")

")

Caledonia Mining Corporation PLC (NYSE:CMCL) is a curious gold miner out in Zimbabwe, whose primary asset is the Blanket Mine. It was one of the first stocks I chose to cover, back in November. Since then, the market has been fairly indecisive about it.

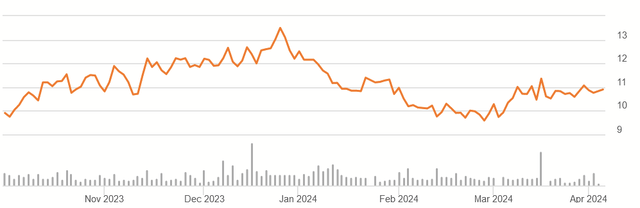

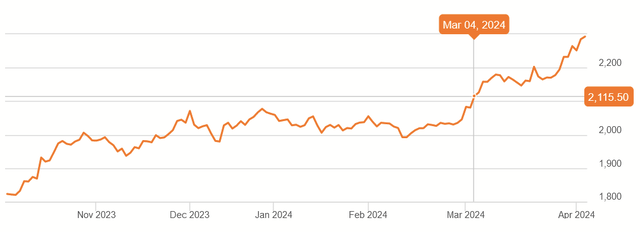

CMCL 6M Price History (Seeking Alpha)

Shares ran up over $13 in December but soon soured, amid disappointing results. I’ll review the disappointments, discuss the future outlook from today’s Q4 earnings call, and I’ll even offer up what I’ve personally found to be a helpful options strategy for those interested.

If this is your first time looking into Caledonia, I recommend checking out my first article, since I give a summary of the company’s history there.

FY 2023 Results

The disappointments relate to:

- Lower production at Blanket in Q1 and Q2

- Less than expected output from the short-term Bilboes project

- Certain higher (but not recurring) costs

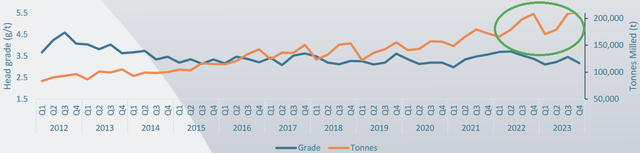

Q4 2023 Company Presentation

As seen above, production declined suddenly at the start of 2023. The company had discussed this before. The decline was due to “equipment failures and logistical issues,” which have since been resolved, evidenced by the increased production in Q3 and Q4.

Bilboes, meanwhile, was put into care and maintenance last summer, after the short-term sulphide project turned out to produce less gold than expected. The long-term potential (that motivated the acquisition) remains unchanged.

Q4 2023 Company Presentation

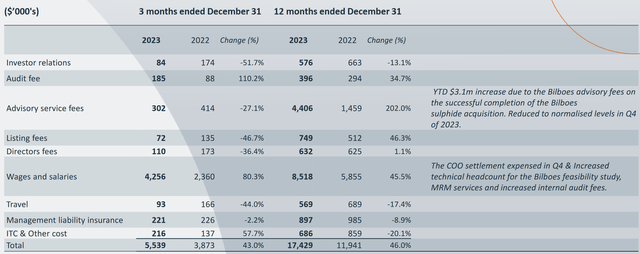

Regarding the increased costs, many of these were short-term in nature. They included a few million in advisory costs for the sulphide project (which has passed). They also included a few million related to severance for the departure of their COO in the fall and increased overtime costs (a time management issue that they have since corrected).

Electrical costs have increased, but their unit costs of electricity have been down, thanks to the solar plant.

FY 2023 Results

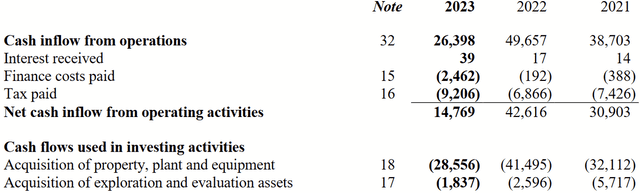

Because of how these issues stack up, operating cash flows fell from $42.6M in 2022 to $14.8M in 2023. Thankfully, we see that capital expenditures have been declining as well.

Future Outlook

Next, I’ll discuss some forward-looking points gathered from this morning’s Q4 earnings call (in which I was present via Zoom).

Blanket Production

Gold production was 78.4K oz produced in 2023, and management is guiding for 74K – 78K annually now, going forward, lower than their 80K+ figure before. Concurrent with that and a newer feasibility study, Blanket’s life of mine has been extended to 2041. I believe this represents an improvement in CMCL as a long-term investment since Blanket is Caledonia’s core asset.

Solar Plant

In Q3 earnings, management elaborated their plans to free up their capital by selling the Blanket solar plant that had constructed and paying the hypothetical owner for the electrical services.

Blanket’s solar plant (caledoniamining.com)

This time, CEO Mark Learmonth explained that the solar plant sale has not yet closed, largely because the counterparty wants to transfer some risk to Caledonia through a sale leaseback. Learmonth was firm that he wants a full sale, no sale-leaseback, and so the negotiations are lingering in the meantime.

Given the rising energy costs and the solar plant’s crucial role in keeping those down, thought has been given to expanding with a second plant, as the current one only provides about 25% of the mine’s electricity. I believe this will become clearer once a decision is reached about the existing plant’s sale.

Bilboes Development

When asked about the long-term prospects for Bilboes, Learmonth explained that it’s going to depend on the timeline for funding. They are currently exploring different options, as they believe they have sufficient means to raise debt and avoid further equity dilution (as he believes debt is their cheapest source of capital right now). After that point, he believes it would be a two-year project to develop the site and begin gold production.

Cash Flows

The decline in operating cash flows was disappointing, but we also know many of its causes were temporary in nature. Moreover, there have been higher gold prices.

Gold $/Oz 6M Price History (Seeking Alpha)

Crucially, after flirting with the line for months, the market finally priced gold above $2,100/oz for the first time in March and has even exceeded the $2,200 milestone. These higher prices will help Caledonia’s margins.

When asked about 2024’s capex, Learmonth also gave a clear answer that he believes it will be $30M.

Valuation

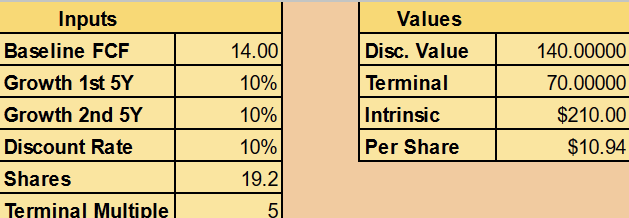

With these updates, it’s time for me to tune my valuation. I’ll do a Discounted Cash Flow model with the following assumptions:

- $14M in baseline free cash flow

- 10% growth rate over the next decade

- Terminal multiple of 5

Given that OCF is typically about $40M+ (2023’s setbacks notwithstanding), higher gold prices, and the figure we got for capex, I think $14M is likely for FCF going forward.

With the declining growth capex at Blanket and the contribution to production at Bilboes on the horizon (I mentioned last time it has potential for 160K oz per year), I believe these will both contribute well to FCF growth rates and make an average rise of about 10% over the decade practical. Since CMCL is a small cap in Zimbabwe and prone to market fears, I’ve also kept the terminal multiple low at 5.

Author’s calculation

With recent market prices, this suggests CMCL is fairly valued at just under $11. It’s also a lower valuation than I provided last time, which was $13.27 per share. Given the important details and outlook provided by the FY results and the earnings call, these lower assumptions felt wiser.

I’ll restate some of the risks to this valuation from last time:

- Changes in Zimbabwe’s economic policy

- Unusual weather/mining accidents

- Sudden declines in price of gold

Then there are some other risks to consider. Caledonia took on more leverage in 2023, issuing its “solar notes.” It has just over $6M in remaining principal on these, due in about two years, and further debt (such as to develop Bilboes) would add to that picture. In years where many inconveniences stack up (one could say that 2023 was an example), this could lead to a situation where the debt is hard to repay.

Caledonia doesn’t have so much debt that I think it would go bankrupt, but I think a dividend cut would be more likely in such a case. Currently, dividends account for an outflow of $11M annually.

Writing Options

While I don’t normally talk about or even encourage options trading, CMCL’s intrinsic value and the current market for its options present an interesting situation, one that I’ve taken up on both the call and the put side.

Recent options quotes (Fidelity.com)

Given CMCL’s volatility that I mentioned earlier and the options contracts being in intervals of $2.50 per share, I’ve found that pretty attractive premiums are offered for contracts. I expect this would only appeal to folks with maybe $5K to $10K invested toward CMCL, given the volume.

Writing monthly options for puts at $10 and calls at $12.50 seems like a decent way to milk extra return. This is especially true if the strategy commits to the fundamentals of the stock itself and setting strike prices based on its intrinsic value.

With both money market rates and CMCL’s dividend around 5%, premiums can serve to enhance this yield attractively. Whether someone starts on the call or the put side, it’s not hard to shift toward writing the opposite contract if assigned.

Conclusion

Caledonia continues to be something of an underdog among gold miners. Yet, I think the market is actually being reasonably cautious this time. The company’s prospects will become clearer after further work is done on Bilboes. It’s a more patient play, and it’s one that probably deserves a greater margin of safety, and that is why I’m not rating it a Buy again, especially if options writing doesn’t interest you, and you want to simplify life with buy-and-hold.

2024 will be an important year as we see what the new-and-improved Blanket can do without setbacks, if the solar plant can be sold, and if funding to develop Bilboes can be procured. Until then, I’m probably not reinvesting my dividends.

Read the full article here

")

")

")