Q2 2024 Earnings Call Transcript")

")

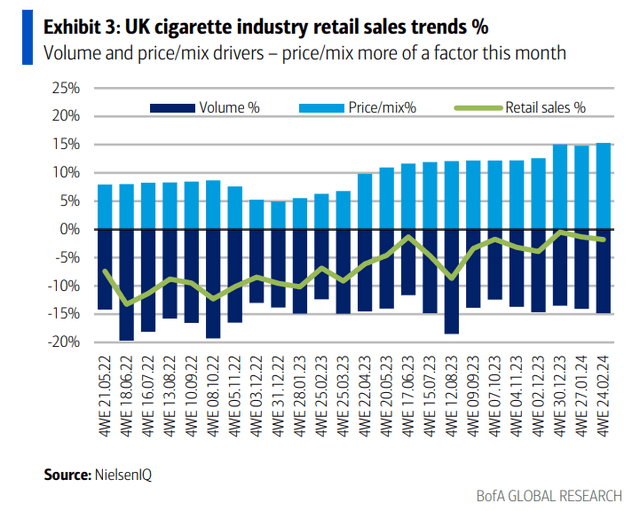

NielsenIQ data show that UK cigarette industry retail sales fell just 1.8% from year-ago levels. That continues an improving trend over the last two years, though sales for Philip Morris International (PM) boasted an annual increase of 6.1% while British American Tobacco (NYSE:BTI) sales dropped 4.7% YoY. Of course, tobacco companies continue to diversify their sales mix, including smokeless tobacco, while embarking on shareholder-friendly initiatives.

I reiterate a buy rating on BTI. With high free cash flow, a big yield, and share buybacks, I see upside ahead while the stock’s technicals show signs of life after a protracted downturn. A recent corporate transaction is also encouraging.

UK Cigarette Sales Stabilizing

BofA Global Research

According to Bank of America Global Research, London-based British American Tobacco is the largest European tobacco company with operations in most major markets across the globe. The company’s biggest market is the US, where it generates around 55% of EBIT. BAT’s main brands are Kent, Dunhill, Lucky Strike, Pall Mall, Rothmans, Newport, Camel, and Natural American Spirit. The company also plays in the Heated Tobacco category with its brand Glo, in vaping where its main brand is Vuse, and in Modern Oral with Velo.

Back in February, BTI reported solid full-year 2023 results. Revenue of £27.28B was down modestly from the previous year but was up 3.1% on an organic basis. Operating cash flow conversion was healthy and the firm sees that metric coming in at 90% in the current year. What was particularly encouraging from a shareholder’s perspective was that BTI took significant steps to reward its equity owners.

Following a partial divestiture of their ITC stake, £1.5 billion of proceeds can be returned to stockholders through buybacks by the end of next year. The sale also brings BTI in line with its peers with respect to its debt/EBITDA ratio – important considering higher interest rates today. That should lend itself to EPS and dividend growth over the years to come. The management team is also taking aim to improve its liquidity while growing its market share in the US through its next-generation portfolio (NGP).

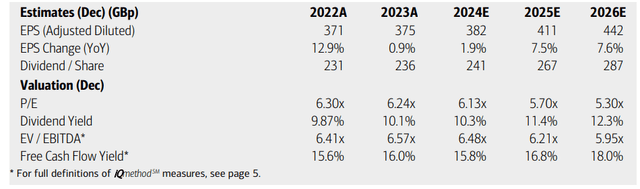

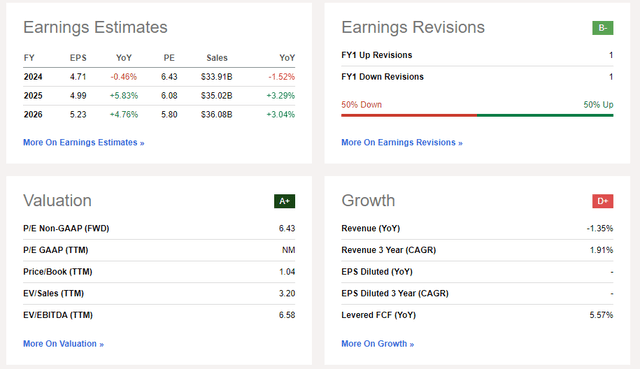

On valuation, analysts at BofA see earnings being about flat this year with solid low- to mid-single-digit growth in 2025 and 2026. For the US ADR shares, Seeking Alpha’s consensus figures show $4.71 of current-year per-share profits and $4.99 out-year EPS with continued growth through 2026. Revenue is seen coming in about flat in 2024 with 3% to 4% growth over the ensuing two fiscal years.

Dividends, meanwhile, are forecast to rise at a fast clip over the coming quarters, potentially resulting in a yield north of 10% depending on what the stock price does. With an exceptionally low EV/EBITDA ratio and an exceptionally strong free cash flow yield, I think the dividend rate going forward will indeed grow.

British American Tobacco: Earnings, Valuation, Dividend Forecasts (GBP, UK Shares)

BofA Global Research

BTI: Earnings Estimates (USD, US ADRs)

Seeking Alpha

If we assume normalized non-GAAP EPS of $4.75 over the next 12 months and apply the stock’s 5-year average earnings multiple of 8.5, then shares should trade between $40 and $41, making it a bargain today as the stock hovers above multi-year lows. Its forward PEG ratio is also below that of the broader market, currently at 1.26.

BTI: Very Low Forward P/E & PEG, Big Cash Flow Yield

Seeking Alpha

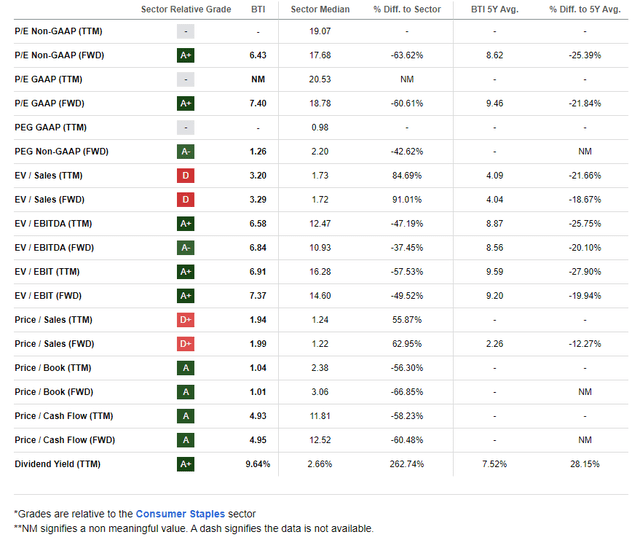

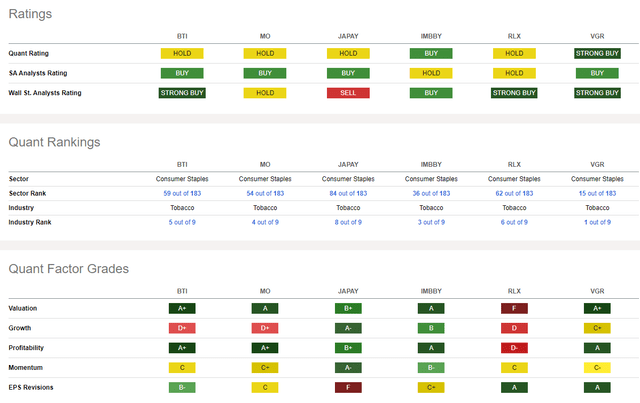

Compared to its peers, BTI features a very strong valuation grade by Seeking Alpha, though weak earnings growth over recent years results in a poor growth rating. But as EPS growth emerges back into the black, I expect more optimism around the bottom-line story. And we are already seeing that via a solid B- EPS revision grade while profitability metrics are robust. Still, share-price momentum has some work to do, but that is a common theme among its Tobacco industry peers.

Competitor Analysis

Seeking Alpha

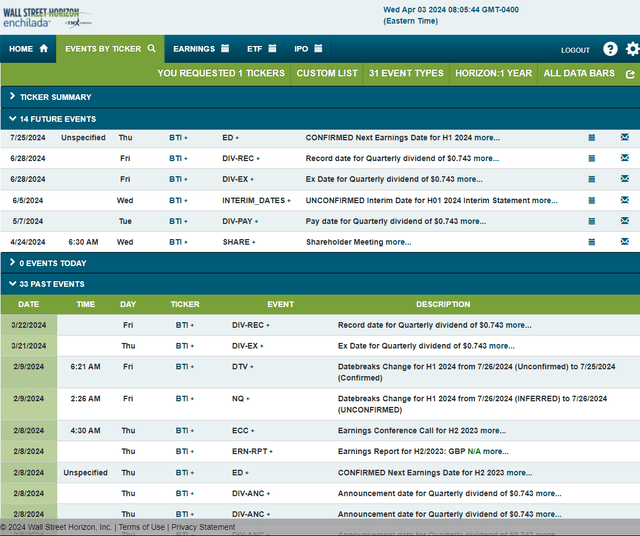

Looking ahead, corporate event data provided by Wall Street Horizon shows a confirmed H1 2024 earnings report to be released on Thursday, July 25. Before that, the company holds its annual shareholders’ meeting on April 24 and is slated to post interim sales data for the first half on Wednesday, June 5.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

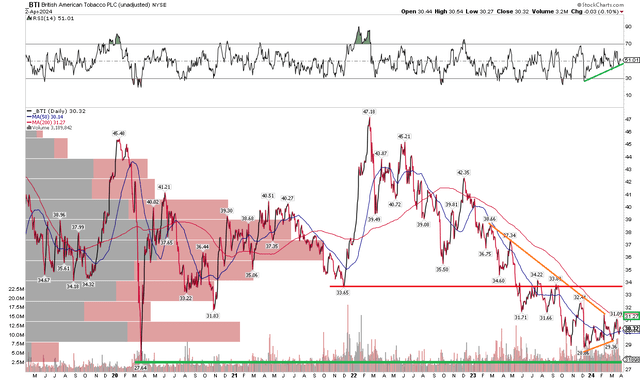

BTI has been treading water since finding a floor late last year. Notice in the chart below that shares have held their March 2020 low and are now approaching their flattening 200-day moving average. With a rising 50dma, the bulls appear to be regaining control of the trend. Also take a look at the RSI momentum oscillator at the top of the graph – it has been trending up since notching a low last October – that is considered to be a harbinger of future price action in the eyes of technicians.

I would like to see BTI rally above its 200dma, but then it enters an area of congestion with resistance around the $34 mark. More significant overhead supply is seen via the volume by price indicator on the left side of the chart in the mid to high $30s. Long here with a stop under $27 still appears as a solid risk/reward play.

BTI: Holding Long-Term Support, Improved RSI

Stockcharts.com

The Bottom Line

I reiterate a buy rating on BTI. I see this value stock with massive free cash flow as improving fundamentally as it focuses on shareholder value. The chart, meanwhile, looks better than it did a handful of months ago given improving momentum trends and a defense of long-term support.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q2 2024 Earnings Call Transcript")

")