from actual market penetration because 1Q24 and 2Q24 show significant wheat sales as inventory, which should not have been classified as a seed product. Instead of selling HB4 seeds to farmers, Bioceres is selling some of its unused inventory of seeds to the food chain, as if it were a farmer, at much lower margins.

Last year, the seed segment sold $29 million at 55% gross margins and $54 million at 34% margin this year. Assuming the $29 million were still sold at 55% margins (something that management pointed to in the earnings call when it said that margins on the HB4 as product and not inventory were flat to up), the remaining $24 million in revenues have a margin of around 10%, average in grain commodities. This indicates that most improvement comes from inventory sales, not package sales.

Commercial front: In the call, management also brought up advances on the patent, approval, and yield aspects of the commercial front. These developments do not immediately affect sales but give an idea of progress in implementing the commercial plan.

The HB4 soybean product’s patent protection has been extended to 2042 via staggered patents. HB4 soybean gained approval in several Asian economies (including Australia, New Zealand, and Malaysia), already covering 80% of Latin American export destinations in Asia. Finally, the newer varieties of HB4 wheat (second and third generation) rank on par with other commercial varieties’ yields in high-yield environments (whereas they are above the commercial varieties in low-yield environments).

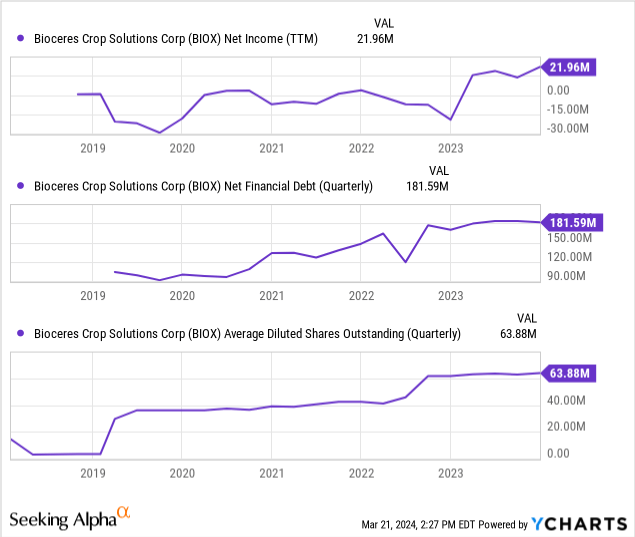

Unspoken risk of debt

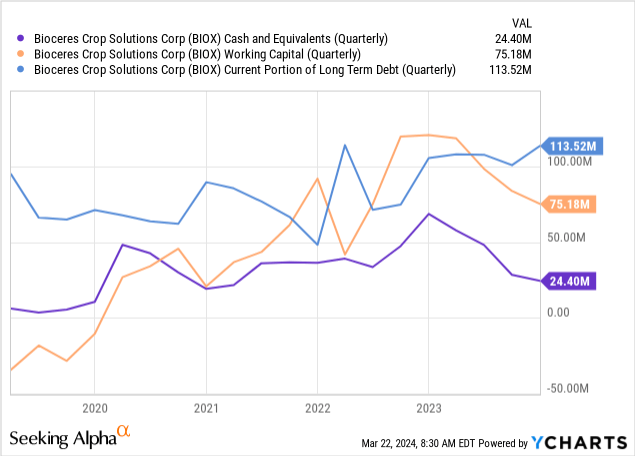

Bioceres has (once again) not made any mention on the release, nor the earnings call, about the impending debt payments that can be read from the current borrowings account at $113 million, against only $25 million in cash.

The company does not even post the maturity schedule of these obligations on its quarterly financial statements. The company’s 20-F shows some information (not presented in a single table as customary) where the company faces bond maturities for at least $45 million this calendar year, but $52 million in borrowings remains unexplained. The company does not even mention if it has a credit facility and under what characteristics. We know that most of those borrowings are dollar and not peso-denominated.

As mentioned in my previous article, this is another sign of a lack of clear communication with shareholders on such a critical topic as current liquidity needs.

Valuation and rating

I would not consider a company facing liquidity risks in the short term, and that is unclear when communicating such an important topic. The investor is hoping for the best in that scenario.

Potential negative resolutions to the current debt problem are refinancing at higher rates (Bioceres’ current cost of debt is 7%, but it has recently financed itself above 14%, as explained in my previous article) and shareholder dilution via raising equity capital.

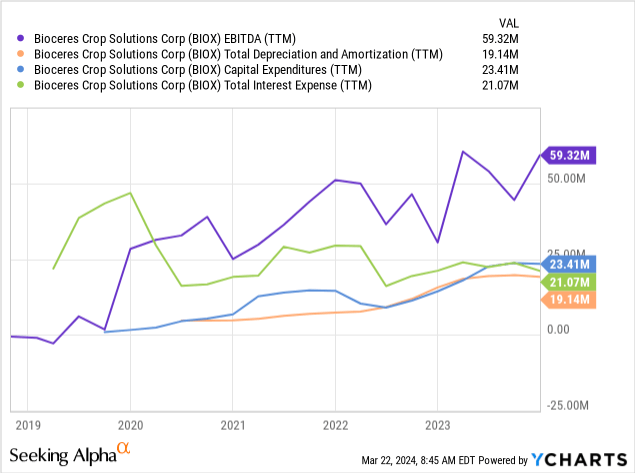

As seen below, EBIT is already approximately $40 million (EBITDA minus D&A or CAPEX), and pre-tax profits are around $20 million annually (EBIT minus total interest expenses).

On these, we need to apply a 30% income tax rate to arrive at an NOPAT of $35 million and a net income of $14 million. These values are too small for a market cap of $800 million (P/E of 57x) and EV of $1 billion (EV/NOPAT of 35x).

EBITDA trends have been pretty muted for the past two years despite the acquisition of Marrone. Bioceres is not yet a growth story, but it is still valued as one. For that reasons I believe it is not an opportunity at these prices.

Read the full article here

Q2 2024 Earnings Call Transcript")