")

")

Successful biotechs rarely have the luxury of taking a leisurely victory lap, as the Street is almost always focused on the next driver. In the case of Neurocrine Biosciences (NASDAQ:NBIX), the shares had been doing okay since my last update prior to the recent quarterly earnings/guidance announcement, but ongoing concerns about the pipeline and near-term growth prospects continue to weigh on sentiment.

I continue to believe that Neurocrine shares are undervalued, but a lot of upside rests on successful clinical trial outcomes, and the company has quite a few meaningful Phase II read-outs coming in 2024. Not all of these will be successful, such is the nature of drug development, but a key win or two could add a welcome tailwind for the share price.

It Takes Money To Make Money, But The Street Didn’t Like 2024 Guidance

Neurocrine’s recent Q4’23 earnings report didn’t do much to stoke investor enthusiasm, with the stock losing approximately $900M in market capitalization since, as key drug Ingrezza came in a bit light of expectations and guidance for 2024 was not only within expectations, but suggestive of relative modest growth in 2024. On top of that, management guided to substantially higher opex, though I would argue this is money well-spent for the long-term benefit of shareholders.

Ingrezza

Looking first at Ingrezza, sales rose 25% year over year and about 3% sequentially, coming in about 1% shy of expectations. Guidance for 2024 ($2.1B to $2.2B) was slightly better than Street expectations at the midpoint (an average sell-side estimate of about $2.11B), but annualizing Q4’23 results suggest around 7.5% year-over-year growth, which is below that double-digit hurdle the Street really likes to see.

Management has often been conservative with its initial sales estimates, and there are some drivers that could lead to better outcomes. The launch in Huntington’s-associated chorea is just getting going, and this market could have some upside as only about 20% of eligible patients use Teva’s (TEVA) Austedo. With that low rate of adoption due in part to challenging dosing and high out-of-pocket costs, issues that aren’t present with Ingrezza, this could be a better market than expected.

Neurocrine also continues to invest in market development. The company’s direct-to-consumer marketing can help at least partly offset some physician reluctance to diagnose and treat tardive dyskinesia, and the company is starting to push more actively into long-term care facilities (and a new sprinkle formulation should facilitate that effort).

Opex

Neurocrine is fairly profitable these days (an operating margin of 29.2% in Q4’23), and management is choosing to leverage that profitability to continue to invest in the business. TO that end, operating expense guidance for 2024 was a fair bit higher than the Street expected, with R&D spending of $570M to $600M (versus around $555M expected) and SG&A spending of $830M-$850M (versus a $786M average estimate).

Truthfully, I don’t think the Street cares too much about the R&D spending – the company disclosed during its December Analyst Day that it is targeting 20 new clinical compounds over the next five years and the company has a robust slate of Phase II trials already underway.

With the SG&A spending, though, there’s definitely increased spending on Ingrezza baked into this guidance, including a focused marketing program to support the chorea indication. Management is also going to spend around $50M on pre-approval market development for crinecerfont, and this could well count for much of the overage in spending.

I frankly think this is a good use of money. Ingrezza had a strong launch in part due to the fact that management made similar investments ahead of approval and given that physician and payor education will be an important part of a successful crinecerfont launch (the first new drug specifically for congenial adrenal hyperplasia), I think this is money well spent.

A “Barbell” Pipeline Could Lead To Strong Sales Down The Line

Not unlike H. Lundbeck (OTCPK:HLUBF) (OTCPK:HLBBF), which I recently wrote about, one of the challenges at Neurocrine is a “barbell-shaped” business. Ingrezza is approved and generating strong profits for Neurocrine, and crinecerfont will likely start contributing sales in 2025 (with a multiyear ramp likely).

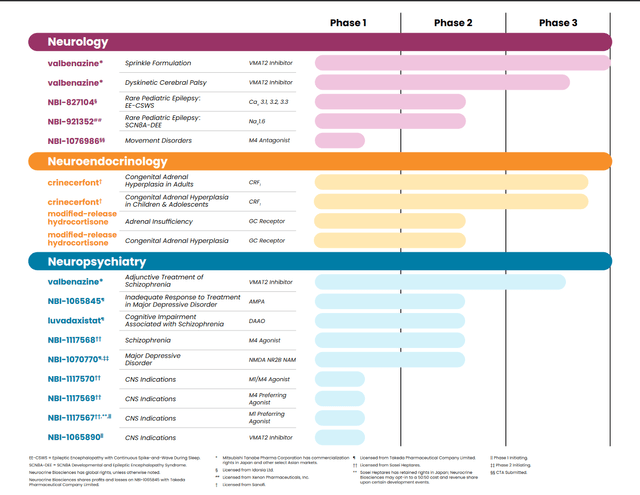

Behind that, though, Neurocrine’s pipeline skews much earlier-stage and higher-risk. There are certainly promising compounds here, and management intends to be active on internal candidate generation and potential in-licensing/acquisition, but the reality is that early-stage neuro-psych drug development is notoriously risky (as seen in the late 2023 clinical failures of NBI-‘352 in focal onset seizures and NBI-‘846 in anhedonia associated with major depression).

Neurocrine Biosciences current pipeline (Neurocrine Biosciences)

Two Phase II programs are expected to read-out in the first half of 2024. Efmody, a candidate for adrenal insufficiency and congenital adrenal hyperplasia, isn’t a particularly high-potential program. The second one (NBI-‘845) is a more interesting candidate for drug-resistant major depressive disorder (or MDD). This is a tough, tough, indication, and I’m assuming only a 10% chance of success, but this could be a $1B+ drug if it works.

A little further back are Phase II read-outs in 2H’24 for NBI’568 in schizophrenia and luvadaxistat in schizophrenia-associated cognitive impairment. Big Pharma has shown interest in the M4 space (‘568 is a selective M4 agonist), with Bristol-Myers (BMY) acquiring Karuna (KRTX) for a $12.7B enterprise value to get KarXT – a M1/M4 agonist targeting schizophrenia and psychosis in Alzheimer’s, as well as potential indications like bipolar disorder and agitation in Alzheimer’s.

Neurocrine would likely be third to market here, behind KarXT and Cerevel’s (CERE) emraclidine, but a multibillion-dollar market can support three drugs. Still, the realities of competition are such that while the odds of positive Phase II data seem better-than-average, there is going to be a higher bar here and upside could be tied to an efficacy profile that shows some differentiation from those more-developed rivals.

The situation with luvadaxistat is quite different. I see this as a much higher-risk program, but if the drug does show compelling efficacy, it could become a standout late-stage candidate.

Behind these compounds is an interesting list of early-stage candidates, including M1, M4, and M1/M4 compounds (NBI-‘567, NBI-’986, and NBI-‘570), with the latter already in Phase I development for CNS indications and the other two expected to start Phase I studies in CNS indications (‘567) and movement disorders (‘986) later this year). Last and not least is NBI-‘890, a new selective VMAT2 inhibitor that is more potent than Ingrezza and that will be studied for various CNS indications.

Importantly, Neurocrine has signaled a shift in its pipeline philosophy – shifting away from psychology toward neurology. Given better-defined pathologies, better-defined efficacy criteria, and less competition (in many cases, at least), I think this is a sound strategy, as psychiatric drugs are notoriously difficult to develop and even if approved, it can be difficult to differentiate them from existing (and often generic) therapies.

The Outlook

Stronger guidance for Ingrezza would have been nice to see, but I still see upside in this drug, as there is still a meaningful untreated/under-treated population here and schizophrenia unfortunately remains a “growth” category in psychiatry.

I’m also bullish on crinecerfont. Management provided additional data on the Phase III trials that included strong placebo-adjusted declines in A4 for both pediatric (-86%) and adult (-66%) patients – well ahead of the thresholds considered significant (the bar for pediatric was a 55% reduction). This strong efficacy supports my above-consensus view that crinecerfont will become a $1B-plus drug over time, but the “over time” part is important, as I think it will take time to expand usage beyond the most severe patients and into more marginal candidates.

My Ingrezza estimates haven’t changed much, but I have increased my assumptions for crinecerfont on that incremental data. I’ve also eliminated the failed candidates for epilepsy and MDD from the model, while adding in estimate for NBI-‘845 in MDD (about $5/share) and upgrading my estimates for NBI-‘568 (to $17/share), with the later driven in part by the value established in the Bristol-Myers acquisition of Karuna.

All told, Ingrezza contributes about $96/share to my fair value, with crinecerfont adding about $28/share and NBI-‘568 adding about $17/share. Including all other contributors, I get a fair value of about $149 (versus $134 previously). I would also note that much of the pipeline carries relatively low odds of approval (<10% to 35% in my model) and if/when positive clinical data comes out, that can unlock meaningful upside.

The Bottom Line

Using my risk-weighted approach, I can’t argue that Neurocrine is a screaming buy, but I do still acknowledge that upside potential from positive clinical read-outs. I also like management’s shift toward neurology and its willingness to explore multiple drug chemistries (peptides, small molecules, antibodies, gene therapy, et al), not to mention its ongoing willingness to consider in-licensing and/or acquisitions where appropriate.

Given a still-undervalued core asset (Ingrezza), an upcoming new contributor (crinecerfont) that I believe the Street underestimates, a growing pipeline of early-stage drugs targeting large addressable markets, and a profitable base business with significant cash ($1.7B), I believe Neurocrine is still very much a biotech worth considering.

Read the full article here

")

")