")

Introduction

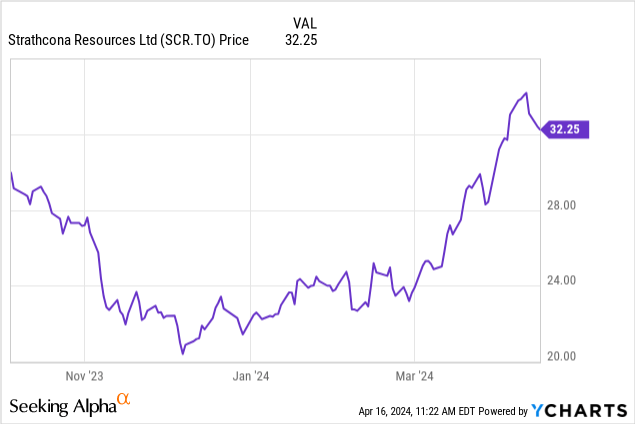

Last December, I argued Strathcona Resources (TSX:SCR:CA) (OTCPK:STHRF) was too cheap after its share price corrected subsequent to the completion of the acquisition of Pipestone Energy. I wasn’t a big fan of the sale of Pipestone to Strathcona as Pipestone had a valuable condensate production, but the acquisition made sense from Strathcona’s perspective as condensate is mainly used as a diluent or heavy oil transportation. As Strathcona is a large heavy oil producer, reducing its exposure to condensate prices by acquiring a condensate producer was a solid move.

Despite the recent share price increase, I think there’s more room to run. The company is trading at less than half the NAV/share using an oil price lower than the current spot price. Additionally, at US$80 WTI, the company will generate just over C$6/share in sustaining free cash flow this year.

Strong production in the fourth quarter sets the tone for 2024 cash flow expectations

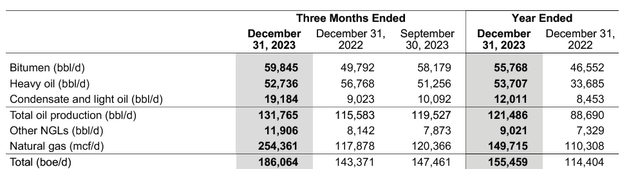

In the fourth quarter of the year, the company produced approximately 184,300 barrels of oil-equivalent per day, of which almost 132,000 barrels consisted of “real” oil. As you can see below, the vast majority of the oil production comes from the production of bitumen and heavy oil, which trades at a lower price than the light oil (and condensate).

Strathcona Investor Relations

Strathcona also produced just under 12,000 barrels per day of natural gas liquids while the remaining oil-equivalent output was contributed by the production of natural gas. This means that about 77% of the total output consisted of liquids and 71% of the oil-equivalent output was oil.

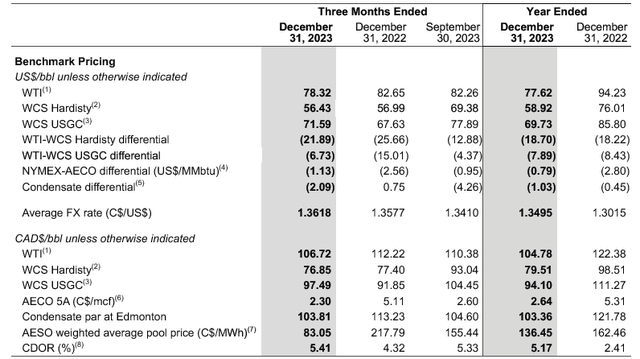

The pricing levels were quite interesting. The average WTI oil price was almost C$109/barrel during the quarter, while the heavy oil price was just under C$79/ barrel in Canada and around C$97.5/barrel at the US Gulf Coast.

Strathcona Investor Relations

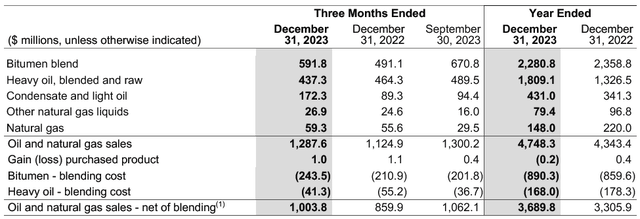

The total revenue in the final quarter of the year was C$1.29B before taking blending costs into consideration, and approximately C$1B after taking the blending costs into account. And as you can see below, the natural gas revenue represented just 5% of the pre-blending revenue, although it accounted for 23% of the oil-equivalent output.

Strathcona Investor Relations

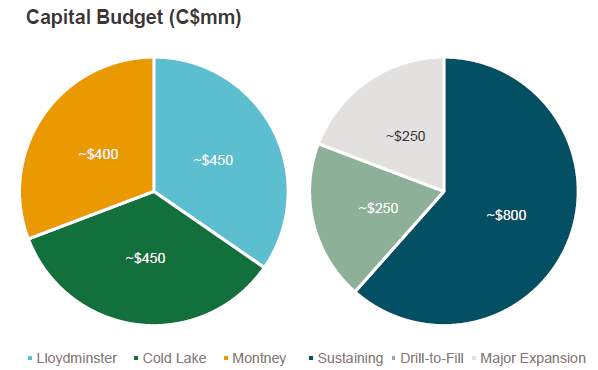

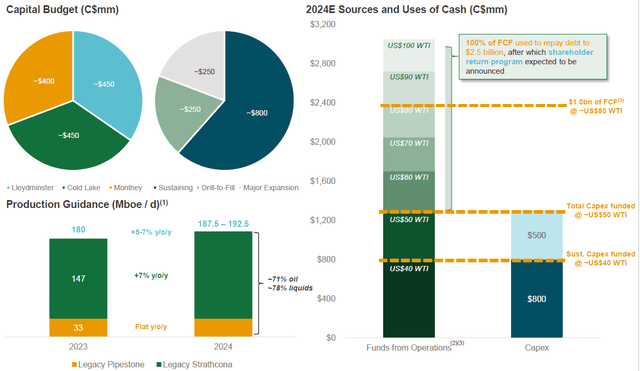

The strong oil price resulted in a total funds flow of C$471M and a net free cash flow result of C$151M. While that was relatively low, keep in mind the C$308M in capex exceeds the required sustaining capex to keep the production level unchanged. As you can see below, the company is budgeting a total capex of C$1.3B for 2024 but only C$800M of that budget is referring to sustaining capex. This means the average quarterly sustaining capex is approximately C$200M and if I would use that number on the Q4 results, the underlying free cash flow was could actually have been C$260M instead of the C$151M that was reported by Strathcona.

Strathcona Investor Relations

As the company’s share count is approximately 214M shares, the underlying free cash flow result was thus roughly C$1.21 per share.

And Strathcona has plenty of useful things to do with the incoming cash flow. First of all, as explained above, of the C$260M in underlying sustaining free cash flow, just over C$100M was directed to growth initiatives. The rest of the free cash flow is used to reduce net debt. Strathcona has a net debt target level of C$2.5B whereafter it will be in a position to announce a shareholder return program. At the end of 2023, Strathcona had C$2.67B in net financial debt, but there also was a C$620M in working capital deficit. The company is not taking the working capital deficit into consideration when it’s talking about its debt targets, and considering Strathcona was close to its self-imposed C$2.5B net debt target and considering the oil price remains strong, the company may have reached the C$2.5B debt limit at the end of Q1 (but this depends on working capital variations). In any case, Strathcona is very close to meet its debt target.

The company also provided a sensitivity analysis using different oil price ranges and at US$80 WTI, Strathcona will generate approximately C$1B in free cash flow after taking growth initiatives into consideration. This indeed means the reported free cash flow will be approximately C$4.65 per share while the underlying sustaining free cash flow will be roughly C$6/share.

Strathcona Investor Relations

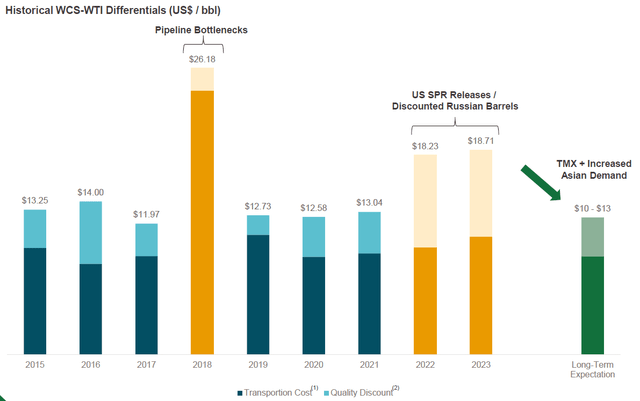

The sensitivity chart above takes a discount of 10% of the WTI price + US$5/barrel into consideration for Western Canadian Select oil.

Strathcona Investor Relations

The updated reserves report contains a lot of useful information

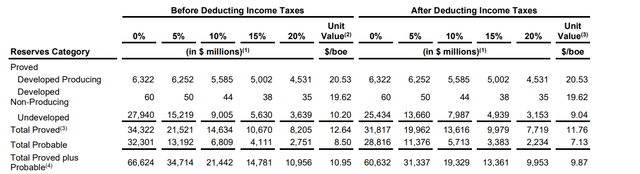

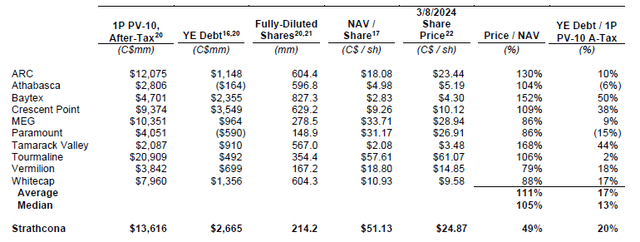

Every year, Canadian oil and gas producers need to publish an updated reserves statement and that provides a good look under the hood for investors. I like to keep an eye on the PV10 value of the reserves and in Strathcona’s case, the after-tax PV10 of the 2P reserves is approximately C$19.3B.

Strathcona Investor Relations

Divided over the current share count of 214M shares, this represents an after-tax NPV10% of around C$90/share, and even after deducting the C$13/share in net debt, you’d end up with C$77/share in theoretical NAV. That however excludes corporate overhead and interest expenses, but it’s clear that even after the recent share price increase to in excess of C$30 Strathcona is still trading at a discount to its fair value.

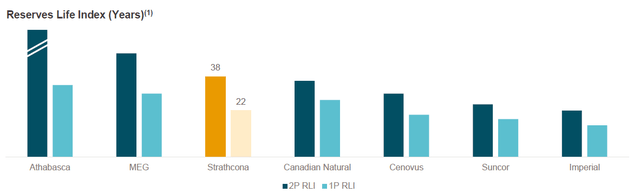

The main driver are the very large 2P reserves which underpin a 38-year remaining life of the assets. Meanwhile the company also has C$6.1B in tax pools and does not expect to be a net tax payer before 2027. And as the tax savings happen up front, it obviously has a sizable impact on a DCF calculation.

Strathcona Investor Relations

The PV10 calculation is based on an average oil price between US$75 and US$80 on a WTI basis between 2024 and 2028 so the assumptions used in the calculation are pretty realistic. Strathcona likes to highlight its undervaluation compared to its peers (shown below on a 1P basis).

Strathcona Investor Relations

Investment thesis

Despite spending C$500M on growth and improvements this year, the net debt will likely drop by about 40% (on the condition the oil price remains at around or just above US$80 on a WTI basis). I think the focus on debt reduction is the right thing to do, and I hope that even after the initial target level of C$2.5B is achieved, Strathcona will continue to deleverage. These are undeniably good times for Strathcona and it would only make sense to go the extra mile and reduce the total debt a bit more to be better protected during an era of weaker prices (but management doesn’t seem to be too interested in doing this, as indicated on the Q4 call). Additionally, as the company is currently paying north of C$50M per quarter in interest expenses, a substantial reduction of the gross debt would have an immediate impact on the interest payments and thus the underlying cash flows.

Strathcona could become an interesting dividend payer as a payout ratio of 50% of the free cash flow after growth investments would result in a dividend of C$2.40 per share. That being said, considering the stock is trading at a big discount to its NAV, Strathcona also may want to buy back its own shares to further increase the NAV/share. While we will have to wait for an official announcement I think a combination of both types of shareholder rewards makes the most sense although Strathcona’s management is focusing on dividends and plans to announce a base dividend and a variable dividend.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")